Last Updated: June 2026

This article is written for medical spa owners, their CPAs, healthcare attorneys, and business brokers. It explains how valuations work, what multiples to expect, and how add-backs affect the final number.

A medical spa valuation is a certified, professional appraisal. It determines what a med spa is worth in dollar terms on a specific date. That number drives sale negotiations, partner buyouts, estate transfers, and SBA financing decisions. A credentialed appraiser reviews your adjusted earnings, recurring revenue mix, physician oversight structure, and comparable transaction data. The result is a defensible conclusion that buyers, lenders, and the IRS will accept.

When med spa owners decide to sell or plan their exit, the single biggest mistake they make is guessing at value. Multiples in this sector vary widely based on ownership structure, service mix, and how clean the books are. Sofer Advisors, headquartered in Atlanta, GA, provides certified business appraisals for medical spa owners across the United States. The firm combines 15+ years of healthcare valuation experience with a next business day response policy for every new inquiry.

Key Takeaways

- EBITDA Multiples Range from 3x to 7x – Medical spa EBITDA multiples typically fall between 3x and 7x depending on ownership structure, revenue mix, and practice size, with physician-owned practices generally commanding the higher end.

- Add-Backs Can Shift Value by Six Figures – Proper identification of owner add-backs, one-time expenses, and above-market owner pay can increase adjusted EBITDA by $50,000 to $200,000 in a mid-size practice.

- Recurring Revenue Commands a Premium – Med spas with high membership revenue, prepaid packages, and loyal patient bases trade at 0.5x to 1x higher multiples than single-visit-driven practices.

- Physician Oversight Affects Transferability – Practices structured around a physician medical director, rather than a single owner-physician, transfer more cleanly to buyers and often avoid restrictive covenant complications.

- Buyer Demand Is Strong in 2026 – Private equity groups, dental support organizations, and strategic acquirers are actively acquiring med spas, driving competitive bidding in markets with strong demographics.

- Credentials Matter for Tax and Legal Use – Valuations used in estate planning, shareholder disputes, or SBA financing must be prepared by an ABV (Accredited in Business Valuation) or ASA (Accredited Senior Appraiser) to meet IRS and lender standards.

The sections below examine each of these points in depth – covering multiples, add-back methodology, buyer demand, and what separates a high-value practice from a mid-market one.

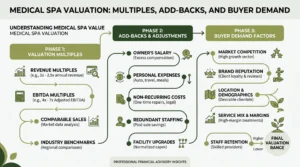

What Drives Medical Spa Valuation?

Medical spa valuation starts with adjusted EBITDA. That stands for earnings before interest, taxes, depreciation, and amortization. It is restated to reflect the true economic earnings a new owner would receive. That number is then multiplied by a market-derived multiple to produce enterprise value.

The IRS requires fair market value for estate and gift tax purposes – defined as the price a willing buyer and seller would agree on when neither is compelled and both have reasonable knowledge of the facts. For med spa transactions, fair market value is usually the right standard, though litigation and partner buyout contexts may apply other definitions.

Three variables drive the concluded value more than any others: adjusted EBITDA after proper add-backs, the multiple the market assigns based on practice characteristics, and transferability – whether the revenue survives when the owner leaves. A practice scoring well on all three is worth 5x to 7x EBITDA, while one scoring poorly on transferability may not exceed 3x even with strong earnings.

What Are Typical Med Spa EBITDA Multiples?

Med spa EBITDA multiples in 2026 typically range from 3.0x to 7.0x. The midpoint for a clean, well-structured practice lands between 4.0x and 5.5x. Sources including peakbusinessvaluation.com and focusbankers.com have tracked med spa transactions and consistently report this range for practices with $500,000 to $3 million in adjusted EBITDA.

High membership revenue is the most consistent premium driver. Practices where 30% or more of revenue comes from monthly memberships or recurring packages trade at higher multiples. Buyers can model predictable cash flow. A diversified service mix – injectables, laser treatments, body contouring, and wellness services – also reduces concentration risk.

| Practice Characteristic | Typical Multiple Range |

|---|---|

| Single-service, owner-dependent practice | 2.5x – 3.5x EBITDA |

| Multi-service, some recurring revenue | 3.5x – 4.5x EBITDA |

| Strong membership base, medical director model | 4.5x – 5.5x EBITDA |

| Multi-location, recurring revenue, PE-ready | 5.5x – 7.0x EBITDA |

Most independent med spa owners will transact in the 3.5x to 5.5x range. Building toward the top of that band is the most reliable path to a better outcome. A certified valuation reveals exactly where your practice sits today and what is holding the multiple back.

How Do Add-Backs Work in a Med Spa Sale?

Add-backs are adjustments to reported net income that normalize earnings to reflect what a new owner would actually earn. They are one of the most contested parts of any healthcare business sale, and med spas tend to have above-average complexity because owner pay structures vary significantly. Identifying every legitimate add-back requires a careful review of three to five years of tax returns, P&L statements, and bank records.

The most frequently identified add-back categories for med spa valuations include:

- Owner pay above market rate for the role actually performed

- Personal vehicle, travel, and entertainment expenses on the business books

- One-time costs such as lease renegotiation fees, rebranding, or litigation expenses

- Above-market rent paid to an owner-related real estate entity

- Non-cash expenses including deferred rent adjustments

Buyers and their advisors will scrutinize every add-back. The American Society of Appraisers requires its members to document and support every adjustment with contemporaneous evidence. An add-back that cannot be supported with documentation gets disallowed.

Why Does Ownership Structure Matter for Value?

Ownership structure is one of the most overlooked value drivers in a medical spa sale. The core question is whether the business can generate its current revenue without you – if not, buyers assign a risk premium that reduces the multiple.

A practice built around a single owner-physician who performs most revenue-generating services is difficult to transfer. The buyer must either retain you under an employment agreement or risk patient attrition. Many buyers price that risk by applying a key person discount. That discount can reduce enterprise value by 20% to 35%.

The solution is a medical director model. A med spa structured so that a contracted physician handles medical oversight while non-physician staff deliver most services transfers more cleanly. The buyer acquires the revenue stream, patient relationships, systems, and brand – not a dependency on one individual.

Personal goodwill is the value tied to the individual owner that cannot transfer in a sale. Enterprise goodwill is the value embedded in the brand, systems, and patient base that does transfer. David Hern CPA ABV ASA addresses this distinction in every medical spa engagement because it directly affects both concluded value and transaction structure.

How Does Buyer Demand Affect Med Spa Prices?

Buyer demand for medical spas has increased significantly over the past three years. Private equity groups that initially targeted dental practices and dermatology groups began pursuing med spas around 2021, and that interest has not slowed.

Competitive processes with multiple buyers consistently produce higher outcomes than single-buyer conversations. A practice that receives three letters of intent at the same time is in a fundamentally stronger negotiating position than one negotiated with a single acquirer.

PE buyers model cash flow over a three to five year hold period. A med spa generating $400,000 per year from memberships and prepaid packages gives a buyer much more confidence in projected earnings. That confidence translates directly into a higher offer multiple.

What Regulatory Issues Affect Med Spa Value?

Regulatory compliance is not just an operational concern. It directly affects valuation. A med spa with unresolved compliance exposure faces two problems. First, lower buyer confidence. Second, post-closing indemnity risk that reduces the effective purchase price through escrow holdbacks or price adjustments.

The Stark Law prohibits physician self-referrals for designated health services. The Anti-Kickback Statute prohibits payments for referrals in federal healthcare programs. Practices that offer any services reimbursed by federal programs must have compliant pay arrangements. Buyers’ legal teams review this in diligence.

State medical practice acts also govern which services a non-physician owner can direct and which require physician supervision. These rules vary by state and have changed in several markets over the past two years. A corporate practice of medicine (CPOM) structure that was compliant three years ago may require review today. Non-compliance gives buyers a negotiating advantage and can delay closing by 30 to 60 days.

How Do You Prepare a Med Spa for a Higher Value?

Preparing a med spa for a certified valuation and eventual sale is not a last-minute project. The actions that most consistently increase value take 12 to 36 months to implement and reflect in the financial record.

Clean financials are the starting point. If owner expenses are mixed with business expenses, the add-back process becomes contentious and some adjustments get disallowed. Separating personal from business expenses two or three years before a sale makes a meaningful difference.

Building recurring revenue is the highest-return investment most med spas can make. A membership program that converts 15% to 20% of patients to monthly members can add $80,000 to $150,000 in annual recurring revenue. At a 5x multiple, that is $400,000 to $750,000 in additional enterprise value.

Documenting systems and protocols is also important. A buyer who sees a well-documented patient acquisition process, a trained clinical team, and a marketing program that does not depend on the owner’s personal social media presence will pay more.

These preparation steps push a practice from a 3.5x multiple to a 5.0x multiple. The difference on a $1 million EBITDA practice is $1.5 million in additional proceeds.

The questions below address the most common topics med spa owners raise when they first contact a valuation firm. These answers reflect the state of the market in 2026 and draw on real engagement experience rather than theory.

Frequently Asked Questions

How to value a med spa?

Valuing a medical spa starts with calculating adjusted EBITDA – restated net income after adding back owner pay above market, personal expenses, and one-time costs. An appraiser then applies a market-derived multiple, typically 3.0x to 7.0x, based on practice size, revenue mix, ownership structure, and transferability.

How much money does a med spa owner make?

Most mid-size medical spas with $1 million to $3 million in revenue generate $200,000 to $600,000 in owner pay and distributions annually. Membership-heavy practices and lean staffing models tend toward the high end of that range.

How profitable is a medical spa?

Medical spas typically show EBITDA margins of 20% to 35% of gross revenue for well-run practices. Profitability improves sharply when the owner reduces personal service delivery and builds recurring membership revenue.

How much does a medical spa valuation from Sofer Advisors cost?

A healthcare practice valuation from Sofer Advisors typically ranges from $10,000 to $30,000 depending on practice size, appraisal purpose, and number of locations. Schedule a free consultation to receive a scoped estimate within one business day.

What is the difference between enterprise value and equity value in a med spa sale?

Enterprise value is the total value of the operating business including any debt. Equity value is what the seller receives after debt is paid at closing. For most transactions, the parties agree on enterprise value first, then adjust for cash, debt, and normalized working capital to arrive at final proceeds.

What multiple of revenue do medical spas sell for?

Revenue multiples for medical spas typically range from 0.5x to 2.0x gross revenue, but EBITDA-based multiples are the primary valuation method because they account for differences in profitability that revenue multiples obscure.

Does a medical spa need a physician owner to sell?

No. Medical spas can be owned by non-physicians in most states through a management services organization (MSO) or similar structure, as long as a licensed physician serves as medical director and retains clinical oversight.

What is personal goodwill and why does it matter in a med spa valuation?

Personal goodwill is the portion of practice value tied to the individual owner that cannot transfer in a sale. Enterprise goodwill is the portion embedded in the brand, systems, and patient base that does transfer. Reducing personal goodwill before a sale directly increases the achievable purchase price.

How long does a medical spa valuation take?

A standard certified valuation takes four to eight weeks from the date financial documents are received. Rush engagements are completed in two to three weeks at a 25% to 50% premium.

Are there AICPA or USPAP standards for medical spa valuations?

Yes. Certified appraisers follow the Uniform Standards of Professional Appraisal Practice (USPAP), endorsed by the AICPA Forensic and Valuation Services for business valuation engagements. Valuations used in IRS submissions, SBA loan applications, or litigation must be prepared by a credentialed appraiser to avoid being challenged and rejected.

Related Case Studies

- Medical Practice Valuation Atlanta Healthcare Sale Transition Guide

- Personal Goodwill Vs Enterprise Goodwill Tax Divorce Guide

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

Executive Summary

Medical spa valuation in 2026 is driven by three variables: adjusted EBITDA after proper add-backs, the market multiple assigned based on practice characteristics, and transferability of the revenue base. EBITDA multiples typically range from 3.0x to 7.0x, with the midpoint for a clean practice landing between 4.0x and 5.5x. Recurring membership revenue, a medical director ownership model, and documented systems support higher multiples. Regulatory compliance under the Stark Law, Anti-Kickback Statute, and state CPOM rules directly affects buyer confidence and purchase price.

What Should You Do Next?

If you own a medical spa and are considering a sale, planning your estate, or need a valuation for a partner buyout or SBA financing, the best time to get a certified appraisal is before your event – not during it. Understanding your value today gives you 12 to 36 months to implement changes. Those changes can move your practice from a 3.5x to a 5.0x multiple. On a $500,000 EBITDA practice, that is $750,000 in additional proceeds.

David Hern CPA ABV ASA, founder of Sofer Advisors, works with medical spa owners, healthcare attorneys, and CPAs across the United States. He produces certified, defensible valuations for every purpose – transactions, estate planning, partner buyouts, and litigation support. Schedule a consultation to discuss your situation and receive a scoped estimate within one business day.

People Also Read

- Medical Practice Valuation Multiples 2026 2027 Complete Atlanta Guide

- Medical Practice Valuation Multiples 2025 2026 Complete Guide

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}