Last Updated: June 2026

This article is written for business partners, partnership attorneys, CPAs, and financial advisors. It explains how dissociation valuations work, which standards apply, and what drives the concluded number. After reading, you will be better equipped to navigate a partner exit with confidence.

A partnership dissociation valuation is a certified appraisal that finds the dollar value of a departing partner’s ownership interest on a set date. It matters because state partnership statutes – including the Revised Uniform Partnership Act (RUPA) – require a buyout price when a partner dissociates. That price must reflect the partner’s share of the firm’s going concern value or liquidation value. Real-world triggers include voluntary withdrawals, forced dissociations, partner deaths, and disputes that reach litigation.

When a partner exits, the remaining partners and the departing partner rarely agree on value. The gap between a self-calculated number and a defensible appraisal can run into the hundreds of thousands of dollars. Sofer Advisors, headquartered in Atlanta, GA, provides certified partnership valuations across the United States. The firm holds dual credentials recognized by the IRS, SEC, and FINRA. It also has 180+ five-star Google reviews backing every project.

Key Takeaways

- RUPA Governs Buyout Price in 37+ States – The Revised Uniform Partnership Act sets the default buyout as the greater of going concern value or liquidation value, measured on the dissociation date.

- Fair Value Differs from Fair Market Value – Dissociation cases use “fair value,” which does not deduct minority interest discounts or marketability discounts the way a standard fair market value appraisal does.

- Three Valuation Approaches Apply – Appraisers use the income approach, market approach, and asset approach, then compare them into a single concluded value.

- Partnership Agreements Can Override Statutes – A well-drafted agreement specifying the valuation method, standard of value, and dispute process often controls over state statute defaults.

- Goodwill Treatment Varies by State – Some states include enterprise goodwill in the buyout; others exclude all goodwill, making applicable jurisdiction a critical variable in every project.

- Credentialed Appraisers Are Essential for Court – Dissociation valuations used in litigation must be prepared by an ABV or ASA credentialed appraiser to withstand Daubert scrutiny.

These six factors shape every dissociation. The sections below examine each one in detail.

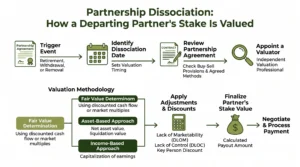

What Is Partnership Dissociation Under RUPA?

Partnership dissociation is the legal event that ends a partner’s association with an otherwise continuing firm. Under the Revised Uniform Partnership Act – codified in statutes like law.lis.virginia.gov – dissociation can be voluntary or involuntary. Each type is also classified as rightful or wrongful. Each category triggers different buyout rights.

A rightful dissociation entitles the departing partner to the buyout price within a reasonable time. A wrongful dissociation may give the firm the right to offset damages against the buyout. Courts decide which type applies. Appraisers find the dollar amount.

Going concern value assumes the firm continues operating. Liquidation value assumes assets are sold. For a business with positive cash flow, going concern value nearly always controls. The income or market approach then drives the result.

RUPA’s buyout provision is a default rule. Partners can modify it by specifying a formula, a fixed price, or a binding appraisal process.

What Standard of Value Applies in Dissociation?

The standard of value controls whether discounts apply. It is one of the most important decisions in a dissociation project.

Dissociation cases under RUPA typically apply fair value, not fair market value. Fair value is the partner’s proportionate share of total firm value – without minority or marketability discounts. A DLOC and a DLOM can reduce a small interest’s value by 30% to 50% under fair market value.

| Standard of Value | Minority Discount | DLOM Applied | Typical Use Case |

|---|---|---|---|

| Fair Market Value | Yes, 15-35% | Yes, 20-35% | Gift and estate tax, open market sale |

| Fair Value (RUPA default) | No | No | Partnership dissociation, minority oppression |

| Investment Value | No | No | Strategic M&A, acquirer-specific pricing |

| Intrinsic Value | No | No | Securities litigation, internal modeling |

A partner with a 25% interest in a $4 million firm receives $1 million under fair value. Under fair market value with a 30% DLOC and 25% DLOM, that same partner might receive $525,000. Confirm the applicable standard before engaging an appraiser.

How Do Appraisers Value a Partnership Interest?

Appraisers use three primary approaches: the income approach, the market approach, and the asset approach. Most dissociation valuations weight two or three and compare them into a single conclusion.

The income approach uses either a discounted cash flow (DCF) model or a capitalization of earnings method. For stable partnerships, capitalization of earnings is often best. For higher-growth firms, DCF holds up better in court. The market approach references EBITDA multiples from comparable deals or guideline public companies.

Key inputs an appraiser collects:

- Three to five years of partnership tax returns (Form 1065) and financial statements

- Partner capital account balances as of the dissociation date

- Any buy-sell agreement, partnership agreement, or operating agreement in effect

- Industry deal data and guideline public company financials

- Records of contingent liabilities, pending litigation, or off-balance-sheet items

Missing records are the most common source of delay. Most standard projects complete in four to eight weeks from receipt of complete papers.

Why Does the Partnership Agreement Matter?

A well-drafted partnership agreement is the single most effective tool for reducing the cost and time of a dissociation buyout. Most partners sign an agreement at formation and never revisit it.

The agreement can set the formula for the buyout price. Common approaches include book value per unit, a fixed multiple of last year’s earnings, or a binding appraisal process. Each removes uncertainty if agreed in advance.

The agreement can also set the standard of value. If it says “fair market value,” minority discounts apply. If it says “fair value,” no discounts apply. The dollar consequences can exceed the cost of a well-drafted agreement by a factor of 100 or more.

Courts consistently enforce partnership agreement valuation clauses unless they are unconscionable or violate public policy. Every partner should review the buyout provisions every three to five years.

How Does Goodwill Affect the Buyout Amount?

Goodwill is often the largest single component of a professional partnership’s value. For law firms, accounting practices, and consulting partnerships, goodwill may represent 60% to 80% of total enterprise value.

Enterprise goodwill is embedded in the firm’s systems, client relationships, and brand. It transfers with the entity and is generally included in a RUPA buyout as part of going concern value.

Personal goodwill is tied to the individual partner. When the partner leaves, personal goodwill leaves with them. Many courts exclude it from dissociation buyout calculations because remaining partners should not pay for value they will not receive.

David Hern CPA ABV ASA addresses this distinction in every professional practice dissociation project because it directly affects the conclusion.

What Role Does an Expert Play in Court?

When talks fail, the matter goes to court. Each side typically retains an independent appraiser to provide expert testimony. The expert’s credentials directly affect the outcome.

Under the Daubert standard, courts evaluate whether an expert’s method is sound before allowing testimony. The ABV from the AICPA Forensic and Valuation Services is one credential courts recognize. The ASA from the American Society of Appraisers is another. Both are accepted markers of qualified expert testimony.

The Sofer Difference is a four-phase process: Discovery, Diligence, Analysis, and Delivery. It is designed to produce a conclusion backed by every document a court might ask about. The written report records the method, data sources, and every adjustment to the reported financials.

David Hern brings a Heart of a Teacher approach to every project. He explains valuation methods in plain language. The partner, the attorney, and the court all understand how the number was reached.

The answers below reflect standard practice under RUPA and USPAP as of 2026.

Frequently Asked Questions

What is partnership dissociation valuation?

Partnership dissociation valuation is the process of finding the buyout price owed to a departing partner under state law. An appraiser calculates the partner’s proportionate share of going concern value or liquidation value, whichever is greater, as of the dissociation date. The analysis applies income, market, and asset approaches. The result is a solid conclusion accepted by courts, the IRS, and all parties.

How is the buyout price calculated under RUPA?

Under RUPA, the buyout price equals the greater of going concern value or liquidation value, multiplied by the partner’s ownership percentage. Going concern value uses standard business valuation approaches. Liquidation value is the net proceeds from an orderly asset sale. For a business generating positive earnings, going concern value nearly always controls.

Does fair value mean no minority discount applies?

Yes, in most dissociation cases. Fair value calculates the partner’s interest as a pro-rata share of total firm value without deducting a minority interest discount or a DLOM. Under fair market value, both discounts can reduce a minority interest’s value by 30% to 50%. The applicable standard is set by state statute and the partnership agreement.

How long does a partnership dissociation valuation take?

A standard certified dissociation valuation takes four to eight weeks from receipt of complete financial records. The timeline depends on partnership complexity and document turnaround from the partner and CPA. Rush projects complete in two to three weeks at a 25% to 50% premium. Court work requiring a full expert report may take 8 to 12 weeks under USPAP.

How much does a partnership dissociation valuation cost?

A partnership dissociation valuation from Sofer Advisors typically ranges from $7,500 to $25,000 depending on partnership complexity, purpose of the appraisal, and whether litigation support is required. Most standard projects complete within four to eight weeks. Rush work is available at a 25% to 50% premium. Schedule a free consultation to receive a scoped estimate within one business day.

What is the difference between dissociation and dissolution?

Dissociation is the departure of one partner from an otherwise continuing partnership. The firm keeps operating, the departing partner receives a buyout, and the remaining partners carry on. Dissolution is the winding up of the entire partnership. All partners exit, assets are liquidated or distributed, and the entity ends. The two events trigger different legal processes and different valuation standards in every state.

Can a partnership agreement override RUPA buyout rules?

Yes. RUPA’s buyout provisions are default rules that apply when the partnership agreement is silent. A properly drafted agreement can specify a different valuation formula, a different standard of value, a fixed price, or a binding appraisal process. Courts generally enforce these provisions unless they are unconscionable or contrary to public policy. Reviewing the buyout clause every three to five years is cost-effective risk management.

What happens if the partners disagree on buyout value?

When parties cannot agree, each side typically retains an independent appraiser. If the two appraisers reach different conclusions – which is common – a court evaluates both analyses and reaches a binding finding. Some partnership agreements include a third-appraiser mechanism where two party-appointed appraisers select a neutral third. The average of the two closest values then controls. Court-decided values often fall between the two expert opinions.

Does goodwill get included in a partnership buyout?

It depends on state law and the type of goodwill. Enterprise goodwill – value embedded in the firm’s systems, client base, and brand – is generally included in a RUPA buyout. Personal goodwill tied to the individual partner is often excluded because remaining partners should not pay for value they will not receive. Some states exclude all goodwill by statute, so jurisdiction review is essential.

What credentials should a partnership valuation expert have?

A qualified dissociation expert should hold the ABV credential from the AICPA or the ASA designation from the American Society of Appraisers – ideally both. These credentials require rigorous exams, experience standards, and ongoing education. Under Daubert, courts evaluate expert qualifications before allowing testimony. An appraiser with recognized credentials and prior court experience is far better positioned to withstand cross-examination than one without them.

Related Case Studies

- Selling A Business In Georgia Complete Exit Planning Guide 2026

- Personal Goodwill Vs Enterprise Goodwill Tax Divorce Guide

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

Executive Summary

Partnership dissociation valuation finds the buyout price owed to a departing partner under state law, typically RUPA. Appraisers apply income, market, and asset approaches to conclude the firm’s going concern value, then multiply by the partner’s ownership percentage. The standard of value – usually fair value, not fair market value – controls whether discounts apply, shifting the buyout amount by 30% to 50%. Goodwill treatment varies by state. An appraiser holding ABV or ASA credentials is essential for a conclusion that holds up in court.

What Should You Do Next?

Get a certified valuation before talks begin – not after they stall. Knowing the solid range of value gives both parties a clear starting point and reduces litigation risk. Review your partnership agreement’s buyout provisions now, before a dissociation event forces the issue on a compressed timeline.

David Hern CPA ABV ASA, founder of Sofer Advisors, works with partners, attorneys, and CPAs across the United States to produce certified, defensible dissociation valuations for negotiation, mediation, and court. Schedule a consultation to discuss your situation and receive a scoped estimate within one business day.

People Also Read

- Why You Must Start Planning Your Business Exit Now With The Right Valuation Expert

- What To Expect During A Business Valuation Step By Step Process

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}