Last Updated: April 2026

A leveraged recapitalization is a transaction in which a company takes on new debt and uses the proceeds to repurchase equity, pay a special dividend to shareholders, or buy out a co-owner. The owner receives cash without selling the business outright, while retaining operational control and a continuing equity stake. According to the AICPA (2023), the resulting capital structure is assessed through the market approach and income approach during valuation.

At Sofer Advisors, we advise owners on the valuation, structuring, and capital stack implications of leveraged recapitalizations for partner buyouts, estate liquidity events, and partial exits. Understanding when this transaction produces the intended result, and when it materially increases risk, is essential before signing a term sheet with a lender or private equity partner.

Owners frequently consider a leveraged recapitalization when they want liquidity now without giving up the company. The decision hinges on free cash flow stability, lender appetite, and the owner’s tolerance for operating under covenant-heavy debt. Knowing which conditions support the structure and which disqualify it saves months of wasted deal process.

Key Takeaways

- Leveraged Recapitalization Definition – the company takes on new debt and distributes the proceeds to shareholders as a dividend or equity repurchase while the owner retains control.

- When to Use It – partner buyouts, estate liquidity events, and partial exits where the owner wants cash without selling operational control.

- Typical Debt Multiples – total debt ranges from 3x to 6x EBITDA depending on industry, cash flow stability, and lender risk appetite.

- Key Risk – higher debt service reduces operating flexibility; a downturn in EBITDA can trigger covenant violations and force restructuring.

- Standard Valuation Cost – a business valuation supporting a leveraged recapitalization typically costs $7,500 to $25,000 and takes four to eight weeks.

Each of these interacts with capital structure and lender terms. The sections below examine each in detail.

What Is a Leveraged Recapitalization?

A leveraged recapitalization is a capital structure transaction in which a company replaces a portion of its equity with new debt and pays the proceeds to shareholders. The owner extracts cash from the business without selling to a third party, while the company assumes a higher debt-to-equity ratio and accepts the ongoing interest burden. The transaction is commonly used for partner buyouts, estate planning liquidity, and partial exits where the owner wants to de-risk personally while continuing to operate.

Formally, the transaction adds senior bank debt, unitranche, or mezzanine financing to the balance sheet and uses that capital to fund a dividend, redeem shares, or buy out a minority partner. According to the Pepperdine Private Capital Markets Report (2024), lower middle market leveraged recapitalizations typically close at 3x to 5x EBITDA in total debt, with pricing tied to prevailing senior secured rates plus a margin based on risk profile.

Sofer Advisors, with dual ABV and ASA accreditation recognized by the IRS and SEC, provides valuations supporting leveraged recapitalization transactions and capital structure decisions. Firms such as Stout and Kroll deliver the same analysis in institutional engagements. The valuation opinion establishes the fair market value used to set the dividend or share redemption price, documents the arm’s-length basis of the transaction, and justifies the structure to lenders and tax authorities.

How Does a Leveraged Recapitalization Work?

A leveraged recapitalization works by sourcing new debt against the company’s cash flows and assets, then distributing the proceeds to shareholders through a cash dividend, stock repurchase, or partner buyout. The business continues to operate under existing management, but the capital structure shifts materially toward debt. Lenders underwrite the transaction based on the company’s ability to service the new debt from free cash flow under both base-case and downside scenarios.

The typical transaction sequence runs through five steps:

- Valuation and capacity analysis – an independent appraiser determines fair market value and debt capacity based on EBITDA, fixed charge coverage, and industry norms

- Lender selection – the company solicits term sheets from senior banks, unitranche lenders, or mezzanine providers based on required proceeds and covenant tolerance

- Due diligence – the lender completes quality of earnings, legal, and collateral diligence over six to ten weeks

- Documentation and closing – credit agreements and security documents are finalized and funded simultaneously with the dividend or redemption

- Post-close monitoring – the company reports covenant compliance quarterly and manages debt service through the amortization schedule

According to the Federal Reserve Senior Loan Officer Opinion Survey (2024), bank lending standards for leveraged transactions tighten materially during periods of economic uncertainty, which directly affects both available proceeds and pricing.

Leveraged Recapitalization vs LBO: Key Differences?

A leveraged recapitalization and a leveraged buyout (LBO) both rely on significant debt financing, but they serve different purposes and have different ownership outcomes. A leveraged recapitalization is initiated by the existing owner to extract cash while retaining control. An LBO is initiated by a buyer, typically a private equity sponsor, to acquire the company outright. The underlying economic mechanics of the debt overlap substantially, but the strategic intent and change-of-control implications differ fundamentally between the two transaction types.

| Factor | Leveraged Recapitalization | Leveraged Buyout (LBO) |

|---|---|---|

| Initiated by | Existing owner | Outside buyer (typically PE) |

| Ownership outcome | Owner retains control | Buyer gains majority or full control |

| Use of proceeds | Dividend to owner / partner buyout | Purchase of seller’s equity |

| Typical debt multiple | 3x to 5x EBITDA | 4x to 6x+ EBITDA |

| Management | Existing team continues | May change per buyer thesis |

| Tax treatment | Dividend or capital gain to owner | Capital gain to seller |

The practical distinction matters because the transactions produce different risk profiles for the owner. In a leveraged recapitalization, the owner keeps the upside of future growth but now operates a more leveraged balance sheet. In an LBO, the seller exits entirely and transfers all forward risk to the acquiring party.

What Are the Types of Recapitalization?

Recapitalizations take several forms depending on the capital source and the strategic goal. Leveraged recapitalization is one variant within a broader category of capital structure transactions that are used to restructure the balance sheet without triggering a full ownership change. The type selected depends on whether the owner wants cash, needs new equity partners, or is restructuring existing debt obligations.

| Type | Capital Source | Primary Use |

|---|---|---|

| Leveraged Recapitalization | New debt | Dividend, partner buyout, estate liquidity |

| Equity Recapitalization | New equity (often PE minority) | Growth capital, partial exit |

| Dividend Recapitalization | Incremental debt | One-time cash distribution |

| Debt Refinancing | Replacement debt | Lower cost or extended maturity |

| Restructuring Recapitalization | Debt-to-equity conversion | Avoid bankruptcy, deleverage |

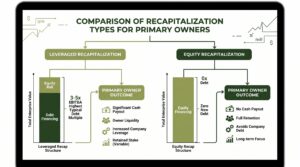

Comparison of recapitalization types as a vertical bar chart, leveraged at highest typical debt multiple (3-5x EBITDA), equity recap at zero new debt, annotated with primary owner outcome for each.

The choice is rarely binary. Many transactions combine a leveraged recapitalization with a minority equity investment from a private equity firm, producing a partial cash exit for the owner plus a growth partner for the business. The resulting hybrid is commonly called an “equity recapitalization with leverage” and is structured to match both the owner’s liquidity goal and the company’s growth plan.

When Do Companies Use Leveraged Recapitalizations?

Companies use leveraged recapitalizations when the owner wants personal liquidity but the business is not a candidate for a full sale, either because the owner wants to continue operating or because market conditions do not favor an exit. The transaction also supports specific estate and partner-buyout scenarios where a third-party sale would create tax or operational complications for existing stakeholders.

The three most common scenarios are:

- Partner buyouts – one owner exits while the other continues operating; the company borrows to fund the departing partner’s equity purchase without bringing in an outside buyer

- Estate liquidity events – a family-owned business funds estate taxes, buys out heirs, or rebalances ownership among next-generation shareholders using debt rather than an outside sale

- Partial exits with growth retention – the owner takes cash off the table for diversification while continuing to benefit from the upside of the remaining equity stake

A leveraged recapitalization also serves as a defensive tactic when an owner wants to discourage an unsolicited acquisition approach, reducing the company’s attractiveness to opportunistic buyers while returning capital to the existing shareholder base.

What Are the Risks of Leveraged Recapitalization?

The primary risk of a leveraged recapitalization is that the increased debt service reduces the company’s ability to absorb a downturn in EBITDA. A business that comfortably served 2x debt under the old structure may struggle at 5x if revenue declines or a key customer is lost. Covenant violations can trigger mandatory prepayments, repricing, or lender-imposed operational restrictions that strip management flexibility at exactly the wrong time.

The three scenarios where leveraged recapitalizations produce poor outcomes are:

- Cyclical or concentrated businesses – companies with volatile earnings or heavy customer concentration cannot sustain covenant-heavy debt; a single quarter of weak performance can cascade into default

- Aggressive debt multiples – taking maximum leverage when lender terms allow 6x+ removes the cushion needed for a downturn; conservative structures at 3x to 4x preserve flexibility

- Weak covenant packages – springing maintenance covenants, limited cure rights, and tight fixed charge coverage ratios convert normal business volatility into lender events

These risks are why experienced appraisers recommend a stress-tested valuation before committing. Modeling debt service against a 15 to 20 percent EBITDA decline exposes whether the structure holds under a realistic recession scenario or whether the owner is overreaching for liquidity.

Frequently Asked Questions

What is a leveraged recapitalization in simple terms?

A leveraged recapitalization is when a company borrows money and uses the cash to pay the owner or buy back shares, instead of selling the business. The owner gets liquidity, keeps control, and the company takes on more debt. It is most commonly used for partner buyouts, estate planning, and partial exits where the owner wants cash without fully exiting.

How is a leveraged recapitalization different from an LBO?

A leveraged recapitalization is initiated by the existing owner to extract cash while retaining control of the business. A leveraged buyout (LBO) is initiated by an outside buyer, typically a private equity firm, to acquire the company outright. Both use significant debt, but the outcomes differ: the owner stays in a recapitalization, while the owner exits in an LBO. The tax treatment and strategic purpose also differ substantially.

What is the purpose of a leveraged recapitalization?

The primary purpose is to provide liquidity to the owner without requiring a sale of the business. Owners also use it to fund partner buyouts, estate planning obligations, family ownership transitions, or personal diversification. A secondary purpose is defensive: adding leverage can deter hostile acquisition approaches by reducing the company’s attractiveness to outside buyers while returning capital to existing shareholders.

How much debt can a company take on in a leveraged recapitalization?

Total debt typically ranges from 3x to 5x trailing twelve months EBITDA for lower middle market companies, with upper middle market deals reaching 5x to 6x depending on industry, cash flow stability, and lender appetite. The appropriate level depends on fixed charge coverage, customer concentration, and cyclicality. Aggressive multiples above 5x remove the cushion needed to absorb a downturn without triggering covenant violations.

What are the tax implications of a leveraged recapitalization?

Tax treatment depends on whether proceeds are distributed as a dividend, stock redemption, or sale of shares to a co-owner. Dividends are generally taxed as ordinary income or qualified dividends depending on structure. Stock redemptions can qualify for capital gains treatment if they meet the IRS substantially disproportionate tests. Coordinate closely with an experienced tax advisor before selecting the structure.

What types of lenders finance a leveraged recapitalization?

Senior bank lenders, unitranche funds, mezzanine providers, and business development companies all participate in leveraged recapitalization financing. Senior banks offer the lowest cost of capital but the most restrictive covenants. Unitranche lenders combine senior and subordinated debt in a single instrument, trading higher pricing for simpler structure. Mezzanine debt fills the financing gap between senior capacity and total required proceeds.

Can a small business do a leveraged recapitalization?

Yes, though the mechanics and cost of capital differ from upper middle market deals. Small businesses with at least $1 million to $3 million in EBITDA and stable free cash flow can access senior secured debt and unitranche financing from regional banks, SBA lenders, and specialty lenders. Below that size, transaction cost often outweighs the benefit and a traditional sale is more practical.

What valuation method is used for a leveraged recapitalization?

Appraisers typically apply a combination of the income approach (discounted cash flow) and the market approach (comparable public company and transaction multiples) to establish fair market value. The opinion supports the dividend or share redemption price, justifies the transaction to lenders, and documents fair value for tax and reporting purposes. The valuation also informs the covenant structure proposed by the lender.

How much does a business valuation cost?

A business valuation supporting a leveraged recapitalization typically costs $7,500 to $25,000 depending on capital structure complexity, report depth, and whether the engagement requires litigation support. Engagements for formal appraisal reports, litigation, or regulatory compliance sit at the upper end of the range. Turnaround is generally four to eight weeks from the date all financial materials are received. Contact Sofer Advisors to scope your engagement.

When should a business owner consider a leveraged recapitalization?

An owner should consider a leveraged recapitalization when they want personal liquidity but are not ready for a full exit, when they need to buy out a partner or fund estate obligations, or when they want to diversify wealth while retaining upside. The transaction is most appropriate for companies with stable EBITDA, low customer concentration, and strong free cash flow.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

A leveraged recapitalization uses new debt to distribute cash to shareholders while the owner retains control. It is most useful for partner buyouts, estate liquidity, and partial exits where a full sale is undesirable. Typical debt multiples run 3x to 5x EBITDA, with upper middle market transactions reaching 6x. The primary risk is that increased debt service reduces the company’s ability to absorb an EBITDA downturn. A stress-tested valuation and conservative capital structure preserve the flexibility the owner is trying to buy.

What Should You Do Next?

If you are considering a leveraged recapitalization for a partner buyout, estate liquidity event, or partial exit, begin with an independent valuation and a debt capacity analysis. These two inputs determine whether the transaction is feasible and what proceeds are realistic before you engage a lender.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides business valuation services supporting leveraged recapitalization transactions, partner buyouts, and capital structure planning. Schedule a consultation to discuss the right approach for your business.

People Also Read

- What Is a Leveraged Buyout? LBO Structure Explained

- What Is a Recapitalization? Business Owner’s Guide

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}