Last Updated: April 2026

Adjusted EBITDA is a modified version of earnings before interest, taxes, depreciation, and amortization (EBITDA) that removes non-recurring, owner-specific, and non-cash items from reported earnings to reveal the true repeatable cash flow generating capacity of a business. While EBITDA is calculated directly from the income statement, adjusted EBITDA reflects a series of normalization adjustments, commonly called addbacks, that present the business as it would operate under a hypothetical arm’s-length buyer rather than its current owner. Buyers, lenders, and business appraisers rely on adjusted EBITDA rather than reported EBITDA to set enterprise value because the raw figure often includes expenses unique to the current ownership structure that a new owner would not incur.

For business owners preparing for a sale or recapitalization, the difference between reported and adjusted EBITDA can directly change the enterprise value offered by millions of dollars, since most middle-market businesses trade at multiples of four to seven times EBITDA. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, prepares independent business appraisals that calculate defensible adjusted EBITDA, support seller-side addback claims under buyer due diligence, and document normalized earnings for IRS audit purposes in middle-market transactions nationwide.

Understanding which adjustments are legitimate, how buyers assess them, and how the adjusted figure drives the final enterprise value is essential knowledge for any business owner entering a sale process. The Key Takeaways below define the essential distinctions before the detailed analysis that follows.

Key Takeaways

- EBITDA Is the Starting Point, Not the Endpoint: Raw EBITDA from the income statement includes owner compensation at its current level, one-time expenses, and non-cash charges that will not recur under new ownership; adjusted EBITDA removes those distortions to show normalized operating earnings.

- Every Dollar of Addback Multiplies Into Enterprise Value: At a 6.0x EBITDA multiple, one additional dollar of legitimately supported addback increases the enterprise value by six dollars; a $200,000 owner compensation adjustment at that multiple adds $1.2 million to the indicated value.

- Buyers Scrutinize Addbacks During Quality of Earnings Review: Buyers commission a quality of earnings (QoE) report from an independent accountant to verify that each seller addback is real, non-recurring, and properly documented; unsupported addbacks are reversed, directly reducing the purchase price.

- Appraisers Apply Normalization Adjustments Under Professional Standards: In a formal business appraisal, the appraiser applies normalization adjustments to EBITDA following AICPA and ASA standards, producing a documented, defensible adjusted EBITDA that satisfies IRS audit scrutiny and lender underwriting requirements.

- Not All Adjustments Run in the Same Direction: Sellers add back expenses to increase EBITDA; buyers sometimes make downward adjustments to remove one-time revenue or non-recurring income that inflated the seller’s trailing results, reducing adjusted EBITDA below the reported figure.

Each of these points determines how a buyer and seller will ultimately negotiate enterprise value. The sections below examine what EBITDA and adjusted EBITDA are, which addbacks are commonly accepted, how buyers challenge them, and how valuation professionals apply normalization in a formal appraisal.

What Is EBITDA?

EBITDA, earnings before interest, taxes, depreciation, and amortization, is a proxy for a business’s operating cash flow before financing decisions, tax structure, and non-cash accounting charges are applied. It is calculated by starting with net income and adding back interest expense, income taxes, depreciation, and amortization. Because interest and taxes are functions of the owner’s financing choices and tax structure rather than the business’s operating performance, removing them produces a figure that is more comparable across businesses with different capital structures and tax positions.

| Metric | What It Measures | Includes Owner-Specific Items | Adjusted for Recurring vs Non-Recurring | Used By |

|---|---|---|---|---|

| Net Income | After-tax bottom line | Yes | No | Sellers reporting historical results |

| EBITDA | Operating cash flow proxy | Yes | No | First screening by buyers and lenders |

| Adjusted EBITDA | Normalized repeatable earnings | No | Yes | Appraisers, PE firms, lenders, deal negotiations |

| Seller’s Discretionary Earnings (SDE) | Owner benefit including one salary | No | Yes | Small business transactions under $3M revenue |

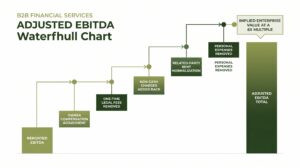

EBITDA is the standard starting metric in middle-market M&A because it strips out financing and tax effects, but it does not yet strip out the owner’s personal expenses, one-time charges, or non-cash items embedded in the income statement. That second layer of normalization is what produces adjusted EBITDA.

What Is Adjusted EBITDA?

Adjusted EBITDA begins with reported EBITDA and applies a series of addbacks and downward adjustments to produce a normalized earnings figure that reflects what the business would generate under a reasonable, arm’s-length owner paying market-rate compensation and running the business without the idiosyncratic expenses of the current ownership structure. The adjustments are disclosed by the seller in an addback schedule and independently verified by the buyer’s accountant in a quality of earnings review.

Addbacks increase adjusted EBITDA above reported EBITDA when the adjustment removes an expense that is either above-market, non-recurring, or specific to the current owner. Downward adjustments reduce adjusted EBITDA below reported EBITDA when they remove one-time revenue events or below-market expenses that artificially inflated the seller’s trailing results. Most transactions involve a mix of both, and the negotiated adjusted EBITDA figure is the number on which the enterprise value multiple is applied at closing.

According to AICPA Forensic and Valuation Services (2023), normalization adjustments in business appraisals for middle-market transactions most frequently involve owner compensation, related-party transactions, non-recurring legal or professional fees, and personal expenses run through the business, all of which require documentation to withstand buyer and IRS scrutiny.

What Are Common EBITDA Addbacks?

Addbacks in middle-market business valuations fall into five categories. Each must be documented with supporting evidence, such as payroll records, contracts, invoices, or professional fee agreements, before a buyer or appraiser will accept the adjustment:

- Owner compensation adjustment: If the owner pays themselves above or below market-rate compensation, the adjustment replaces actual owner salary and benefits with the market cost of a professional manager performing the same role. In an owner-operated business where the owner takes a below-market salary and extracts profit through distributions, this is a downward adjustment that increases adjusted EBITDA.

- One-time and non-recurring expenses: Legal fees for a lawsuit that has been resolved, costs related to a facility move or system implementation, severance payments for terminated employees, and penalties for regulatory violations that have been corrected are removed because they will not recur under the new owner.

- Non-cash charges: Depreciation and amortization are already removed in the EBITDA calculation, but additional non-cash items such as stock-based compensation expense, amortization of deferred financing costs, and impairment charges are also added back because they do not represent actual cash outflows from the operating business.

- Related-party and above-market expenses: Rent paid to a related entity at above-market rates, professional fees paid to family members for services available at lower cost on the open market, and insurance premiums through owner-affiliated agencies at non-competitive rates are adjusted to market equivalents.

- Personal expenses run through the business: Automobile expenses for vehicles used primarily for personal purposes, personal travel and meals charged to the company, cell phone plans for family members, and personal club memberships deducted as business expenses are added back because the new owner will not incur them.

How Does Adjusted EBITDA Affect a Sale Price?

Adjusted EBITDA is the direct input into the EBITDA multiple that buyers and sellers apply to establish enterprise value in most middle-market transactions. If a business trades at a 5.0x EBITDA multiple and the seller’s addback schedule moves adjusted EBITDA from $800,000 to $1,000,000, the enterprise value increases from $4 million to $5 million. That $200,000 in addbacks produced a $1 million increase in indicated value. This multiplicative relationship is why sellers invest significant time and documentation in supporting the addback schedule before going to market, and why buyers scrutinize each adjustment with equal intensity.

The addback schedule also determines the letter of intent price versus the final purchase price in the definitive agreement. Buyers typically issue a letter of intent based on the seller’s stated adjusted EBITDA and then conduct quality of earnings diligence to verify each addback. If the QoE report reverses $100,000 in unsupported addbacks, the purchase price at a 5.0x multiple decreases by $500,000. A well-documented addback schedule prepared before the sale process begins protects the seller from price adjustments at the definitive agreement stage.

According to the American Society of Appraisers (ASA) (2024), the most common source of purchase price reduction between letter of intent and closing in middle-market transactions is buyer-driven reversal of seller addbacks that were not supported by adequate documentation at the time the LOI was issued.

Schedule your free consultation with Sofer Advisors to document your adjusted EBITDA with the credentialed appraisal support that holds up under buyer due diligence and prevents purchase price erosion between LOI and closing. Discover The Sofer Difference.

How Do Buyers Scrutinize EBITDA Adjustments?

Buyers challenge EBITDA addbacks through the quality of earnings (QoE) review, an independent accounting analysis commissioned by the buyer after the letter of intent is signed and during the due diligence period. The QoE examines the seller’s financial statements, addback schedule, and supporting documentation to determine whether each adjustment is legitimate, properly quantified, and genuinely non-recurring. QoE findings directly inform the final purchase price in the definitive agreement.

The adjustments buyers most frequently reverse or reduce in QoE review include:

- Unsupported owner compensation addbacks: If the seller claims a compensation adjustment but cannot provide a market comparability study or comparable compensation data for the role, buyers reduce or eliminate the addback.

- Recurring non-recurring expenses: Expenses labeled as one-time that appear across multiple years in the seller’s financials are treated as recurring costs, not addbacks. A legal expense claimed as one-time that appears in three consecutive years is classified as a regular business cost.

- Revenue pull-forward: Buyers investigate whether revenue was accelerated into the trailing twelve months through early invoicing, channel stuffing, or contract restructuring to inflate the measurement period results artificially.

- Related-party adjustments without market evidence: If the seller adjusts related-party rent to market rate but cannot produce a current market rent comparables analysis for the specific location, buyers apply their own (typically lower) market rent estimate.

- Pro-forma adjustments for businesses not yet acquired: Sellers sometimes add back the projected EBITDA of a planned acquisition or new product line that has not yet been completed; buyers give zero credit for pro-forma add-ons without a track record.

According to FASB Accounting Standards Codification 805 (2024), the acquirer’s purchase price allocation after closing must reflect the acquired business’s fair value of identifiable assets and liabilities at the acquisition date, independent of the seller’s addback schedule, reinforcing why independently established adjusted EBITDA is critical documentation for the post-close allocation.

How Does Valuation Use Adjusted EBITDA?

In a formal business appraisal, the appraiser calculates adjusted EBITDA as part of the income approach to value. The normalization process follows AICPA Statement on Standards for Valuation Services (SSVS No. 1) and ASA Business Valuation Standards, which require the appraiser to document every normalization adjustment and support each one with market data, comparable compensation surveys, or independent evidence. This professional documentation standard is what distinguishes an appraisal-grade adjusted EBITDA from a seller-prepared addback schedule and is what satisfies IRS audit requirements under Treasury Regulation 1.170A-17.

The appraiser applies the adjusted EBITDA in three ways. Under the market approach, adjusted EBITDA is multiplied by an appropriate EBITDA multiple derived from comparable public companies or precedent transactions to produce an indicated enterprise value. Under the income approach, adjusted EBITDA is the starting point for a normalized free cash flow projection used in a discounted cash flow (DCF) analysis. Under the asset approach, adjusted EBITDA confirms that the going concern value exceeds the liquidation value of the underlying assets. An EBITDA multiple analysis by industry shows the range of multiples buyers apply in specific sectors, all of which are applied against adjusted EBITDA rather than reported EBITDA.

Credentialed firms including Kroll and Stout provide EBITDA normalization analysis in large-cap transactions; for middle-market business owners, Sofer Advisors provides quality of earnings support and business appraisals with ABV and ASA credentialed oversight on every engagement, ensuring that the adjusted EBITDA figure presented to buyers is documented, defensible, and prepared to withstand QoE scrutiny without purchase price erosion.

Frequently Asked Questions

What is adjusted EBITDA?

Adjusted EBITDA is a normalized version of earnings before interest, taxes, depreciation, and amortization that removes non-recurring, owner-specific, and non-cash items to show the true repeatable operating earnings of a business. It begins with reported EBITDA from the income statement and applies a series of addbacks and downward adjustments. The adjusted figure is used by buyers, lenders, and appraisers to establish enterprise value because it strips out the distortions created by the current owner’s compensation structure, personal expenses, and one-time events.

How is adjusted EBITDA different from EBITDA?

EBITDA is calculated directly from the income statement by adding back interest, taxes, depreciation, and amortization to net income. It still includes owner-specific expenses, personal costs run through the business, and one-time charges that will not recur. Adjusted EBITDA applies a second layer of normalization to remove those items, producing a figure that represents what the business would earn under a hypothetical arm’s-length owner. The difference between the two figures is the total addback schedule, and that difference multiplied by the applicable EBITDA multiple directly determines the enterprise value premium.

How do you calculate adjusted EBITDA?

Adjusted EBITDA is calculated by starting with net income, adding back interest expense, taxes, depreciation, and amortization to reach reported EBITDA, then adding back non-recurring and owner-specific expenses and making downward adjustments for above-market or one-time revenue items. Common addbacks include above-market owner compensation, personal expenses through the business, one-time legal or advisory fees, and non-cash charges. Each addback must be supported by documentation. The resulting adjusted EBITDA is then multiplied by an appropriate industry multiple to produce an indicated enterprise value.

What expenses can be added back to EBITDA?

Expenses that can be added back to EBITDA in a business valuation or sale process include: owner compensation above or below market rate (adjusted to the market cost of a replacement manager); one-time legal fees, settlement costs, or advisory fees that have been paid and will not recur; personal expenses run through the business such as personal vehicle costs, personal travel, or family member expenses; non-cash charges such as stock compensation expense or impairment write-downs; and related-party expenses paid at above-market rates. Each addback must be specific, documented, and genuinely non-recurring to withstand buyer scrutiny.

Why do buyers push back on seller addbacks?

Buyers push back on seller addbacks because every dollar of accepted addback increases the purchase price by the applicable EBITDA multiple, making the quality of addback documentation a direct financial interest. Buyers hire independent accountants to conduct a quality of earnings review specifically to verify that addbacks are real, non-recurring, properly quantified, and not the result of revenue pull-forward or accounting policy changes that artificially improved the seller’s trailing results. Addbacks that cannot be supported with primary documentation are reversed, and the purchase price is reduced accordingly.

What is a quality of earnings report?

A quality of earnings report is an independent accounting analysis conducted on behalf of the buyer during due diligence that examines the seller’s financial statements and addback schedule to assess the accuracy, sustainability, and recurrence of reported earnings. The QoE identifies revenue recognition risks, verifies that addbacks are legitimate, checks for working capital anomalies, and confirms that the trailing twelve months of results are representative of ongoing operations. QoE findings often lead to purchase price adjustments, escrow requirements, or representation and warranty insurance conditions in the definitive agreement.

How does owner compensation affect adjusted EBITDA?

Owner compensation is the most common single addback in middle-market business appraisals because many business owners pay themselves at levels that differ significantly from the market cost of a professional manager performing the same role. If an owner takes a $600,000 salary in a business that would hire a CEO for $250,000, the $350,000 excess is added back to EBITDA. Conversely, if an owner takes a $50,000 salary and extracts the rest through distributions, a downward adjustment is applied to reflect the true market cost of replacing the owner’s labor, which reduces adjusted EBITDA below reported EBITDA.

Do downward adjustments ever reduce adjusted EBITDA below reported EBITDA?

Yes. Downward adjustments reduce adjusted EBITDA when the seller’s reported results include one-time revenue events, below-market expenses, or accounting decisions that temporarily inflated earnings. Common examples include a one-time government contract that will not be renewed, a year in which the owner took no salary, below-market rent paid to a related landlord, or revenue recognized early through contract restructuring. Buyers apply downward adjustments aggressively during QoE because they represent financial risk the buyer will absorb if the inflated results do not repeat after closing.

How much does a business appraisal with EBITDA normalization cost?

A business appraisal from Sofer Advisors that includes full EBITDA normalization and addback documentation for a sale or recapitalization transaction typically ranges from $7,500 to $25,000 depending on the company’s revenue, industry, and the number and complexity of normalization adjustments required. Most standard valuation engagements are completed in four to eight weeks from document receipt. For a fee estimate based on your specific business and transaction, contact Sofer Advisors.

When should a business owner prepare an adjusted EBITDA schedule?

A business owner should prepare a documented adjusted EBITDA schedule at least twelve months before beginning a sale or recapitalization process. Preparing it in advance gives the owner time to clean up personal expenses run through the business, establish compensation at a market-rate level that minimizes the adjustment required, resolve any non-recurring items that are still open, and build a three-year track record of clean financials that buyers will accept without aggressive QoE pushback. Arriving at a sale process with a pre-prepared addback schedule supported by documentation significantly reduces the risk of purchase price reduction at the definitive agreement stage.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

Adjusted EBITDA is a normalized earnings metric that removes non-recurring, owner-specific, and non-cash items from reported EBITDA to reveal the true repeatable operating cash flow a business generates under arm’s-length ownership. The difference between reported and adjusted EBITDA, multiplied by the applicable industry EBITDA multiple, directly determines how much enterprise value a seller’s addback schedule adds to or subtracts from the purchase price. Buyers verify every addback through a quality of earnings review during due diligence, and unsupported adjustments are reversed with a direct impact on the final price. In a formal business appraisal, normalization adjustments are applied following AICPA and ASA standards, producing a documented adjusted EBITDA that satisfies IRS audit requirements, lender underwriting, and buyer QoE scrutiny. Sofer Advisors prepares independent business appraisals with full EBITDA normalization for middle-market sellers and buyers across all industries, with ABV and ASA credentialed oversight on every engagement.

What Should You Do Next?

If you are preparing to sell your business or respond to a buyer’s quality of earnings review, having a credentialed appraiser document your adjusted EBITDA before the sale process begins is the single most effective step you can take to protect the purchase price between letter of intent and closing. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals prepare independent business appraisals with full EBITDA normalization analysis for middle-market business owners across all industries. Schedule your free consultation to understand your business’s adjusted EBITDA baseline and how it translates to enterprise value.

People Also Read

- EBITDA Multiple for Business Valuation by Industry

- Quality of Earnings Report: What Buyers Discover Before a Sale

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}