Last Updated: April 2026

Normalized EBITDA is a measure of a business’s recurring earnings after removing owner-specific compensation, one-time expenses, and non-recurring items that would not transfer to a buyer. It starts with EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) and applies adjustments to reflect what a hypothetical arm’s-length buyer would actually acquire. According to the AICPA Business Valuation Standards (2023), sustainable earnings capacity is the central input for income-based valuations and must reflect normalized, going-concern operations.

At Sofer Advisors, we prepare normalized EBITDA schedules for business sales, partner buyouts, and ESOP transactions. An overstatement invites buyer pushback during due diligence; an understatement leaves value on the table. Defensible adjustments with documentation behind each line are what keep a deal from collapsing at the quality-of-earnings stage.

Owners approaching a sale or ownership transition need to understand what appraisers and buyers will adjust, how those adjustments affect the multiple, and which items the other side will contest. The sections below cover each component in the order appraisers follow.

Key Takeaways

- Definition – normalized EBITDA starts with EBITDA and removes owner pay above a market replacement rate, personal expenses, and one-time items to isolate recurring earnings that transfer to a buyer.

- Formula – Normalized EBITDA = EBITDA + owner compensation adjustment + personal expense addbacks + one-time cost addbacks – one-time revenue items +/- rent normalization.

- Typical Adjustment – normalization commonly adds 15 to 40 percent to reported EBITDA in closely held businesses where owner compensation exceeds a market replacement salary.

- Buyer Application – buyers apply an industry multiple (3x to 7x EBITDA for the lower middle market) to normalized EBITDA to arrive at enterprise value.

- Limitation – a single year of normalized EBITDA can misrepresent performance; appraisers typically weight a 3-to-5-year trailing average to reflect sustained earnings power.

Each of these components interacts with how the valuation multiple is applied. The sections below examine each in detail.

What Is Normalized EBITDA?

Normalized EBITDA is a version of EBITDA that strips out earnings distortions tied to the current owner: compensation above a market replacement salary, personal expenses run through the business, and one-time or non-recurring items that would not continue under new ownership. The result reflects what the business would earn under a hypothetical arm’s-length buyer at market-rate costs. It is the standard earnings base for income-approach and market-approach valuations in M&A and appraisal.

The distinction matters because reported EBITDA in a closely held company almost always reflects the owner’s personal financial decisions as much as business performance. An owner paying themselves $800,000 in a market where a replacement manager costs $250,000 is suppressing reported EBITDA by $550,000. A buyer at 5x EBITDA loses $2,750,000 in value if that adjustment is missed. Normalization corrects these distortions so the multiple reflects the business’s earning power as a going concern, not the current owner’s choices.

How Is Normalized EBITDA Calculated?

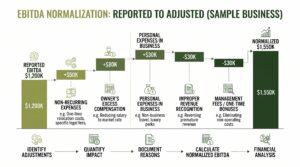

Normalized EBITDA is calculated by starting with reported net income, adding back interest, taxes, depreciation, and amortization to reach EBITDA, then applying owner-specific and non-recurring adjustments line by line. Each adjustment adds to or subtracts from reported EBITDA based on whether the item is owner-specific, non-recurring, or not priced at arm’s-length terms. Appraisers document every line with supporting data because buyers and their advisors scrutinize each adjustment during quality-of-earnings diligence.

The standard calculation follows four steps:

- Start with net income and add back ITDA – add interest, income taxes, depreciation, and amortization to reach baseline EBITDA for the trailing twelve months or weighted average period

- Owner compensation adjustment – compare actual owner draw, salary, and benefits to a market-rate replacement manager; add the excess back with W-2 and compensation survey support

- Personal expenses and non-arm’s-length items – identify owner personal costs (personal vehicle, family health insurance, personal travel, above-market family payroll) and add them back with receipt documentation

- One-time and non-recurring items – remove one-time revenue such as PPP loan forgiveness or single-year government grants; add back one-time costs such as legal settlements or extraordinary repairs not representing run-rate operations

According to the Pepperdine Private Capital Markets Report (2024), lower middle market transactions close at 3x to 6x normalized EBITDA depending on industry and customer concentration, making normalization accuracy proportional to seller proceeds. An error of $200,000 in the normalized figure translates to $600,000 to $1.2 million in lost enterprise value at a 3x to 6x multiple, which is why buyers commission a quality of earnings review to independently verify each adjustment before committing to a purchase price.

What Adjustments Are Included in Normalized EBITDA?

Normalized EBITDA adjustments cover four categories: owner-specific compensation, personal use of business resources, non-recurring revenue and cost items, and related-party transactions not priced at arm’s length. The scope of each depends on the company’s financial structure, the owner’s role in daily operations, and industry norms. Appraisers review three to five years of financials to identify patterns before committing to any adjustment.

| Adjustment Category | Common Examples | Direction |

|---|---|---|

| Owner compensation | Salary and distributions above market replacement CEO rate | Add back excess |

| Personal expenses | Personal vehicle, family health insurance, personal travel | Add back |

| One-time revenue | PPP loan forgiveness, single-year government grants | Subtract |

| One-time costs | Legal settlements, major non-recurring repairs | Add back |

| Related-party rent | Owner-occupied property leased below or above market | Normalize to market rate |

| Non-arm’s-length transactions | Family member salaries above market, related-party vendor pricing | Adjust to arm’s length |

The owner compensation adjustment is typically the largest single item. IRS Revenue Ruling 59-60 establishes that fair market value determinations assume a competent management team hired at market compensation, not the prior owner’s pay structure. Published compensation surveys are the standard method for documenting this adjustment under buyer scrutiny, and appraisers typically benchmark owner draws against industry-specific executive pay data from sources such as the Economic Research Institute or Mercer to compute a defensible excess compensation addback.

How Do Normalized and Adjusted EBITDA Differ?

Normalized EBITDA and adjusted EBITDA are related but serve different purposes and different audiences. Normalized EBITDA is used in M&A and business appraisal to represent recurring earnings that transfer to a new owner; every adjustment is evaluated against what a hypothetical buyer would actually experience. Adjusted EBITDA is a broader, non-GAAP term used by public companies, private equity portfolio reporting, and lenders to remove items management considers non-representative of core operations, including stock-based compensation, restructuring charges, and integration costs.

| Factor | Normalized EBITDA | Adjusted EBITDA |

|---|---|---|

| Primary context | M&A, business appraisal | Public company reporting, PE portfolio |

| Key adjustments | Owner comp, personal expenses, one-time items | Stock compensation, restructuring, M&A costs |

| Governing standard | AICPA valuation standards, USPAP | SEC non-GAAP disclosure rules |

| Audience | Buyers, appraisers, lenders | Investors, analysts, boards |

| Subjectivity | High (judgment on transferability to buyer) | Moderate (disclosed in SEC filings) |

Closely held businesses use the two terms interchangeably. In a formal valuation, the governing concept is always normalization: what would this business earn under hypothetical arm’s-length ownership? That question controls every adjustment decision. Buyers who see an “adjusted EBITDA” in a seller’s memorandum will run their own normalization analysis to confirm how the measures diverge. Sellers who build a well-documented normalization schedule with three years of prior-period comparatives before going to market tend to close faster, retain more of the agreed purchase price, and face fewer adjustments during the buyer’s quality of earnings process.

How Do Buyers Use Normalized EBITDA?

Buyers use normalized EBITDA as the base against which an industry transaction multiple is applied to arrive at enterprise value. The multiple reflects what comparable businesses in the same sector and size range have sold for on a normalized basis, drawn from private transaction databases and, where available, public company data. Applying the right multiple to a correctly normalized EBITDA produces a defensible value range both sides can negotiate against.

The practical sequence a buyer follows when evaluating a target includes four steps:

- Review the seller’s normalization schedule – assess each adjustment for documentation, business justification, and consistency across prior years; flag unsupported items for further diligence

- Commission a quality of earnings report – an independent CPA firm validates or disputes seller adjustments by testing bank statements, payroll, and expense records against the claimed addbacks

- Apply haircuts to contested adjustments – items without adequate documentation are reduced or removed, lowering normalized EBITDA and, with it, the offer price at any given multiple

- Triangulate with a DCF analysis – most institutional buyers cross-check the multiple-based value against a discounted cash flow model using normalized earnings as the base

Sofer Advisors, with ABV and ASA accreditations recognized by the IRS and SEC, prepares independent normalization analyses that document each adjustment for buyer review. Firms such as Stout and Kroll perform the same role in institutional-scale M&A. In each case, the value of the independent analysis comes from its defensibility: a normalization schedule produced by a credentialed appraiser carries more weight in quality of earnings diligence than one assembled by the seller’s internal accounting team without independent verification.

What Are the Limits of Normalized EBITDA?

Normalized EBITDA has three structural limits buyers and appraisers must account for before using it as the primary valuation input. It omits capital expenditure requirements: two businesses with identical normalized EBITDA but different capex needs will have different economic returns. Normalization is also subjective: two qualified appraisers reviewing the same financials may reach different totals based on differing judgments about what is recurring. A single-year figure can overstate value at a cyclical peak or understate it at a trough.

The three scenarios where normalized EBITDA produces the most distorted picture are:

- Capital-intensive operations – manufacturing, healthcare practices, and construction companies with significant equipment or facility requirements need a free cash flow analysis alongside EBITDA multiples to capture true economic return after reinvestment costs

- Cyclical or concentrated revenue – a business at a revenue peak will show inflated normalized EBITDA; applying a multiple to peak-year earnings prices in mean reversion risk that surfaces as a purchase price reduction or earnout

- Aggressively normalized schedules – when a seller adds back items buyers consider recurring, the gap between ask and bid can stall a transaction or shift deal structure toward earnouts and seller notes

These limits are why experienced appraisers apply normalized EBITDA multiples alongside a discounted cash flow analysis. In capital-intensive industries, a debt-free, cash-free net asset analysis is added as a third anchor to produce a supportable value range. Triangulating across three methodologies reduces the risk that any single approach’s structural weakness distorts the final opinion, and gives both buyers and sellers a defensible range to negotiate within rather than a single-point estimate that either party can challenge.

Frequently Asked Questions

What is normalized EBITDA in simple terms?

Normalized EBITDA is the recurring profit a business would generate under a new arm’s-length owner once the current owner’s personal pay above a market rate, personal expenses, and one-time costs are removed. Most closely held businesses show a normalized EBITDA higher than their reported net income because owners have legitimate reasons to minimize taxable income through compensation and expense decisions that disappear when the business transfers.

How is normalized EBITDA different from EBITDA?

EBITDA removes interest, taxes, depreciation, and amortization from net income to approximate cash operating earnings. Normalized EBITDA then applies a second layer of adjustments for owner-specific factors, personal expenses, and non-recurring items. EBITDA reflects what the business reported; normalized EBITDA reflects what it would have generated under arm’s-length operations. For closely held companies, the gap is often 15 to 40 percent of reported EBITDA.

What is the normalized EBITDA formula?

The formula is: Normalized EBITDA = Net Income + Interest + Taxes + Depreciation + Amortization + Owner Compensation Adjustment + Personal Expense Addbacks + One-Time Cost Addbacks – One-Time Revenue Items +/- Rent Normalization. Each addback requires documentation, including W-2s, payroll records, expense reports, and third-party compensation benchmarks. The result is typically expressed as a trailing-twelve-month figure or a weighted average of three to five years.

What multiple is applied to normalized EBITDA?

Multiples vary by industry and company size. Lower middle market businesses (under $10 million EBITDA) typically trade at 3x to 6x. Upper middle market companies ($10 million to $50 million) often attract 5x to 8x. High-growth businesses with recurring revenue and strong margins may command premiums above those ranges. The appropriate multiple comes from comparable private transactions and, where relevant, public company trading data from the same sector.

How much does a business valuation cost?

A business valuation that includes a normalized EBITDA analysis and a formal appraisal report typically costs $7,500 to $25,000 depending on company complexity, the number of adjustments required, the purpose of the engagement, and whether litigation support is needed. Engagements involving regulatory compliance or contested adjustments sit at the upper end. Turnaround is generally four to eight weeks from receipt of all financial materials. Contact Sofer Advisors to scope your engagement.

What is a quality of earnings report and how does it relate to normalized EBITDA?

A quality of earnings (QoE) report is an independent analysis commissioned by the buyer that tests the seller’s normalized EBITDA schedule by tracing each adjustment to supporting documentation. The QoE team reviews bank statements, payroll records, and expense detail to confirm or dispute each addback. Items that fail are reduced or removed, lowering the normalized EBITDA used in the offer calculation. A well-documented normalization schedule prepared in advance reduces QoE surprises.

When should a business owner calculate normalized EBITDA?

An owner should build a normalized EBITDA schedule two to three years before a planned sale, ESOP transaction, or partner buyout. Early preparation allows operational changes, such as restructuring compensation or eliminating personal expenses, that improve the figure on a multi-year basis. A single peak year is discounted by buyers; three consecutive years of similar performance is treated as evidence of sustained earnings capacity.

Does normalized EBITDA account for capital expenditures?

Normalized EBITDA does not account for capex requirements. It adds back depreciation as a non-cash charge, but depreciation proxies future asset replacement costs. Appraisers working with manufacturing, healthcare, or equipment-heavy companies often use EBITDA minus maintenance capex alongside normalized EBITDA to capture true economic return. Buyers in these sectors apply lower multiples because of the embedded reinvestment obligation.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

Normalized EBITDA adjusts reported earnings for owner-specific compensation, personal expenses, and non-recurring items to isolate the sustainable earnings a buyer is acquiring. It is the standard base for EBITDA multiple valuations in M&A and appraisal. The formula adds back excess owner pay and one-time costs, then removes non-recurring revenue. Its primary limit is omitting capital expenditure requirements, which is why appraisers cross-check normalized EBITDA against a discounted cash flow analysis. A documented normalization schedule prepared two to three years before a sale prevents buyer QoE reviews from eroding the final offer.

What Should You Do Next?

If you are planning a sale, partner buyout, or ESOP transaction within the next two to three years, build a defensible normalized EBITDA schedule now rather than at the negotiating table. Three years of consistently documented adjustments are far more credible to a buyer than a single peak-year figure assembled under deadline pressure.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides business valuation services supporting M&A transactions, partner buyouts, and ESOP feasibility analyses. Schedule a consultation to discuss the right approach for your business.

People Also Read

- Adjusted EBITDA vs EBITDA: Key Differences Explained

- EBITDA Multiple for Business Valuation by Industry

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}