Last Updated: June 2026

This article is written for estate planning attorneys, CPAs, and family business owners preparing to transfer business interests. You will learn how DLOC and DLOM are calculated, what the IRS requires, and how to protect your discount from challenges.

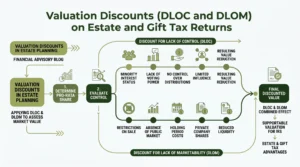

Valuation discounts for estate tax refers to percentage reductions applied to the fair market value of a business interest when that interest lacks full control or cannot be sold quickly. These discounts lower the taxable value reported on IRS Form 706 or Form 709, reducing estate and gift tax liability. They apply to minority interests in family businesses, closely held LLCs, and limited partnerships.

When the IRS audits an estate or gift tax return, discount support is among the first items reviewed. A discount that lacks a credentialed appraisal or fails to meet IRS Revenue Ruling 59-60 standards can be disallowed. Sofer Advisors, headquartered in Atlanta, GA, provides qualified appraisals for estate and gift tax returns backed by dual ASA and ABV credentials recognized by the IRS, SEC, and FINRA.

Key Takeaways

- DLOC Reduces Control Value – A discount for lack of control (DLOC) typically ranges from 15% to 35% for minority interests in closely held entities.

- DLOM Reflects Illiquidity – A discount for lack of marketability (DLOM) ranges from 20% to 40% based on industry, company size, and exit options.

- Combined Discounts Are Multiplicative – A 25% DLOC and 30% DLOM produce a combined reduction of about 47.5%, not 55%, because they are applied sequentially.

- IRS Requires a Qualified Appraisal – Treasury Regulation 1.170A-17 requires a qualified appraisal by a credentialed appraiser to support discounts on a tax return.

- Audit Risk Is High – The IRS Office of Chief Counsel lists valuation discounts as a top compliance focus, and unsupported discounts are routinely challenged.

- Timing Matters – The appraisal must reflect value as of the date of gift or date of death, not the return filing date.

These rules interact in practice. The sections below examine each one in detail.

What Is a Discount for Lack of Control?

A discount for lack of control (DLOC) reflects the lower value placed on a minority interest that cannot direct company decisions. A minority shareholder in a closely held business cannot force distributions, compel a sale, or change management strategy. This powerlessness reduces what a hypothetical buyer would pay. That reduction is the DLOC.

Revenue Ruling 59-60 establishes the hypothetical buyer and seller framework. Courts recognize the inability to control as a real economic limitation. A 30% interest in a family LLC carries less per-unit value than a 100% interest. This holds true even when the underlying assets are identical.

Analysts typically support a DLOC using restricted stock studies and control premium data from public company acquisitions. The typical range is 15% to 35%. An appraiser who applies a flat 35% without fact-specific analysis gives the IRS an easy target. The correct approach ties every percentage to entity documents and economic conditions as of the valuation date.

What Is a Discount for Lack of Marketability?

A discount for lack of marketability (DLOM) reflects the cost and time required to convert a closely held interest into cash. Unlike shares of a public company, a minority interest in a family LLC or S-corporation has no ready market. Legal restrictions often limit who can buy. The DLOM is applied after the DLOC, to the already-discounted minority value – the discounts multiply, not add.

Several models support a DLOM. The Mandelbaum factors, from Tax Court case Mandelbaum v. Commissioner (1995), offer a nine-factor framework. It covers dividend policy, management, and holding period. Analysts also use option-pricing models like the Longstaff and Finnerty models. Restricted stock studies show historical average discounts of 25% to 35%.

A 30% to 40% DLOM is defensible when a layered Mandelbaum analysis and at least one quantitative model support it. Applying DLOM without that structure invites IRS scrutiny. It is often the larger of the two discounts. It requires both methodological rigor and clear written documentation.

How Are the Two Discounts Combined?

Combining DLOC and DLOM requires a specific calculation sequence. You do not add the two percentages. The correct method is multiplicative, and understanding this math matters for the numbers reported on Form 706 or Form 709.

Here is an example using a simplified fact pattern:

| Step | Description | Value |

|---|---|---|

| 1. Enterprise Value (100% control) | Fair market value of the whole company | $5,000,000 |

| 2. Pro-Rata Minority Interest (25%) | Straight proportional slice | $1,250,000 |

| 3. Apply DLOC (25%) | Minority interest value after control discount | $937,500 |

| 4. Apply DLOM (30%) | Value after marketability discount | $656,250 |

| 5. Combined Effective Discount | Reduction from pro-rata value | 47.5% |

The table above shows that a 25% DLOC and 30% DLOM do not produce a 55% combined discount. The combined reduction is about 47.5%. The DLOM applies to the already-discounted minority value – not the original enterprise value. This distinction matters when explaining the discount to a client or an IRS examiner. A well-supported report shows each step clearly and ties each discount to a specific method.

Why Does the IRS Challenge Valuation Discounts?

The IRS challenges valuation discounts because the dollar amounts at stake are large. Estate and gift tax is assessed at rates up to 40%. A $1 million reduction in reported value saves $400,000 in tax. The IRS has a strong incentive to examine whether each discount is real and properly supported.

Three common reasons discounts are challenged include:

- The appraisal was not performed by a qualified appraiser under Treasury Reg. 1.170A-17

- The appraiser applied a blanket discount without fact-specific analysis tied to entity documents

- The appraisal date did not match the gift date or date of death

The IRS Office of Chief Counsel identifies valuation discounts as a compliance priority for family limited partnerships and LLCs. The entity must also have genuine business purpose and documented governance activity. Courts have upheld discount disallowance when an entity formed with no purpose beyond holding personal assets.

How Do Appraisers Support Discounts on Tax Returns?

A qualified appraisal for estate and gift tax purposes must meet Treasury Regulation 1.170A-17 and conform to USPAP. For business interests, the American Society of Appraisers Business Valuation Standards also apply.

The core steps in the process are:

- Review entity documents for transfer restrictions and voting rights

- Analyze three to five years of financial statements

- Apply the income, asset, or market approach as appropriate

- Apply DLOC and DLOM using benchmarked models and documented reasoning

Each step produces documentation that defends a specific part of the discount. Gaps in any step create audit vulnerabilities. A summary letter does not satisfy Treasury Regulation 1.170A-17. The penalty for an unsupported valuation can reach 40% of the underpayment under IRC Section 6662(h). David Hern CPA ABV ASA, founder of Sofer Advisors, holds dual accreditations satisfying the IRS definition of qualified appraiser for estate and gift tax engagements.

What Is the Sofer Advisors Approach to Discount Analysis?

The Sofer Difference is a four-phase process – Discovery, Diligence, Analysis, and Delivery – designed to give estate planning teams a clear and defensible discount analysis that holds up under IRS review. Each phase builds on the last. No step is skipped regardless of timeline pressure.

In Discovery, the team collects entity documents and financial statements. In Diligence, analysts normalize the financials and identify relevant discount studies. In Analysis, the team applies DLOC and DLOM and tests results against published benchmarks. In Delivery, the final report meets Treasury Regulation 1.170A-17 standards and attaches to Form 706 or Form 709.

Sofer Advisors brings a Heart of a Teacher to this process, translating technical language into plain explanations attorneys and CPAs can use when responding to IRS inquiries. A discount buried in jargon is harder to defend than one backed by clear, logical reasoning.

When Should You Order a Discount Appraisal?

Timing is critical. The appraisal must reflect conditions as of the valuation date – the date of gift or date of death. An appraisal completed months after the transfer is a reconstruction and carries higher audit risk.

Order the appraisal as early as possible. For gift tax, complete the appraisal before the gift is made. For estate tax, the executor typically has nine months to file Form 706, but waiting until the final month creates deadline risk. Most appraisals are completed within four to eight weeks. Each new transfer requires its own contemporaneous analysis – a prior-year appraisal does not carry over.

Frequently Asked Questions

What are valuation discounts for estate tax?

Valuation discounts for estate tax are percentage reductions applied to the fair market value of a business interest that lacks full control or marketability. The two main types are DLOC (discount for lack of control) and DLOM (discount for lack of marketability). Together, they lower the taxable value reported on Form 706 or Form 709. They apply to minority interests in closely held businesses, family LLCs, and limited partnerships.

How are valuation discounts typically applied in estate tax planning?

Discounts are applied in a two-step sequence. First, a DLOC is applied to the control value to reach the minority interest value. Then a DLOM is applied to that minority value to reflect illiquidity. The two discounts multiply rather than add. This requires a qualified appraisal as of the date of death or gift date, conforming to Treasury Regulation 1.170A-17 and USPAP standards.

What are valuation discounts and how do DLOC and DLOM differ?

DLOC reflects the reduced value of a minority interest that cannot direct business decisions, compel distributions, or force a sale. DLOM reflects the inability to sell quickly at full value. DLOC is applied first to the control value. DLOM is applied second to the resulting minority interest value. Both require separate supporting methodology and written documentation in the appraisal report.

What discount on estate taxes is typically allowed by the IRS?

The IRS does not set a fixed percentage for valuation discounts. DLOC commonly ranges from 15% to 35%, and DLOM commonly ranges from 20% to 40%. Combined discounts of 35% to 50% are common when both apply. The IRS scrutinizes discounts above 40% on either factor and requires detailed, fact-specific appraisal support to allow discounts at the high end of published ranges.

Can the IRS disallow a valuation discount already reported on a return?

Yes. The IRS can disallow a discount during audit if the appraisal does not meet qualified appraisal standards, the discount lacks fact-specific support, or the entity lacks genuine business purpose. The IRS has three years from the filing date to audit, or six years if the value understatement exceeds 25%. Penalties of 20% to 40% plus interest apply to unsupported discounts.

How much does a valuation discount appraisal from Sofer Advisors cost?

A valuation for estate or gift tax purposes typically ranges from $7,500 to $25,000 depending on entity complexity, number of interests transferred, and required documentation. Most engagements are completed within four to eight weeks. Rush engagements are available at a 25% to 50% premium. Schedule a free consultation to receive a scoped estimate for your specific situation.

Are valuation discounts available for real estate held in an entity?

Yes, when the interest transferred is a minority stake in the entity rather than direct property ownership. The entity must have genuine business purpose beyond tax planning. Courts have removed discounts when the sole purpose of an LLC was holding personal-use real estate. A formal operating agreement and documented business activity are required for the discount to hold.

What happens if a discount is challenged in Tax Court?

The Tax Court reviews the appraisal, the appraiser’s credentials, methodology, and benchmark comparability. Cases like Estate of Mandelbaum v. Commissioner show courts give weight to detailed, well-reasoned reports and reject flat unsupported percentages. Having an appraiser with expert witness experience strengthens the taxpayer’s position. David Hern has served as an expert in 11+ cases across multiple jurisdictions.

Related Case Studies

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

- Minority Interest And Marketability Discounts In Business Valuation

- Closely Held Business Valuation For Estate Tax Atlanta Guide

Executive Summary

Valuation discounts for estate tax – specifically DLOC and DLOM – lower the taxable value of minority interests in closely held businesses on Form 706 and Form 709. DLOC reflects lack of control and ranges from 15% to 35%. DLOM reflects illiquidity and ranges from 20% to 40%. The two are applied sequentially, producing combined effective discounts that can reach 47% or more. IRS scrutiny is significant, and only a qualified appraisal by a credentialed appraiser under Treasury Regulation 1.170A-17 provides reliable audit protection.

What Should You Do Next?

Review the entity documents for any interest you plan to gift or include in an estate and confirm whether a qualified appraisal is in place. If an appraisal exists, verify it was prepared as of the correct valuation date. If none exists, begin the engagement early to meet filing deadlines.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides qualified appraisals for estate and gift tax returns that meet IRS standards and are prepared to withstand audit examination. Schedule a consultation to discuss your valuation discount needs and receive a scoped engagement estimate.

People Also Read

- Valuation Of Closely Held Business For Estate Tax Purposes

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}