Last Updated: April 2026

Veterinary practice valuation is the process of determining the fair market value (FMV) of a privately held veterinary business, whether a solo companion animal clinic, a multi-doctor general practice, an emergency and critical care hospital, or a specialty referral center, using accepted financial and market-based methodologies that account for the practice’s earnings, client base, staff structure, and the risk profile specific to the veterinary sector. The applicable method and multiple depend on the practice’s size, specialty, doctor dependency, and whether the buyer is a corporate consolidator, a private equity-backed platform, or an individual practitioner.

Sofer Advisors, a credentialed business valuation firm based in Atlanta, GA, provides independent business appraisals for veterinary practice owners, buyers, attorneys, and financial advisors, including pre-sale valuations, buy-sell agreement appraisals, and estate and gift tax appraisals for practice ownership transfers, with ABV and ASA credentialed oversight on every engagement.

If you are a practice owner preparing for a sale, planning a partner buyout, or transferring a practice interest for estate planning, the difference between an informal estimate and a credentialed independent appraisal can represent hundreds of thousands of dollars in after-tax proceeds. Veterinary practice values have increased substantially over the past decade as corporate consolidators and private equity-backed platforms have entered the sector, raising EBITDA multiples and creating a more complex valuation environment.

Key Takeaways

- EBITDA Multiples Drive Value for Established Practices: Mid-size practices with EBITDA above $500,000 are valued at 6x to 10x EBITDA. Solo practices under $500,000 use SDE multiples in the 2x to 4x range.

- Doctor Dependency Is the Largest Single Value Discount: Practices where the owner generates more than 60% of revenue face a material discount. Distributed production across three or more veterinarians commands higher multiples.

- Corporate Consolidators Pay Higher Multiples: Private equity-backed platforms pay above-market multiples for practices with minimum EBITDA thresholds, multi-doctor structure, and geographic fit with their existing networks.

- Revenue Multiples Are a Secondary Check Only: Rule-of-thumb revenue multiples of 0.7x to 1.5x gross revenue do not capture profitability differences. EBITDA multiples are the credentialed standard for formal appraisals.

- A Credentialed Appraisal Is Required for Tax, Legal, and Financing: IRS estate returns, ESOP transactions, and SBA loans above $250,000 all require a qualified independent appraisal. A broker opinion does not satisfy any of these requirements.

The sections below examine each of these principles in detail: the valuation methods applied to veterinary practices, the EBITDA multiples by practice type, the key value drivers and discounts, how corporate consolidation affects pricing, how solo and multi-doctor practices compare in value, and when a formal independent appraisal is legally required.

How Is a Veterinary Practice Value Determined?

When you need to determine what your veterinary practice is worth, credentialed appraisers apply three standard approaches: the market approach using comparable transaction EBITDA or SDE multiples, the income approach using discounted cash flow analysis, and the asset approach as a secondary check on going-concern value.

Veterinary practice valuation adapts these methods to the specific financial and operational characteristics of the sector. The market approach applies transaction multiples from comparable veterinary practice sales to the subject practice’s normalized EBITDA or SDE. The income approach applies a capitalization of earnings or DCF analysis to projected cash flows. The asset approach values tangible and intangible assets at FMV and is rarely used as a standalone method for going-concern practices.

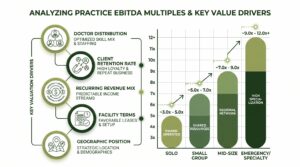

| Practice Type | Revenue Range | Primary Method | Typical Multiple | Key Adjustment |

|---|---|---|---|---|

| Solo (Owner-Operator) | Under $750K | SDE Multiple | 2.0x – 3.5x SDE | Doctor transition discount |

| Small Group (2-3 Doctors) | $750K – $2M | EBITDA Multiple | 5x – 7x EBITDA | Client retention; staff stability |

| Mid-Size (4-6 Doctors) | $2M – $8M | EBITDA Multiple | 7x – 9x EBITDA | Management depth; growth trajectory |

| Emergency/Specialty | $5M+ | EBITDA Multiple | 8x – 12x+ EBITDA | Referral network; specialized equipment |

For practices valued using the market approach, the appraiser identifies transactions involving comparable veterinary practices in terms of size, specialty, geography, and financial profile, then applies the selected multiple to normalized earnings. Normalization adjusts reported earnings for the owner’s above-market compensation, personal expenses run through the practice, non-recurring items, and related-party transactions that would not continue under new ownership.

According to the American Veterinary Medical Association (AVMA) (2024), there are approximately 31,000 veterinary practices in the United States. Corporate consolidators entering the sector over the past decade have driven median EBITDA multiples for well-performing companion animal practices from approximately 3x to 5x before 2015 to 6x to 10x or higher in recent transactions, making independent appraisal increasingly critical as price expectations and buyer willingness to pay have moved in both directions.

What EBITDA Multiples Apply to Vet Practices?

EBITDA multiples for veterinary practices range from 4x to 12x or higher depending on practice size, type, and buyer. Your specific multiple reflects five adjustable risk factors: doctor concentration, client retention rate, geographic competition, facility stability, and five-year revenue growth trend. Applying a median published multiple without these adjustments can overstate or understate value by 30% to 50%.

The EBITDA multiple is the most widely used valuation benchmark for practices with established management, multiple doctors, and EBITDA above $500,000. EBITDA is calculated by adding back interest, taxes, depreciation, and amortization to net income, normalizing for owner compensation at a market management rate of $150,000 to $250,000 per full-time equivalent veterinarian, and removing non-recurring items. The resulting normalized EBITDA is multiplied by a market-derived multiple.

General companion animal practices with EBITDA between $500,000 and $1.5 million and two to three doctors trade at 5x to 7x EBITDA when sold to individual buyers or smaller platforms. The same practice sold to a well-capitalized corporate consolidator targeting that geographic market may trade at 8x to 10x or higher, because the consolidator can achieve margin improvements through group purchasing, shared services, and operational scale that an individual buyer cannot. Specialty and emergency practices with EBITDA above $2 million and referral network depth trade at 10x to 12x or more, reflecting their defensible competitive position and high barriers to entry.

According to the American Society of Appraisers (ASA) (2024), a credentialed appraiser specializing in professional practice valuation applies risk-factor adjustments systematically rather than selecting a multiple from a published range without support. This discipline is what separates a defensible FMV conclusion from an informal estimate.

What Drives Value in a Veterinary Practice?

The reality is that two practices with identical revenue can produce valuations that differ by 3x to 4x. The multiple reflects risk, not revenue. Factors that place your practice above the median are those that protect earnings continuity after the sale; factors that reduce it are those that threaten the buyer’s ability to retain revenue.

Value drivers that increase veterinary practice value above the median multiple include:

- Multi-doctor production distribution: Practices with no single doctor generating more than 30% of total production command higher multiples because buyer earnings risk after the owner’s departure is lower.

- Active client count and retention rate: A practice with 3,000 or more active clients and annual retention above 70% has a more defensible revenue base than a comparable practice with higher attrition.

- Recurring revenue mix: Practices with wellness plan enrollment or subscription preventive care programs have more predictable cash flows than transaction-dependent general practices.

- Facility ownership or long-term lease: Practices that own their facility or hold a long-term transferable lease with renewal options eliminate facility relocation risk for the buyer and support a higher multiple.

- Geographic market position: Practices in high-growth suburban markets with limited veterinary competition within a 5-mile radius have stronger pricing power and growth potential than those in saturated markets.

No list of value drivers substitutes for a practice-specific analysis. The weight assigned to each factor varies by buyer type, market conditions, and the practice’s unique risk profile, which is why a credentialed appraisal is required for any formal valuation purpose.

Key value discounts include owner-concentrated production, a facility lease expiring within 24 months without a renewal option, declining active client counts over the prior three years, significant deferred capital expenditure, and key staff turnover risk tied to the departing owner’s personal relationships.

How Does Corporate Consolidation Affect Valuation?

Corporate consolidation has raised EBITDA multiples for qualifying practices over the past decade, but the benefit is not automatic. If your practice meets the size and structure criteria that national platforms target, including minimum $500,000 in normalized EBITDA, at least two full-time equivalent veterinarians, and geographic fit, you may receive competitive offers from multiple corporate buyers that individual buyers cannot match.

According to the Internal Revenue Service (IRS) (2024), the fair market value of a closely held professional practice such as a veterinary clinic must be determined under the hypothetical willing buyer and willing seller standard of Revenue Ruling 59-60. Where corporate consolidators have established a documented pattern of paying above-historical-norm EBITDA multiples for qualifying practices, those transactions constitute relevant market evidence that a credentialed appraiser must consider.

National valuation advisory firms such as Stout and Kroll (formerly Duff & Phelps) typically provide financial due diligence and transaction support for large corporate buyers in these deals. The selling practice owner needs an independent credentialed appraisal from a firm that is not engaged by the buyer, to establish FMV independently before negotiating and to satisfy any regulatory requirements tied to the transaction.

Practices that do not meet corporate buyer criteria, including solo practices, practices with doctor-concentrated production, and practices in rural markets with limited strategic value to a consolidator, are valued by reference to individual buyer transaction comparables, which carry lower multiples. Owners who receive an unsolicited offer from a corporate buyer should obtain an independent appraisal before responding, because the offer price may be above or below FMV depending on the buyer’s internal strategic valuation.

Schedule your free consultation with Sofer Advisors, an Inc. 5000-recognized firm with 180+ five-star Google reviews, to receive a credentialed independent veterinary practice appraisal that reflects current market conditions, corporate consolidation multiples, and your practice’s specific risk factors. Discover The Sofer Difference.

How Do Solo and Multi-Doctor Practices Compare?

Here is what most solo practice owners don’t realize: the valuation gap between a solo practice and a multi-doctor practice of equal revenue isn’t primarily about size. It’s about transition risk, specifically the buyer’s exposure to the possibility that patients, staff, and referral relationships will follow the departing owner out the door.

A solo practice where the selling owner is the primary or sole producing veterinarian carries material transition risk. Patients may follow the departing doctor to a new clinic, staff may leave due to loyalty to the seller, and revenue may decline materially in the 12 to 24 months after close before stabilizing under new management. This risk is reflected in lower EBITDA multiples and more conservative earnings normalization in the appraisal.

A multi-doctor practice with distributed production and a stable associate doctor team presents a fundamentally different risk profile. Revenue continuity after the owner’s departure is more predictable because patients have established relationships with remaining associate doctors. Staff retention is more likely because team culture is not entirely dependent on the owner’s personal relationships. These structural differences, not absolute revenue size, explain why multi-doctor practices trade at EBITDA multiples 2x to 4x higher than solo practices of similar revenue.

The owner of a solo practice who wants to maximize sale value can hire an associate before the sale to build a multi-doctor structure, but this transition requires 24 to 36 months of associate development before the valuation benefit is reflected in a credentialed appraisal. Owners who begin this process early, as part of a planned exit strategy, consistently achieve higher after-tax proceeds than those who list their practice before the structural risk profile has improved.

When Do You Need a Formal Vet Practice Appraisal?

You need a credentialed independent business appraisal whenever the concluded value carries tax, regulatory, or financial consequences if misstated. Informal estimates from brokers, corporate buyer offers, and rule-of-thumb revenue multiples do not satisfy IRS, ERISA, or SBA standards. A formal engagement with an ABV or ASA credentialed appraiser is required for the following purposes.

Circumstances that require or strongly warrant a formal independent appraisal for a veterinary practice include:

- Pre-sale negotiation: An independent FMV conclusion prepared before engaging buyers establishes a credentialed price anchor that supports the asking price against buyer due diligence adjustments and quality of earnings analysis.

- Buy-sell agreement trigger: When a partnership buyout is triggered by a partner’s death, disability, or retirement, most well-drafted buy-sell agreements require a credentialed independent appraisal if the parties cannot agree on price.

- Estate tax return: The IRS requires a qualified appraisal satisfying Revenue Ruling 59-60 for any estate and gift tax return that includes a veterinary practice interest, with the appraisal signed by a credentialed appraiser under penalties of perjury.

- Gift of practice interest: Any transfer of a veterinary practice interest by gift requires a qualified appraisal under Treasury Regulation 25.2512-2(f) to support the FMV reported on Form 709.

- SBA lending: Small Business Administration (SBA) lenders require a credentialed business valuation for loans above $250,000 where the veterinary practice serves as collateral, prepared under SBA SOP 50-10.

- ESOP establishment: If the practice converts to employee ownership, the Employee Retirement Income Security Act (ERISA) requires an annual independent appraisal by a qualified appraiser to satisfy the ESOP trustee’s fiduciary obligation.

Regional CPA firms and practice brokers provide informal estimates and rule-of-thumb price opinions that do not satisfy any of these formal requirements. Sofer Advisors, with 15+ years of valuation experience and dual ABV and ASA credentials recognized by the IRS, SEC, and FINRA, provides the independent credentialed appraisals required for all formal purposes.

Frequently Asked Questions

How do you calculate the value of a veterinary practice?

Veterinary practice value is calculated by applying a market-derived EBITDA multiple to normalized EBITDA for established multi-doctor practices, or an SDE multiple for solo owner-operated practices. Normalization adjusts reported earnings for owner compensation, personal expenses, and non-recurring items. The selected multiple reflects the practice’s risk profile relative to comparable transactions, adjusted for doctor concentration, client retention, geographic market, and buyer type, with income and asset approaches applied as secondary checks.

What is a good EBITDA for a veterinary practice?

EBITDA margins for companion animal practices range from 15% to 30% of gross revenue, depending on compensation structure, facility costs, and staffing model. A practice with $2 million in revenue and a 20% EBITDA margin produces $400,000 in EBITDA, which at a 7x multiple yields a $2.8 million enterprise value. Specialty and emergency practices often achieve 25% to 35% margins. Practices below 12% EBITDA face multiple compression from buyers who normalize profitability downward.

What EBITDA multiple is used for a vet practice?

EBITDA multiples for veterinary practices range from approximately 4x to 12x or higher depending on practice size, type, and buyer. Solo practices under $500,000 in EBITDA trade at 4x to 6x. Small group practices with two to three doctors trade at 5x to 7x when sold to individual buyers. Mid-size practices trade at 7x to 9x. Specialty and emergency hospitals with $2 million or more in EBITDA trade at 10x to 12x or higher when sold to well-capitalized corporate buyers.

How profitable is a veterinary practice?

Veterinary practice profitability depends on practice type, staffing model, and owner compensation structure. Companion animal practices generate net owner benefit of 20% to 30% of gross revenue when measured as SDE. Multi-doctor practices with professional management generate EBITDA margins of 18% to 28%. Emergency and specialty practices achieve the highest EBITDA margins in the sector due to premium pricing and referral models. Revenue alone does not indicate profitability without understanding the full cost structure and owner compensation treatment.

What is the difference between SDE and EBITDA for a vet practice?

SDE, or seller’s discretionary earnings, adds the owner’s total compensation and personal benefits back to net income, capturing the full economic benefit available to an owner-operator. EBITDA measures operating earnings available to a buyer who installs a doctor at market compensation. SDE multiples are applied where the owner is the primary producing doctor. EBITDA multiples apply where professional management exists independent of the owner and the practice can operate without the selling veterinarian.

Does corporate consolidation increase what my practice is worth?

Corporate consolidation increases valuations for practices that meet consolidator acquisition criteria, including minimum EBITDA thresholds, multi-doctor structure, and geographic fit with the buyer’s existing network. Practices that qualify receive competitive offers from multiple corporate buyers, driving multiples above what individual buyers pay. Practices that do not qualify are valued by individual buyer comparables, which carry lower multiples. A credentialed independent appraisal establishes FMV incorporating both individual and corporate buyer markets as relevant evidence.

How do I value a veterinary practice for estate planning?

For estate planning, a veterinary practice must be appraised at FMV under the hypothetical willing buyer and willing seller standard of Revenue Ruling 59-60. The appraisal must apply income, market, and asset approaches and address all eight FMV factors including economic outlook, earning capacity, and comparable transactions. A discount for lack of control or marketability may apply if a minority interest is being transferred. The appraisal must be completed before the estate or gift tax return is filed.

How much does a veterinary practice appraisal cost?

An independent business appraisal for a veterinary practice from Sofer Advisors ranges from $7,500 to $25,000 depending on the practice’s revenue, complexity, and scope of methodologies required. Most standard engagements are completed within four to eight weeks of document receipt. Pre-sale appraisals are frequently recovered in the improved negotiating position they create, and estate and gift tax appraisals are deductible as ordinary and necessary expenses. For a fee estimate, contact Sofer Advisors.

What documents are needed for a veterinary practice valuation?

A credentialed appraiser requires three to five years of financial statements and tax returns, an active client count and retention report, a doctor production report showing revenue by veterinarian, facility lease documentation, a current equipment list, a staff roster with tenure and compensation, and any existing buy-sell or shareholder agreements. Specialty practices also provide referral source data. Documentation completeness directly affects the appraiser’s ability to normalize earnings accurately and reduces IRS challenge risk.

How long does a veterinary practice valuation take?

A standard independent appraisal takes four to eight weeks from the date all required financial documents are received, covering appraisal fieldwork, financial analysis, market comparables research, and report preparation. Pre-sale appraisals should be initiated at least three to six months before the intended transaction start date to allow time to review the concluded value and address any value-limiting findings. Estate and gift tax appraisals must be completed before the relevant tax return filing deadline.

Can a broker price opinion replace an independent appraisal?

No. A broker price opinion from a veterinary practice broker estimates the likely selling price range based on market experience, but it is not a qualified appraisal under IRS, ERISA, or ASA standards. It does not satisfy the ERISA independent appraisal requirement for ESOP transactions and does not support a Form 8283 or Form 709 charitable or gift tax filing. A credentialed independent appraisal prepared by an ABV or ASA-credentialed appraiser is required for all formal purposes.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

Veterinary practice valuation applies the market, income, and asset approaches to determine FMV, with EBITDA multiples as the primary benchmark for established multi-doctor practices and SDE multiples for solo owner-operated practices. Multiples range from 4x to 12x or higher depending on practice size, specialty, doctor concentration, client retention, geographic market, and buyer type. Corporate consolidation has materially increased multiples for qualifying practices over the past decade, while solo practices with high doctor dependency trade at discounts to the market median. A credentialed independent appraisal is required for estate and gift tax returns, ESOP transactions, SBA lending, and buy-sell agreement triggers.

What Should You Do Next?

If you are considering selling your veterinary practice, planning a partner buyout, or need a credentialed appraisal for estate planning, an SBA loan, or an ESOP transaction, the starting point is a consultation with a qualified appraiser who can assess your practice’s current value and the specific factors driving it above or below the median multiple for your practice type. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals for veterinary practices across all size categories and all valuation purposes. Schedule your free consultation to understand what your veterinary practice is worth.

People Also Read

- How to Value a CPA or Accounting Firm: Beyond the 1x Revenue Rule

- How to Value an Insurance Agency: Multiples and Methods

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This article provides general information for educational purposes only and does not constitute legal, tax, financial, or professional advice. Consult qualified professionals regarding your specific circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}