Last Updated: April 2026

A revenue multiple valuation is a method that prices a business by multiplying its annual revenue by an industry-specific factor derived from comparable market transactions. Unlike earnings-based approaches, it does not require the company to be profitable. Enterprise value (EV) divided by revenue, also written as EV/Revenue, produces a value estimate that reflects what buyers pay relative to top-line performance, independent of cost structure or margin. According to the AICPA (2023), this method falls within the market approach to business valuation.

At Sofer Advisors, we apply the revenue multiple method alongside other market approach techniques to produce defensible valuations for transactions and buy-sell agreements. Understanding when this method is appropriate before entering any deal is essential.

Sellers often prefer revenue multiples because they produce higher implied values for pre-profit companies, while buyers prefer EBITDA multiples because they tie value to cash generation. Knowing which method governs your transaction gives you a negotiating advantage before the first offer.

Key Takeaways

- Revenue Multiple Definition – the EV/Revenue method divides enterprise value by annual revenue, reflecting what buyers pay for top-line performance regardless of profitability.

- When to Use It – revenue multiples apply to pre-profit companies, SaaS businesses, and acquisitions driven by market share rather than earnings capacity.

- Industry Ranges – SaaS typically 4x to 10x ARR; professional services 0.5x to 1.5x; manufacturing and distribution 0.3x to 1.0x depending on gross margin and growth.

- Key Limitation – the revenue multiple ignores profitability; two businesses with identical revenue but different margins produce materially different EBITDA multiples and cash flow value.

- Standard Valuation Cost – a business valuation engagement including market approach analysis typically costs $7,500 to $25,000 and takes four to eight weeks.

Each of these interacts with transaction context. The sections below examine each in detail.

What Is the Revenue Multiple Method?

The revenue multiple method prices a company by applying an industry-derived multiplier to its annual revenue, producing an enterprise value estimate without requiring positive earnings. It is used in M&A transactions, brokerage sales, and investor due diligence for companies with strong revenue but thin or negative earnings before interest, taxes, depreciation, and amortization (EBITDA). The method reflects what comparable businesses have sold for as a function of top-line performance.

Formally, the calculation is EV divided by trailing twelve months (TTM) revenue or annual recurring revenue (ARR). Appraisers source data from transaction databases such as DealStats and BVR, which track actual sale prices for private company transactions across industries and size ranges. According to the Pepperdine Private Capital Markets Report (2024), revenue multiples remain the primary pricing benchmark for lower middle market deals where EBITDA data is incomplete or inconsistent.

Sofer Advisors, with dual ABV and ASA accreditation recognized by the IRS and SEC, applies revenue multiple analysis alongside EBITDA and discounted cash flow (DCF) methods to triangulate a defensible conclusion across transaction types. Firms such as Stout and Kroll use the same multi-method framework in institutional engagements. The weight assigned to each method depends on what the data supports, the purpose of the valuation, and the profile of the company being valued.

When Should You Use Revenue Multiples?

Revenue multiples are most appropriate when EBITDA is negative, near zero, or distorted by owner compensation, growth-phase expenses, or one-time costs a buyer will not inherit. In those cases, an EBITDA multiple either produces an unusable result or dramatically understates value. Revenue multiples provide a more stable anchor when the top line is strong and predictable, giving buyers and sellers a common reference point for early negotiations.

The three most common scenarios where revenue multiples outperform EBITDA multiples are:

- Pre-profit companies – growth-mode businesses where EBITDA is negative because sales, marketing, and headcount investment exceeds current revenue; the revenue base reflects future earning potential

- SaaS and recurring revenue businesses – SaaS companies are routinely priced at 4x to 10x ARR because recurring contracts reduce revenue risk; EBITDA multiples are avoided when customer acquisition costs depress near-term earnings

- Strategic acquisitions – buyers purchasing for market share, customer lists, or geographic coverage anchor offers to revenue rather than profitability, making the revenue multiple the operative metric

How Does Revenue Multiple Compare to EBITDA?

The revenue multiple ignores profitability; the EBITDA multiple does not. A company with high revenue but thin margins appears more valuable under a revenue multiple than under an EBITDA multiple, which is why the choice of method directly affects the implied sale price. Buyers and sellers frequently argue for different methods during negotiations depending on where the value is concentrated in the target company.

| Factor | Revenue Multiple | EBITDA Multiple |

|---|---|---|

| Input | Annual revenue (TTM or ARR) | Normalized EBITDA |

| Best for | Pre-profit, high-growth, SaaS | Established, profitable businesses |

| Ignores | Profitability, cost structure | Revenue scale, growth trajectory |

| Typical range | 0.3x to 10x+ (varies by sector) | 3x to 10x (most private companies) |

| Valuation standard | Market approach | Market approach |

An EBITDA multiple is the default in most private transactions because it directly reflects cash generation. The revenue multiple is a substitute used when EBITDA is unreliable. Applying one without understanding the other leaves an owner exposed in negotiations where the counterparty understands both.

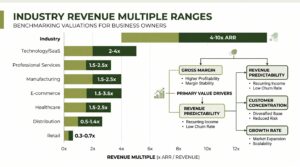

What Revenue Multiples Apply by Industry?

Revenue multiples vary significantly by industry, gross margin, growth rate, and revenue predictability. High-margin, recurring-revenue businesses command the highest multiples; capital-intensive or commoditized businesses command the lowest. Applying an average without controlling for these factors produces an indefensible valuation. According to the IBBA Market Pulse Report (2024), small business transactions clustered between 0.4x and 0.8x revenue, with the top quartile driven by recurring contracts and low customer concentration.

| Industry | Typical Revenue Multiple |

|---|---|

| SaaS / Software | 4x to 10x ARR |

| Healthcare Services | 1x to 3x |

| Professional Services | 0.5x to 1.5x |

| Manufacturing | 0.4x to 1.0x |

| Distribution / Logistics | 0.3x to 0.8x |

| Retail / Consumer | 0.3x to 0.7x |

These ranges are starting points. A professional services firm with 80 percent gross margin and long-term retainers commands a multiple near the top of its range; one billing hourly with high client concentration sits near the bottom. Comparable selection and qualitative adjustments determine where any specific business falls.

How Is a Revenue Multiple Calculated?

The revenue multiple is calculated by dividing the enterprise value of comparable sold transactions by their annual revenue, identifying the median or mean multiple across that comparable set, and applying that figure to the subject company’s TTM or projected annual revenue. The resulting estimate represents enterprise value before adjusting for cash, debt, and working capital to arrive at equity value available to the seller at closing.

Enterprise value in the comparable transaction set reflects the total consideration paid: equity purchase price plus assumed debt minus cash. Appraisers apply filters before selecting comparables (industry classification, revenue size, geographic market, transaction type, and date) to ensure the multiple reflects genuinely similar businesses and current market conditions. An unfiltered industry average applied without these controls is one of the most common errors in informal business valuations and broker rule-of-thumb estimates.

Three variables determine which revenue figure is used. TTM revenue is standard for stable businesses. Projected twelve-month (NTM) revenue applies to high-growth companies where the forward trend matters more than history. ARR is used for SaaS businesses with high revenue predictability and low churn. Selecting the wrong input shifts the implied value significantly and often forms the basis of valuation disputes between buyer and seller at the term sheet stage of a transaction.

What Limits the Revenue Multiple Method?

The revenue multiple method should not be used as the sole valuation approach for profitable, stable businesses where EBITDA is reliable. It ignores the efficiency with which revenue converts to earnings. Profitability differences between two companies with identical revenue can justify a two-to-three-times difference in EBITDA multiple and a materially different sale price in the final negotiation, which is why the method must be chosen carefully for each engagement.

The three scenarios where revenue multiples produce unreliable results are:

- Profitable, stable businesses – when normalized EBITDA is available and consistent, the EBITDA multiple produces a more precise result because it reflects actual cash flow capacity

- Capital-intensive businesses – manufacturers and distributors with significant fixed asset requirements are better valued using EBITDA or an asset approach, because revenue does not capture the capital deployed

- Declining revenue – applying a market multiple to declining top-line performance embeds future risk; a DCF analysis better captures that risk through explicit projections and a risk-adjusted discount rate

Experienced appraisers use the revenue multiple as one input in a multi-method framework. An independent appraiser with access to institutional transaction databases produces a more defensible result than rule-of-thumb estimates.

Frequently Asked Questions

What is a revenue multiple in business valuation?

A revenue multiple is a valuation metric calculated by dividing enterprise value by annual revenue (EV/Revenue). It reflects what buyers pay relative to top-line performance, independent of profitability. Appraisers use it as a market approach method when EBITDA is unavailable or unreliable, most commonly for SaaS companies, pre-profit businesses, and strategic acquisitions. An independent appraiser applies the method when revenue patterns, not earnings, are the most defensible indicator of value.

What is a good revenue multiple for a small business?

A good revenue multiple depends on industry, gross margin, growth rate, and revenue predictability. Most main street businesses sell at 0.3x to 1.5x revenue, professional services firms at 0.5x to 1.5x, and SaaS companies with strong ARR at 4x to 10x. The multiple is only meaningful when compared to verified transactions involving genuinely similar companies. Without credentialed comparable selection, the multiple is speculative regardless of the range it lands in.

How is a revenue multiple different from an EBITDA multiple?

A revenue multiple (EV/Revenue) divides enterprise value by annual revenue and ignores profitability. An EBITDA multiple (EV/EBITDA) divides enterprise value by normalized earnings and reflects cash generation capacity. Revenue multiples apply to pre-profit or high-growth companies; EBITDA multiples apply to established, profitable businesses. Both fall within the market approach but measure different aspects of value. Choosing the right one depends on whether cash generation or revenue scale better represents the business being valued.

What industries use revenue multiples for valuation?

Revenue multiples are most commonly used in SaaS and software, healthcare services, professional services, and marketing or media with recurring contract revenue. Manufacturing, distribution, and retail are more commonly valued on EBITDA multiples because earnings are more stable. Strategic acquirers in any industry may apply revenue multiples when purchasing for market share. The method selected reflects both the company profile and the transaction rationale behind the deal.

How do you calculate a revenue multiple?

Divide the enterprise value of a comparable sold company by its annual revenue to identify the observed multiple. Apply the median or mean across a selected set of comparables to the subject company’s TTM, ARR, or projected revenue. The result is an estimated enterprise value. Adjust for cash, debt, and working capital to arrive at equity value for the seller.

Can a revenue multiple be used for a business that is not profitable?

Yes. The revenue multiple method is specifically designed for companies where EBITDA is negative, near zero, or distorted by growth-phase costs. It values top-line performance independently of profitability, making it the primary method for pre-revenue startups, SaaS companies with high customer acquisition costs, and businesses in growth mode. Investors and strategic buyers accept revenue multiples for these companies because the top line is the most reliable forward indicator of value creation.

What does a 3x revenue multiple mean?

A 3x revenue multiple means a buyer is willing to pay three dollars for every dollar of annual revenue. If a company generates $2 million in revenue and sells at 3x, the implied enterprise value is $6 million. This is above average for most traditional businesses but below average for healthcare services or SaaS with strong recurring revenue. Gross margin and growth rate ultimately determine whether the multiple is justified for any specific business.

How do gross margins affect the revenue multiple?

Gross margin is the single most important driver of revenue multiple variation within an industry. A company with 70 percent gross margin justifies a higher multiple than one with 30 percent at the same revenue level, because more of each revenue dollar converts to potential earnings. Ignoring margin differences is a systematic source of valuation error. Two companies at identical revenue but different margins should not receive the same multiple under any defensible analysis.

How much does a business valuation cost?

A business valuation engagement including market approach analysis typically costs $7,500 to $25,000 depending on firm, capital structure complexity, and report depth. Engagements for litigation, buy-sell agreements, or regulatory compliance require a full appraisal report. Turnaround is generally four to eight weeks from the date all financial materials are received. Sofer Advisors provides full-scope appraisal reports meeting IRS, ESOP, and court-admissibility standards for all formal valuation purposes.

When should a business owner get a revenue multiple valuation?

A business owner should obtain a revenue multiple valuation when preparing for a sale, evaluating an offer, entering a partner buyout, or planning an exit strategy. It is also useful when EBITDA fluctuates year to year. An independent appraisal establishes a defensible baseline before entering any negotiation. An independent appraisal also protects the owner when an unsolicited offer anchors the conversation to a multiple that favors the buyer.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

The revenue multiple method values a business by multiplying annual revenue by an industry-derived factor, producing an enterprise value estimate independent of profitability. It is most reliable for SaaS companies, pre-profit businesses, and strategic acquisitions. EBITDA multiples remain the default for profitable, established businesses. Industry ranges vary from 0.3x for retail to 10x for high-growth SaaS, and the appropriate multiple depends on gross margin, growth rate, and customer concentration.

What Should You Do Next?

If you are preparing to sell, evaluating an offer, or entering a partner buyout, knowing which valuation method governs your transaction is the first step. Applying the wrong multiple can cost you significantly more than the cost of an independent appraisal.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides business valuation services for transactions, buy-sell agreements, and strategic planning. Schedule a consultation to discuss the right valuation method for your business.

People Also Read

- EBITDA Multiple for Business Valuation by Industry

- WACC for Business Valuation: Calculation and Application

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}