Last Updated: June 2026

This article is for business owners, estate attorneys, and CPAs who need to understand IDGT sales. After reading, you will know which discounts apply, what the IRS requires, and how to choose a qualified appraiser.

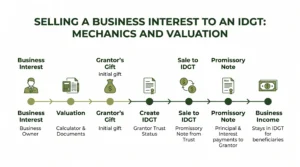

An intentionally defective grantor trust valuation is the formal process of finding the fair market value of a business interest sold to an IDGT. An IDGT is a trust that sits outside your taxable estate for estate tax but stays inside for income tax. The grantor pays income tax on trust earnings, shrinking the estate without any gift tax cost. The sale transfers a business interest at a discounted value, locking in today’s price and shifting future growth to your heirs.

Why does this matter? Business owners use IDGT sales to shift wealth without triggering gift taxes. The IRS requires a qualified appraisal to support every IDGT sale price. Without one, the IRS can recast the transaction as a taxable gift. Sofer Advisors, headquartered in Atlanta, GA, provides IDGT appraisals for middle-market owners across the United States, with dual ABV and ASA credentials recognized by the IRS, SEC, and FINRA.

Key Takeaways

- IDGT Split Treatment – The trust is defective for income tax but valid for estate tax, so income tax payments reduce the estate without triggering gift tax.

- No Capital Gains on Sale – The IRS treats the grantor and trust as one taxpayer. No capital gains apply on the installment sale.

- Valuation Discounts Apply – DLOM of 15-35% and a minority discount of 15-30% often cut the transfer value by 20-40%.

- Qualified Appraisal Required – Treasury Regulation 1.170A-17 requires a qualified appraisal from a credentialed appraiser to support the sale price.

- Estate Freeze Benefit – All future appreciation on the transferred interest grows outside the taxable estate, saving estate taxes over time.

The sections below examine how each element works and where valuation plays a central role.

What Is an IDGT and How Does It Work?

An intentionally defective grantor trust is an irrevocable trust that removes assets from your taxable estate while keeping you as the income taxpayer. The “defect” is intentional. For estate tax, assets leave your estate. For income tax, the IRS treats you as the owner under grantor trust rules.

This split is the core of the strategy. You pay income tax on trust earnings, which reduces your estate without triggering gift tax. Trust beneficiaries receive those earnings with no income tax cost to them.

The mechanics involve two steps. First, you make a seed gift to the trust equal to at least 10% of the assets you plan to sell. This establishes that the trust has real equity. Second, you sell a business interest to the trust in exchange for a promissory note at or above the Applicable Federal Rate (AFR). Because you and the trust are the same taxpayer for income tax, the sale triggers no capital gains.

Firms like nationaladvisors.com and saul.com serve business owners using IDGT structures as part of broader estate planning. A qualified appraisal is the foundation that makes the structure hold up when the IRS reviews it.

How Is the Business Interest Valued for Sale?

Valuing a business interest for an IDGT sale follows standard fair market value methodology. Fair market value is the price a willing buyer and willing seller would agree on. This standard comes from Revenue Ruling 59-60, the foundational IRS guidance for business appraisals.

Three approaches apply to most closely held businesses.

- Income Approach – Values the business based on future cash flow discounted to present value. Best for operating businesses with stable earnings.

- Market Approach – Uses EBITDA multiples from comparable private sales and guideline public companies.

- Asset Approach – Values net assets at fair market value. Used for holding companies where asset value exceeds earnings value.

After finding enterprise value, the appraiser applies entity-level discounts. A minority interest in a closely held LLC receives a DLOC, the reduction a buyer applies because the holder cannot direct company decisions. It also receives a DLOM, reflecting no liquid market for the shares.

These discounts often reduce value by 20% to 40%. On a $10 million enterprise with a 30% interest and a 35% combined discount, the appraised value drops from $3 million to roughly $1.95 million. Sofer Advisors supports every discount with data from restricted stock studies and closed transaction databases.

Which Discounts Apply in an IDGT Transfer?

Discounts are the primary lever that makes an IDGT sale efficient. The IRS challenges unsupported discounts in gift tax audits. The burden of proof rests with the taxpayer.

DLOC reflects the reality that a minority holder cannot control distributions or force a sale. Closed transaction studies support DLOC ranges of 15% to 35%, depending on governance documents and economic rights.

DLOM reflects the cost and delay of selling a closely held interest. No public market exists for shares in a family LLC. Restricted stock studies support DLOM ranges of 15% to 35%. Appraisers document DLOM using the Mandelbaum factors, which weigh 10 elements including financial statement quality and the prospect of future liquidity.

The table below shows a simple example for a 30% minority interest in a $5 million enterprise.

| Step | Value |

|---|---|

| Enterprise Value | $5,000,000 |

| Pro-Rata Share (30%) | $1,500,000 |

| Minus DLOC (20%) | ($300,000) |

| Minus DLOM (25%) | ($300,000) |

| Appraised Value of Interest | $900,000 |

This table shows how discounts reduce the transfer value. The note drops from $1.5 million to $900,000. That $600,000 reduction lowers gift tax exposure. Firms like gsrm.com also serve this market. Discount quality varies widely, so confirm your appraiser holds a recognized credential and documents discounts with cited data.

What IRS Rules Govern IDGT Valuations?

The IRS does not have one regulation covering every IDGT installment sale. Practitioners rely on a framework from several guidance documents and statutes.

Revenue Ruling 59-60 defines the standard for valuing closely held business interests. It lists eight factors appraisers must consider, including earnings history, dividend capacity, book value, and the economic outlook.

Revenue Ruling 2004-64 confirms that a grantor’s payment of income tax on trust earnings does not create a taxable gift. This protects the income tax depletion benefit that makes IDGT sales efficient.

IRC Section 7872 requires the promissory note to carry interest at or above the AFR. A below-AFR rate creates an imputed gift, reducing the grantor’s lifetime exemption.

Treasury Regulation 1.170A-17 defines the qualified appraisal rules. The appraiser must hold a recognized credential such as ABV from the AICPA Forensic and Valuation Services division or ASA from the American Society of Appraisers. The appraisal must conform to USPAP (Uniform Standards of Professional Appraisal Practice). Penalties under IRC Section 6662 for valuation misstatements reach 20% to 40% of the understated tax. A USPAP-compliant appraisal grounded in Revenue Ruling 59-60 gives every IDGT transaction its strongest IRS defense.

When Should You Start the IDGT Valuation Process?

Timing is the most underestimated factor in IDGT planning. Many owners wait until the estate attorney drafts the trust before engaging an appraiser. By then, the structure is often set in ways that limit valuation options. Engage a qualified appraiser before the trust is drafted.

Early appraisal input helps attorneys see which discount levels are supportable. That shapes which interests to transfer and what note term fits the business. Allow at least 60 to 90 days from engagement to final report. Rushing creates documentation gaps the IRS can exploit.

David Hern CPA ABV ASA, founder of Sofer Advisors brings a Heart of a Teacher to every IDGT engagement. He explains valuation timing, discount levels, and estate tax savings in plain terms that owners and advisors can act on. This reflects The Sofer Difference, a four-phase process of Discovery, Diligence, Analysis, and Delivery. Every engagement follows that process from the first document review to the final qualified written report, ensuring discounts are supported and the timeline aligns with the attorney’s schedule.

The questions below address the details that come up most often in IDGT practice.

Frequently Asked Questions

What is an intentionally defective grantor trust valuation?

An intentionally defective grantor trust valuation is a formal appraisal of a business interest sold to an IDGT. The appraiser finds the fair market value of the specific ownership interest. That value sets the promissory note size and protects the transaction from IRS gift tax challenges. The appraiser applies income, market, and asset approaches to reach enterprise value, then adjusts for discounts including lack of control and lack of marketability.

How much does an IDGT valuation from Sofer Advisors cost?

An IDGT business interest valuation from Sofer Advisors typically ranges from $7,500 to $25,000, depending on business complexity and the depth of discount analysis required. Most standard engagements complete within four to eight weeks from receipt of financial documents. Rush engagements are available at a 25% to 50% premium. Schedule a free consultation to receive a scoped estimate for your specific transaction.

What is the 10% seed gift rule for IDGTs?

The trust must hold equity equal to at least 10% of the sale price before the installment sale closes. This rule prevents the IRS from treating the transaction as a gift. The seed gift is typically funded with cash or assets already outside the business. Without adequate trust equity, the IRS can recast the transaction and assess gift tax on the full transferred value. Most attorneys build in a buffer above 10% to reduce audit risk.

What is the Applicable Federal Rate and why does it matter?

The Applicable Federal Rate (AFR) is the minimum interest rate the IRS sets monthly for related-party loans. In an IDGT sale, the promissory note must carry interest at or above the AFR on the sale date. If the note rate falls below AFR, the IRS imputes the shortfall as a taxable gift, reducing the grantor’s lifetime exemption. The IRS publishes AFR tables monthly in Revenue Rulings.

Can DLOM and DLOC be applied together in an IDGT sale?

Yes, appraisers apply both DLOM and DLOC when facts support them, sequentially. DLOC is applied first to enterprise value to produce a minority interest value. DLOM is then applied to reflect the absence of a liquid market. Combined discounts typically range from 20% to 40%, depending on interest size and governing documents. Each discount must be supported by empirical data and cited studies in the qualified appraisal report.

What happens to the IDGT if the grantor dies before the note is paid?

If the grantor dies while the note is outstanding, the unpaid balance is included in the grantor’s gross estate. Trust assets are not included because the sale was a bona fide arm’s-length transaction. Planners often carry life insurance on the grantor to cover the note payoff without forcing a business sale. Appreciation inside the trust still passes to beneficiaries outside the estate, so the core planning benefit is largely preserved.

How does an IDGT sale compare to a GRAT for business transfer?

Both tools shift appreciation to heirs outside the taxable estate. A GRAT requires fixed annuity payments for a set term and fails if the grantor dies during that term. An IDGT sale uses a promissory note with flexible terms and benefits from valuation discounts that a GRAT does not receive. For closely held interests with strong discount potential, IDGT sales typically produce larger wealth transfers. Your attorney and CPA should model both before choosing.

What qualifications must an IDGT appraiser hold?

An IDGT appraiser must qualify under Treasury Regulation 1.170A-17. Required credentials include ABV from the AICPA or ASA from the American Society of Appraisers, verifiable experience with the property type, and a fee not contingent on the outcome. The appraiser must be independent from the taxpayer. Sofer Advisors holds dual ABV and ASA credentials recognized by the IRS, SEC, and FINRA and operates under USPAP-compliant standards.

Related Case Studies

- Why You Must Start Planning Your Business Exit Now With The Right Valuation Expert

- What To Expect During A Business Valuation Step By Step Process

- Estate Planning Business Valuation Georgia Gift Tax Compliance Guide

Executive Summary

An IDGT sale moves a business interest out of your taxable estate at a discounted value. You sell the interest to the trust in exchange for a promissory note at the AFR. Because the trust is defective for income tax, no capital gains apply on the sale. A qualified appraiser applies DLOC and DLOM to reduce the transfer value. All future appreciation grows outside the estate. IRS compliance requires a qualified appraisal following Revenue Ruling 59-60 and Treasury Regulation 1.170A-17. Timing, discount support, and documentation determine whether the plan holds under audit.

What Should You Do Next?

Gather three to five years of financial statements and your entity’s operating agreement. Share those with your estate attorney and a qualified appraiser before the trust is drafted. The earlier the appraiser reviews the structure, the more options are available to your planning team.

David Hern CPA ABV ASA, founder of Sofer Advisors has completed IDGT appraisals for middle-market owners across the United States, with 180+ five-star Google reviews and dual ABV and ASA credentials.

SCHEDULE A CONSULTATION to discuss your IDGT valuation and protect your estate plan with a defensible, IRS-compliant appraisal.

People Also Read

- Why You Must Start Planning Your Business Exit Now With The Right Valuation Expert

- What To Expect During A Business Valuation Step By Step Process

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}