Last Updated: April 2026

A pre-revenue startup valuation is an independent assessment of fair market value (FMV) for a company that has not yet generated income. Without revenue or earnings, traditional valuation methods do not apply directly. Appraisers and investors use structured frameworks that translate team quality, market size, prototype progress, and early customer traction into a defensible dollar estimate. Internal Revenue Code (IRC) Section 409A (2024) requires stock options be issued at no less than FMV, making an independent valuation both a compliance requirement and a strategic tool.

At Sofer Advisors, we prepare 409A valuations and startup appraisals for early-stage companies navigating equity compensation, fundraising, and acquisition planning. Pre-revenue valuation is not guesswork. Each method below provides a systematic way to price a business before it earns a dollar, and the method selected directly affects the share price your employees pay for their options.

Whether you are issuing your first option grant, preparing for a seed round, or defending a 409A in due diligence, the valuation method your appraiser selects and the milestones your company has reached determine whether that conclusion holds up under IRS review or investor scrutiny.

Key Takeaways

- Pre-Revenue Methods – appraisers use the Berkus, scorecard, risk factor summation, cost-to-duplicate, and VC methods rather than revenue or earnings multiples to value startups with no income.

- Berkus Method Ceiling – this framework assigns up to $500,000 to each of five milestones, placing the maximum pre-money valuation at $2.5 million for the earliest-stage companies.

- VC Method Return Targets – investors applying the VC method require 10x to 30x returns, working backward from a projected exit valuation to estimate today’s implied pre-money value.

- 409A Compliance Requirement – IRC Section 409A (2024) mandates an independent valuation before stock options are issued; without one, recipients face income tax plus a 20 percent excise tax on the grant date.

- Cost and Timeline – a 409A valuation for a pre-revenue startup costs $2,500 to $9,000 and takes two to four weeks from data submission to final report.

The sections below examine each of these in detail: the core methods appraisers use, how the Berkus method works, what multiples investors apply, how equity dilution affects startup value, and when a 409A valuation is legally required.

How Do You Value a Startup With No Revenue?

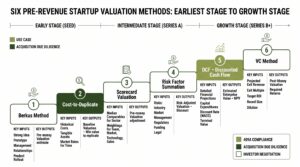

Appraisers value pre-revenue startups by assessing founding team strength, market opportunity, prototype progress, and early customer signals. These methods are specifically designed to price future potential rather than historical earnings. Without a financial track record, they serve as the bridge between founder conviction and investor confidence. The most widely used frameworks are the Berkus method, scorecard method, risk factor summation, cost-to-duplicate method, and venture capital (VC) method.

Without revenue or earnings before interest, taxes, depreciation, and amortization (EBITDA), appraisers cannot directly apply market multiples or discounted cash flow (DCF) analysis the same way they would for an established business. Pre-revenue valuation substitutes historical financials with forward-looking assumptions and qualitative assessments. The selection of method depends on the company’s stage, the purpose of the valuation, and what data is available to support the assumptions made at the time of engagement.

According to the AICPA (2023), best practices for early-stage company valuation require appraisers to document the rationale for method selection and calibrate conclusions against comparable transactions in the same industry. Without that calibration, a valuation cannot withstand IRS review or investor scrutiny.

Independent appraisal firms such as Stout and Kroll apply these frameworks to produce 409A valuations that satisfy IRS safe harbor requirements. Sofer Advisors, with dual ABV and ASA accreditation recognized by the IRS, SEC, and FINRA, delivers the same institutional rigor with a founder-education approach that larger firms rarely provide.

What Is the Berkus Method of Valuation?

The Berkus method assigns up to $500,000 in value to each of five startup milestones, creating a pre-money valuation ceiling near $2.5 million for companies with no significant revenue. A startup that has completed three milestones receives a pre-money valuation near $1.5 million. That ceiling directly reflects the risk profile of a company with no proven revenue model, where potential is real but execution risk remains high across every dimension.

Developed by angel investor Dave Berkus, this method was designed for early-stage technology startups. Each milestone represents a category of risk the startup has reduced by reaching a defined threshold. A sound idea addresses the risk of building something no one wants. A working prototype demonstrates that the team can execute. A quality management team reduces leadership failure risk. Strategic relationships expand market access. Product rollout signals that the revenue model can function at some scale.

| Milestone | Max Value Added |

|---|---|

| Sound idea (basic value) | $500,000 |

| Prototype (reduces technology risk) | $500,000 |

| Quality management team (reduces execution risk) | $500,000 |

| Strategic relationships (reduces market risk) | $500,000 |

| Product rollout or initial sales (reduces production risk) | $500,000 |

The Berkus method is simple and transparent, making it well suited for angel and pre-seed rounds. Investors frequently combine it with the scorecard or VC method for larger raises, because no single method captures the complete risk picture at the earliest stages of company development.

What Startup Valuation Methods Do Investors Use?

Investors and appraisers apply six core methods to pre-revenue startups, often combining two or three to triangulate a defensible fair market value. No single method works in every situation. The right choice depends on the company’s stage, the purpose of the valuation (409A compliance, investor negotiation, or acquisition due diligence), and what financial data and comparable transactions are available to support the analytical framework being applied.

The six most common methods are:

- Berkus method – milestone-based scoring for early-stage technology startups, pre-money ceiling near $2.5 million

- Scorecard method – benchmarks against comparable funded companies using weighted factors for team strength, market size, product quality, and traction

- Risk factor summation – starts from an average pre-money value for comparable companies, then adjusts for 12 defined risk categories including management depth, legislative risk, and competitive environment

- Cost-to-duplicate – estimates what it would cost to rebuild the startup from scratch, establishing a value floor based on investment made to date

- Income approach using DCF – applies a discount rate to projected future revenues; used when projections can be credibly supported by market data or early customer commitments

- Venture capital (VC) method – works backward from a projected exit valuation using the investor’s required return multiple of 10x to 30x

Appraisers frequently weight methods by reliability. When financial projections are speculative, the Berkus and scorecard methods carry more weight. When a lead investor has set terms in a comparable raise, the VC method and DCF provide the strongest evidence. Method triangulation is standard practice at valuation firms with established 409A experience and is the most defensible approach before the IRS.

What Multiples Apply to Pre-Revenue Startups?

Pre-revenue startups are not valued on revenue multiples because there is no revenue to multiply. Investors applying the VC method require 10x to 30x returns to compensate for the high failure rate of early-stage companies, working backward from a projected exit valuation to estimate the company’s present worth. The implied pre-money value is derived from the exit assumption and the return target, not set as a starting point.

Without revenue or earnings, multiples-based approaches require a bridge to projected financials. An investor estimates the startup’s exit value, divides by the required return multiple, and discounts to today. A $100 million assumed exit at a 20x return implies a present value of $5 million before deducting the required investment amount. That calculation assumes the investor can negotiate a price at or below that implied value when the round closes, which is why method assumptions are openly debated during term sheet negotiations.

National Venture Capital Association (NVCA) (2024) data shows that early-stage valuations averaged $8 million to $12 million pre-money for seed rounds with a lead institutional investor. Pre-revenue companies without institutional backing frequently see implied valuations in the $1 million to $4 million range, depending on market size, team credibility, and comparable transaction data.

Once the company reaches annual recurring revenue (ARR), revenue multiples replace the VC method as the primary benchmark. High-growth software-as-a-service (SaaS) companies at Series A typically command 4x to 10x ARR depending on growth rate and competitive position.

How Does Equity Dilution Affect Startup Value?

Each new funding round creates new shares, reducing existing shareholders’ percentage ownership and changing the per-share price used in 409A valuations. Founders and early employees who hold options granted before a round absorb dilution through a lower ownership percentage at exit, not through a change in their original option price. Understanding this distinction before issuing equity compensation prevents both strategic and compliance errors.

A Simple Agreement for Future Equity (SAFE) is a widely used pre-revenue financing instrument. SAFEs grant investors the right to receive equity at a future priced round, typically at a discount of 15 to 25 percent or subject to a valuation cap. When a priced round closes, the post-money valuation changes, the share count increases, and the per-share price for future option grants must reflect the new fair market value.

Founders who do not update their 409A after a material funding event risk issuing options below FMV. Under IRC Section 409A (2024), the option recipient owes income tax on the discount at vesting, plus a 20 percent excise tax, creating significant personal liability with no cash distribution to fund the payment.

When Does a Startup Need a 409A Valuation?

A 409A valuation is required before a startup issues any stock options and must be refreshed after specific triggering events. Missing a trigger and issuing options without a current 409A exposes option recipients to ordinary income tax plus a 20 percent excise tax on the grant date, not at exercise. The safe harbor protection provided by an independent appraisal applies only if the valuation was completed before the grant.

The IRS requires that stock options be granted at no less than FMV to avoid adverse tax consequences under IRC Section 409A (2024). An independent appraisal meeting the regulatory standard creates a legal safe harbor protecting both the company and the option recipient from enforcement. Without that safe harbor, the IRS can assess the full tax liability on the grant date rather than waiting for the option to be exercised or the underlying shares to be sold.

The six most common 409A triggers are:

- First option grant – required before the startup issues any employee stock options

- New priced round – required after closing a seed, Series A, Series B, or later equity round

- Material event – required after a significant new contract, regulatory approval, or acquisition offer

- Annual refresh – required if no major funding event has occurred but option grants continue

- Pre-transaction – required before any merger, acquisition, or asset sale

- SAFE conversion – required after SAFEs or convertible notes convert to priced equity

Each trigger represents a point at which fair market value has materially changed and prior option pricing is no longer defensible. The cost of a 409A valuation ($2,500 to $9,000) is a small fraction of the tax exposure it prevents for every employee who holds options.

Selecting the right valuation method requires documented assumptions, calibrated inputs, and a clear audit trail. Founders who understand these requirements before issuing options or entering a raise are better positioned to protect their teams from compliance risk. An appraiser with dedicated 409A experience makes that process faster and more defensible in any IRS review.

Frequently Asked Questions

What is pre-revenue startup valuation?

Pre-revenue startup valuation establishes a fair market value for a company with no income. Appraisers use the Berkus method, scorecard method, risk factor summation, and VC method instead of revenue multiples. The result informs investor negotiations, stock option pricing under IRC Section 409A, and acquisition due diligence. Inputs include team quality, market size, prototype progress, and early customer traction signals.

How does the Berkus method work?

The Berkus method assigns up to $500,000 to each of five startup milestones: a sound idea, a working prototype, a quality management team, strategic relationships, and product rollout or initial sales. The maximum pre-money valuation is $2.5 million. A startup that has completed three milestones receives a valuation near $1.5 million. The method is most useful for angel rounds and pre-seed companies without institutional backing.

What is the scorecard valuation method?

The scorecard method benchmarks a target startup against recently funded comparable companies in the same sector. The appraiser assigns weighted scores across five to seven factors: team strength, market size, product quality, competitive environment, and sales channels. Each factor carries a percentage weight, and the target company’s score is multiplied by the average pre-money valuation of comparable funded companies to arrive at an estimated value.

What is the VC method for startup valuation?

The venture capital (VC) method estimates a startup’s current value by working backward from a projected exit valuation. The appraiser assumes an exit value, divides by the investor’s required return multiple (typically 10x to 30x), and discounts the result to the present day. The method requires assumptions about exit timing, exit value, and the investor’s required rate of return.

How much does a 409A valuation cost for a pre-revenue startup?

A 409A valuation for a pre-revenue startup typically costs between $2,500 and $9,000, depending on the firm and the complexity of the company’s capital structure. Boutique valuation firms generally charge less than Big 4 accounting firms or national firms such as Stout or Kroll. The process takes two to four weeks from submission of financial materials to delivery of the final report.

How long does a 409A valuation take to complete?

A 409A valuation typically takes two to four weeks from the date the appraiser receives all required materials. Pre-revenue companies generally have simpler capital structures, which can reduce turnaround time. The process includes data review, valuation modeling, report drafting, and a review period for founder questions. Founders should factor this timeline into any option grant or fundraising schedule.

What is a SAFE and how does it affect my 409A valuation?

A Simple Agreement for Future Equity (SAFE) is a pre-revenue financing instrument that grants investors the right to receive equity at a future priced round, typically at a discount or subject to a valuation cap. SAFEs do not require a 409A at issuance because no share price is set. Once a SAFE converts to equity at a priced round, a new 409A valuation must be completed before issuing additional stock options.

How often must a startup refresh its 409A valuation?

A startup must update its 409A valuation every 12 months if no material event has occurred, or immediately after a triggering event such as a new priced round, a significant contract, or conversion of SAFEs or convertible notes. Options granted after a triggering event but before a new 409A is completed may be non-compliant under IRC Section 409A, resulting in income tax and a 20 percent excise tax penalty for option recipients.

What happens if a startup issues stock options without a 409A valuation?

Issuing stock options without a current 409A creates immediate tax consequences for the option recipient. Under IRC Section 409A (2024), the recipient owes income tax on the intrinsic value at vesting, plus a 20 percent excise tax and interest. The company may also face reporting obligations. An independent 409A appraisal completed before the grant provides safe harbor protection for both the company and its option holders.

Can a startup perform its own 409A valuation?

Startups cannot self-value for IRS safe harbor purposes. To qualify for safe harbor under IRC Section 409A, the valuation must be performed by an independent appraiser with relevant credentials and valuation experience. Founders and internal employees are not considered independent. A 409A completed without an independent appraiser does not qualify for safe harbor and exposes the company to IRS scrutiny and potential penalties.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

Pre-revenue startup valuation is both a regulatory requirement and a strategic tool. IRC Section 409A (2024) mandates that stock options be issued at fair market value, established by an independent appraisal. Early-stage companies use the Berkus, scorecard, risk factor summation, cost-to-duplicate, and VC methods because revenue multiples do not apply without a financial track record. Each funding round and material event requires a refreshed 409A. Knowing how these methods work and when a valuation is legally required gives founders the clarity to price equity accurately and protect option holders from IRS penalties.

What Should You Do Next?

If your startup is preparing for its first option grant, closing a seed round, or converting SAFEs to equity, a current 409A valuation is required before issuing options. Founders who wait expose option recipients to income tax and a 20 percent excise tax on the grant date. That is the Sofer Difference: institutional-grade protection with a cost and timeline designed for early-stage companies.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides independent 409A valuations and startup valuation consulting for early-stage companies at every funding stage. Schedule a consultation to discuss your valuation timeline and equity structure.

People Also Read

- 409A Valuation for Startups: What Founders Must Know

- 409A Valuation Cost and Pricing Guide for Startups

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}