Last Updated: June 2026

This article is for business owners, advisors, and CPAs who need a clear breakdown of how these two discounts are defined, measured, and applied. After reading, you will know which discount applies to your situation. You will understand the typical magnitude. You will also have practical steps to reduce it before a formal valuation is completed.

An owner dependency discount is a reduction applied to a business’s value when too much of its revenue, relationships, or operational knowledge rests with a single owner. It matters because buyers and appraisers treat that concentration as a direct financial risk. That risk cuts what they will pay. In practice, this discount can shave 10% to 40% off an otherwise healthy valuation. This makes it one of the costliest overlooked factors in any sale or succession event.

Understanding the difference between owner dependency and the related but distinct key person discount is not just an academic exercise. When Sofer Advisors, headquartered in Atlanta, GA, conducts a business appraisal for an owner planning an exit, financing event, or estate transfer, one of the first questions the team asks is: what happens to this business if the owner steps away tomorrow? The answer shapes the entire valuation. It often determines whether a deal closes at the asking price or at a steep reduction.

Key Takeaways

- Owner Dependency vs Key Person – These are related but distinct. Owner dependency covers operational control. A key person discount targets revenue tied to one individual’s relationships or skills.

- Discount Magnitude – An owner dependency discount typically ranges from 10% to 40% of enterprise value. This depends on how embedded the owner is in daily operations and client relationships.

- Triggering Factors – Appraisers look for at least 5 indicators: owner controls pricing, owner holds primary client contacts, no written procedures exist, no management team is in place, and revenue declines are expected after departure.

- Minority Interest Overlap – A minority interest discount (DLOM or DLOC) can stack on top of an owner dependency adjustment. This can compound the total reduction to 50% or more in some cases.

- Reduction Timeline – Most owners need 12 to 36 months of documented operational changes before an appraiser will meaningfully reduce or remove the discount.

- Regulatory Standards – Both the American Society of Appraisers and the AICPA Forensic and Valuation Services division require appraisers to document and support any company-specific risk adjustments in their written reports.

What Is an Owner Dependency Discount?

An owner dependency discount is a company-specific risk premium. Appraisers add it to the discount rate – or subtract it directly from value – when a business cannot function at full capacity without its owner. This adjustment reflects the probability that revenue, profitability, or key relationships will erode when the owner exits. It is not a penalty. It is a measurement of real economic risk that buyers price into any offer.

Appraisers apply this adjustment most often under the income approach, using DCF or capitalization of earnings methods. When the owner is deeply embedded in operations, the appraiser may increase the company-specific risk component of the discount rate by 2 to 10 percentage points. The IRS does not mandate a specific method, and neither does USPAP. Any adjustment must be supported by objective evidence. This includes interview findings, financial data, customer concentration reports, and industry benchmarks.

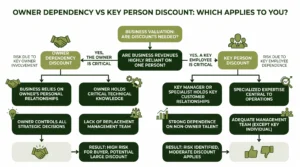

How Does It Differ from the Key Person Discount?

The key person discount is a narrower adjustment. It targets the revenue or profit that will be lost if a single individual – whether the owner or a non-owner executive – leaves the business. Owner dependency is the broader category. The key person discount is one specific mechanism within it.

If a business earns $1.2 million in revenue and $800,000 traces directly to the owner’s relationships, the key person discount addresses that revenue risk. If the same business also lacks documented processes and a management team, the owner dependency discount addresses the operational risk. Both can apply at the same time.

Key person adjustments also appear in life insurance planning and buy-sell agreement valuations. Owner dependency tends to produce larger adjustments because it affects the entire operational structure, not just one revenue stream.

What Triggers an Owner Dependency Finding?

Appraisers look for specific, observable evidence before applying an owner dependency discount. There must be documented indicators that value is materially tied to the owner’s presence. A general sense that the owner is important is not enough.

The most common triggers fall into five categories:

- The owner controls all major pricing decisions and no written pricing policy exists

- The owner is the named contact on 50% or more of client contracts or accounts

- There is no written operations manual or documented business processes

- No management team is in place to handle daily decisions independently

- Historical revenue shows a measurable correlation to the owner’s personal activity

Two or three strong indicators are often enough to justify an adjustment. In divorce proceedings or shareholder disputes, a high owner dependency finding can support a personal goodwill allocation. This may reduce the enterprise value subject to division.

Our four-phase process – Discovery, Diligence, Analysis, and Delivery – surfaces these risks early. Clients understand what drives their value before the final report is issued. That transparency is what we call The Sofer Difference.

How Much Is a Business Worth With $500K in Sales?

Revenue alone does not determine value, but owner dependency can significantly affect the multiple applied to those earnings. A business with $500,000 in revenue and strong systems might trade at 3 to 5 times seller’s discretionary earnings (SDE). At a 20% SDE margin, that is $100,000 in earnings. Apply a 20% to 30% owner dependency discount, and the concluded value drops from $350,000 to as low as $210,000.

The table below illustrates this with a 20% SDE margin and a 3.5x earnings multiple:

| Dependency Level | SDE | Base Value (3.5x) | Discount Range | Concluded Value |

|---|---|---|---|---|

| Low (documented systems, team in place) | $100,000 | $350,000 | 0% – 5% | $332,500 – $350,000 |

| Moderate (some reliance, partial processes) | $100,000 | $350,000 | 10% – 20% | $280,000 – $315,000 |

| High (owner controls most functions) | $100,000 | $350,000 | 25% – 35% | $227,500 – $262,500 |

| Severe (no team, all relationships owner-held) | $100,000 | $350,000 | 35% – 45% | $192,500 – $227,500 |

A “severe” classification can cut concluded value nearly in half compared to a “low” classification. Buyers factor this in through due diligence. They often require sellers to stay involved for 12 to 24 months under an earnout when dependency is high.

What Is a Typical Minority Discount?

The minority interest discount is a separate adjustment that reduces the value of a non-controlling ownership stake. It is distinct from owner dependency, but the two frequently appear together in the same appraisal.

A typical minority discount has two components. The discount for lack of control (DLOC) reflects that a minority owner cannot force dividends or control major decisions. The discount for lack of marketability (DLOM) reflects that a minority interest in a private company cannot be quickly sold. Combined, DLOC and DLOM typically range from 25% to 45% from pro-rata controlling value. When owner dependency risk is added on top, the total impact on value can compound significantly.

The IRS scrutinizes these discounts closely. Appraisers must support each adjustment with empirical data and professional methodology.

How Can You Reduce Owner Dependency Before a Sale?

Reducing owner dependency takes time. The steps required to reduce the discount also make the business more profitable and more attractive to buyers.

David Hern brings a Heart of a Teacher to every client engagement. He does not just report the discount. He explains what is driving it and what an owner can do to close the gap before going to market. Consistent changes made over 12 to 24 months can shift a business from “high dependency” to “moderate” or even “low.”

The most effective steps include:

- Document all core business processes in writing, including pricing, client onboarding, and service delivery

- Hire or promote a second-in-command who can manage daily operations independently for at least 90 days

- Transition primary client relationships so at least two team members are named contacts on every major account

- Create an employee incentive plan that keeps key staff in place after a sale

- Build at least 12 months of consistent revenue performance not tied to the owner’s personal sales activity

A buyer or appraiser looks at the track record, not just the current state. A manager hired six weeks before listing carries little weight. One who has run operations for 18 months with documented results is a materially different story.

Frequently Asked Questions

What is owner dependency in a business valuation?

Owner dependency is a condition where a business’s revenue, client relationships, or operations rely heavily on a single owner. Appraisers treat it as a company-specific risk that reduces value. The more embedded the owner is in daily activities, pricing, and client management, the larger the discount applied. Reducing it before a sale is one of the most direct ways to increase concluded value.

How much is the owner dependency discount typically?

The discount typically ranges from 10% to 40% of enterprise value, though severe cases reach 50% when combined with other risk factors. The exact amount depends on how many dependency indicators are present, the business size, and industry norms. There is no fixed percentage. It is developed case by case, based on specific facts and documented with objective evidence.

How is the key person discount different from owner dependency?

The key person discount targets revenue or relationships tied to one individual. Owner dependency is broader and covers operational control, process gaps, and management bench strength. Both can apply to the same business at the same time. Key person adjustments also arise in life insurance planning and buy-sell valuations. Owner dependency is more commonly addressed in exit planning and transaction contexts.

What is a typical minority discount percentage?

A typical minority discount combines a DLOC of 15% to 25% with a DLOM of 15% to 30%, for a combined range of 25% to 45% from pro-rata controlling value. When owner dependency risk is also present, the total reduction can exceed 50%. Courts and the IRS require these discounts to be supported by empirical data and professional methodology.

How much is a business with $500,000 in sales worth?

A business with $500,000 in revenue might be worth $150,000 to $500,000 or more, depending on profit margin, growth trend, industry, and risk profile. Applying a 3.5x earnings multiple to a 20% SDE margin yields a base value of $350,000. An owner dependency discount of 20% to 35% reduces that to $227,500 to $280,000. Understanding your risk profile matters before setting a sale price.

How much does a business valuation from Sofer Advisors cost?

Our standard valuation typically ranges from $7,500 to $25,000, depending on engagement complexity, appraisal purpose, and business size. Most engagements are completed within four to eight weeks. Rush engagements are available at a 25% to 50% premium. Schedule a free consultation for a scoped estimate based on your situation and timeline.

Can owner dependency be reduced before a sale?

Owner dependency can be substantially reduced before a sale. It requires a deliberate plan and enough time for changes to show in the financial record. Most appraisers need 12 to 24 months of consistent results before they will materially reduce the discount. Key steps include hiring a management team, documenting processes, and transitioning client relationships.

Does owner dependency affect estate planning valuations?

Yes. In estate and gift tax valuations, owner dependency directly affects how appraisers split value between personal goodwill and enterprise goodwill. Personal goodwill is typically excluded from the taxable estate because it belongs to the individual, not the entity. A higher owner dependency finding often leads to a larger personal goodwill allocation. The appraiser’s methodology must meet Rev. Rul. 59-60 and Treasury Regulations.

What credentials should an appraiser have for this analysis?

An appraiser analyzing owner dependency should hold an ABV (Accredited in Business Valuation, issued by the AICPA) or an ASA (Accredited Senior Appraiser, issued by the American Society of Appraisers). These credentials require demonstrated experience, a written exam, and ongoing education. Both the IRS and FINRA recognize these designations. A CPA credential alone is not enough without one of these valuation-specific accreditations.

How do appraisers document the owner dependency discount?

Appraisers document owner dependency through management interviews, financial statement analysis, customer concentration data, and industry benchmark comparisons. The documentation appears in the company-specific risk section of the discount rate build-up or as a standalone discussion in the report. For IRS and litigation purposes, the report must explain what evidence was gathered, how factors were weighted, and how the adjustment was calculated.

Related Case Studies

- Selling A Business In Georgia Complete Exit Planning Guide 2026

- Personal Goodwill Vs Enterprise Goodwill Tax Divorce Guide

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

Executive Summary

Owner dependency and key person discounts are two of the most consequential risk adjustments in business valuation. Owner dependency addresses the broad operational risk when a business cannot function without its owner. The key person discount is narrower. It focuses on revenue tied to one individual. Both can apply to the same business. Both can materially reduce concluded value – often by 10% to 40%. Owners who understand these adjustments early achieve better outcomes in sales, estate transfers, and financing events.

What Should You Do Next?

If you are planning a sale, ownership transfer, or estate event in the next one to five years, get a baseline valuation now. This gives you an objective measure of where you stand. A value-building plan can then document your progress. It can confirm what those improvements are worth at the closing table. Do not wait until negotiations to discover a discount you could have spent two years reducing.

Schedule a consultation with David Hern CPA ABV ASA to find out where your business stands today.

People Also Read

- Small Business Valuation Georgia What Every Owner Should Know

- Eminent Domain Business Valuation Georgia Property And Business Owner Rights

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}