Last Updated: April 2026

A recapitalization is a corporate finance transaction in which a company restructures the composition of its capital, adjusting the balance between debt and equity in its balance sheet to achieve a specific ownership, liquidity, or financing objective. The restructuring can involve taking on new debt to pay shareholders a special dividend, issuing new equity to retire existing debt, selling a controlling or minority stake to a financial sponsor, or combining these strategies. Recapitalizations are used by privately held business owners to achieve partial liquidity without a full sale, by private equity firms to optimize post-acquisition capital structure, and by management teams executing buyouts of operating divisions from larger parent companies.

For business owners evaluating ownership transition options, a recapitalization offers a path to liquidity, balance sheet strength, or succession that a conventional sale does not always provide. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides independent business appraisals that establish the defensible fair market value required to negotiate recapitalization terms, satisfy lender and investor due diligence, and document enterprise value for tax and estate planning purposes in middle-market transactions nationwide.

Understanding which type of recapitalization fits a business owner’s objectives and what valuation role each structure requires is the foundation of any successful capital restructuring plan. The Key Takeaways below summarize the core mechanics before the detailed analysis that follows.

Key Takeaways

- Recapitalizations Change Capital Structure Without a Full Exit: A recap restructures the debt and equity mix of a business, enabling owners to extract partial liquidity, transfer ownership to management or financial sponsors, or optimize the balance sheet without requiring a complete sale of the business.

- Leveraged Recaps Use Debt to Fund Shareholder Liquidity: In a leveraged recapitalization, the business takes on new senior debt and distributes the proceeds to existing shareholders as a special dividend, allowing owners to monetize a portion of their equity while retaining operational control and future upside.

- PE-Sponsored Recaps Combine Partial Exit with Growth Capital: When a private equity firm acquires a majority stake, the existing owner typically receives cash at close for the sold portion and retains a minority equity interest, participating in a future full sale at a higher valuation once the sponsor’s value creation plan is executed.

- Valuation Is Required at Every Stage of a Recap: Lenders require an independent business appraisal to underwrite new debt, investors require fair market value to price the equity purchase, and tax and estate planning require a credentialed appraisal to document the value transferred at each stage.

- The Right Recap Structure Depends on the Owner’s Objectives: Liquidity, succession, growth capital, and tax efficiency each point toward different recapitalization structures; an independent business appraisal establishes the equity value baseline from which each alternative is evaluated and compared.

Each of these structures creates different economic outcomes for the business owner depending on how much liquidity is extracted, how much operational control is retained, and what the post-recap capital structure implies for the business’s future growth and eventual exit. The sections below examine how each major recapitalization type works, why owners choose them, and where business valuation enters the process.

What Is a Recapitalization?

A recapitalization restructures a company’s capital composition without necessarily transferring full ownership to a new buyer. Unlike a conventional sale, in which all equity changes hands at a single closing price, a recapitalization allows the current owner to remain involved in the business to varying degrees while achieving a specific financial objective, whether liquidity, debt reduction, succession, or growth funding. The mechanics of each recap are determined by what problem the owner is trying to solve and what capital structure the business’s existing and projected cash flows can support.

| Recap Type | Primary Objective | Capital Source | Owner’s Post-Recap Role |

|---|---|---|---|

| Leveraged (Debt-Funded) | Shareholder liquidity via special dividend | New senior debt | Retains majority equity and operational control |

| Equity | Debt reduction and balance sheet cleanup | New equity issuance | Diluted ownership stake but debt-free balance sheet |

| PE-Sponsored Majority Buyout | Partial exit plus growth capital | PE equity plus debt | Minority equity holder, rolls into next sale event |

| Management Buyout (MBO) | Succession and management ownership | Debt plus management equity | Exits partially or fully at closing |

| Dividend Recapitalization | Sponsor liquidity in a PE-owned company | New debt in existing PE-owned entity | PE sponsor is the primary beneficiary |

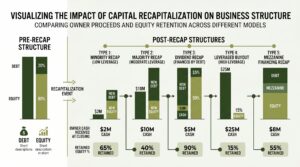

Recapitalizations are classified by the direction in which the debt and equity balance moves. A leveraged recap increases debt and reduces effective equity concentration by monetizing owner equity through borrowed funds. An equity recap decreases debt by issuing new ownership, diluting existing equity. A PE-sponsored recap combines both: a portion of equity is sold, new debt is added, and the resulting capital structure supports the sponsor’s operating and exit strategy.

What Are the Main Types of Recapitalization?

The type of recapitalization a business pursues is determined by its cash flow profile, the owner’s liquidity needs, the availability of credit, and whether institutional capital is involved. Middle-market business owners most frequently encounter five recapitalization structures:

- Leveraged recapitalization: The business borrows senior debt, secured against its assets and cash flows, and uses the proceeds to pay the existing shareholders a special dividend. The owner retains equity ownership and operational control but receives immediate liquidity without selling a single share. Lenders typically require the business to demonstrate sufficient earnings before interest, taxes, depreciation, and amortization (EBITDA) coverage to service the new debt.

- Equity recapitalization: The business issues new shares to investors, typically to raise capital for growth, acquisitions, or to repay debt that has become unsustainable. Existing shareholders are diluted but the balance sheet is strengthened. Equity recaps are common in businesses emerging from overleveraged conditions or entering a capital-intensive growth phase.

- Private equity-sponsored recapitalization: A PE firm acquires a majority ownership stake, providing the seller with a significant cash distribution at closing while the seller retains a minority equity position, typically 10% to 40%, in the recapitalized entity. This structure gives the seller immediate liquidity on the majority of their equity and the opportunity to participate in a second liquidity event when the PE firm exits.

- Management buyout recapitalization: The company’s existing management team acquires ownership from the current owner, typically funded through a combination of senior debt, subordinated debt, and management equity. The prior owner exits fully or partially, and management becomes the equity owner of the recapitalized entity.

- Dividend recapitalization: A PE-owned company takes on new debt, the proceeds of which are distributed to the PE sponsor as a dividend rather than reinvested in the business. This structure allows the sponsor to return capital to their limited partners without selling the company, but it increases leverage and reduces the cushion available to the business if earnings decline.

Why Do Business Owners Choose Recapitalization?

Business owners choose recapitalizations when a full sale is either undesirable or premature and a conventional sale does not address the specific objective they are trying to achieve. Common owner objectives that lead to a recapitalization rather than a sale include the following:

- Partial liquidity without full exit: The owner wants to monetize a portion of the equity built over many years without giving up the business entirely, often because they believe significant value creation remains ahead.

- Succession to management: The owner wants to transition the business to a management team that has earned the right to own it, and a management buyout provides the mechanism without requiring management to fund the entire purchase price from personal assets.

- Balance sheet optimization: Excess equity capital that could be returned to shareholders is sitting in the business; a leveraged recap extracts it efficiently while the business continues to operate under its existing management and strategy.

- Growth capital: The owner needs additional capital to fund an acquisition, expand facilities, or invest in technology, and an equity recap or PE partnership provides access to institutional capital without requiring a full sale.

- Estate and succession planning: Recapitalizing a portion of the business into a new entity or transferring shares at a documented fair market value creates the structure needed for orderly generational transfer at defensible tax values.

According to AICPA Forensic and Valuation Services (2023), middle-market PE-sponsored recapitalizations have grown as a preferred alternative to full sales among business owners aged 55 to 65 who want to derisk personal wealth while maintaining operational involvement in businesses they spent decades building.

What Is Leveraged Recapitalization?

A leveraged recapitalization is the most common recapitalization structure for privately held middle-market businesses because it allows owners to extract liquidity without any change in ownership percentage or operational control. The business borrows senior secured debt, typically from a bank or private credit fund, at a multiple of EBITDA that the lender determines the business’s cash flows can support. The borrowed proceeds are distributed to the owner as a special dividend. After the distribution, the owner holds the same equity percentage as before closing but the business now carries a debt obligation that must be serviced from operating cash flows.

For a business generating $3 million in annual EBITDA, a lender willing to advance 3.0 times EBITDA would provide $9 million in new debt. After transaction costs, the owner receives approximately $8 million in cash while retaining 100% of the equity. If the business later sells for $25 million, the owner receives the full equity proceeds on the sale minus the outstanding debt balance. The leveraged recap effectively allows the owner to take a portion of their equity value off the table without triggering a sale at the current price, while remaining positioned to benefit from future value creation.

According to the American Society of Appraisers (ASA) (2024), lenders providing leveraged recap financing require an independent business appraisal confirming the enterprise value and normalized EBITDA used to calculate the debt multiple, because the business’s asset value and cash flow coverage are the primary collateral supporting the loan.

Schedule your free consultation with Sofer Advisors to understand your business’s current fair market value and how much equity you could extract through a leveraged recapitalization without compromising the business’s ability to service new debt. Discover The Sofer Difference.

What Is a PE-Sponsored Recapitalization?

A private equity-sponsored recapitalization, often called a PE recap or majority recapitalization, is a transaction in which a PE firm acquires a majority ownership stake, typically 60% to 80%, in a privately held company, distributing the purchase price for that stake to the existing owner while the owner retains a minority equity position. The PE firm brings institutional capital and operational resources with the goal of growing the business and selling it at a higher multiple within three to seven years. The owner participates in that second exit as a minority equity holder.

For business owners who built significant value and want partial liquidity but believe the business has meaningful future upside, the PE recap is frequently the most economically attractive structure. The owner receives a cash distribution at close representing the majority of their equity value, eliminates personal concentration risk in a single illiquid asset, and retains meaningful participation in the next sale. The retained minority equity, often called a rollover equity position, is typically the most lucrative equity the owner has ever held because it is backed by institutional capital, a professional management team, and a defined exit horizon.

According to Bain and Company’s Global Private Equity Report (2024), the median holding period for PE-backed companies before exit is approximately 5.1 years, making the PE recap’s rollover equity a defined-horizon investment rather than an open-ended illiquid position. That defined timeline is what separates a PE recap from simply selling a minority stake to a passive investor.

The critical negotiation point in a PE recap is the valuation used to price the equity at closing. PE firms model their acquisition price on projected EBITDA at an exit multiple, which means the owner’s cash distribution at close depends entirely on the credibility of the normalized EBITDA baseline used to anchor the deal price. An independent appraisal that documents adjusted EBITDA and supports the concluded enterprise value reduces the information asymmetry between the owner and the PE firm and protects the owner from accepting a discounted purchase price based on conservative buyer assumptions.

How Does Valuation Support Recapitalization?

Business valuation serves three distinct functions in a recapitalization. First, the pre-recap appraisal establishes the enterprise value and normalized EBITDA that anchors the deal price, whether the recap involves lender underwriting, a PE firm’s equity pricing, or a management team’s buyout financing. Without an independent appraisal, each of these parties sets the price from their own model with their own assumptions, and the owner negotiates without a verified reference point. A credentialed appraisal from Sofer Advisors provides that reference point with ABV and ASA oversight on every engagement.

Second, for tax and estate planning purposes, the appraisal documents the fair market value of equity transferred or sold at each stage of the recapitalization. Transfers of ownership that occur at prices materially below independently appraised fair market value may be recharacterized by the IRS as partial gifts, creating unintended gift tax exposure. Credentialed firms including Kroll and Stout provide transaction appraisals in large-cap recapitalizations; for middle-market owners, Sofer Advisors provides business valuation for mergers and acquisitions with direct ABV and ASA credentialed oversight that satisfies lender, investor, and IRS documentation standards in the same engagement.

Third, the weighted average cost of capital (WACC) analysis embedded in the valuation report models how the proposed post-recap capital structure affects the business’s cost of capital and, therefore, its value. Adding leverage reduces the equity cost of capital through the tax shield on interest deductions but increases financial risk; the WACC analysis helps both the owner and the lender or investor understand whether the proposed debt load is appropriate for the business’s risk profile and cash flow profile. This analysis is particularly important in leveraged recapitalizations where the debt service coverage ratio determines how much equity the owner can actually extract.

Frequently Asked Questions

What is a recapitalization in simple terms?

A recapitalization is a restructuring of how a business is financed, specifically the mix of debt and equity it carries. Rather than selling the entire business, the owner adjusts the capital structure to achieve a specific goal, such as extracting personal liquidity through new debt, reducing debt by issuing new equity, or selling a majority stake to a private equity firm while retaining a minority position. The business continues operating under the same name and management, but its financing structure and ownership composition change.

Why would a company do a recapitalization?

Companies recapitalize to solve a specific financial or ownership problem that a conventional sale does not address. Common reasons include: an owner who wants partial liquidity without a full exit; a management team that wants to buy ownership from the founder through a leveraged buyout; a business that needs growth capital without a sale; or an owner who wants to optimize the balance sheet by replacing expensive equity with lower-cost tax-deductible debt. Each objective leads to a different recapitalization structure with different financing sources and ownership outcomes.

What are the types of recapitalization?

The five main types used in middle-market transactions are leveraged recapitalization, in which the business borrows against its assets to pay the owner a special dividend; equity recapitalization, in which new equity is issued to retire debt; PE-sponsored majority recapitalization, in which a PE firm buys a controlling stake and the owner retains minority equity; management buyout, in which the management team acquires the business using debt and personal equity; and dividend recapitalization, in which a PE-owned company takes on new debt to pay the sponsor a distribution without selling the business.

How does a leveraged recapitalization work?

In a leveraged recapitalization, the business borrows senior debt based on a multiple of its EBITDA, typically two to four times EBITDA in middle-market transactions, and distributes the cash proceeds to the owner as a special dividend. The owner retains 100% of the equity and operational control after closing, but the business now carries new debt that must be serviced from operating cash flows. The owner’s effective net wealth increases by the after-tax amount of the dividend, while the business’s equity value decreases by the same debt amount added to the balance sheet, producing no immediate change in total enterprise value.

What is rollover equity in a PE recapitalization?

Rollover equity is the minority ownership stake the selling owner retains after a PE firm acquires the majority of the business. Rather than receiving 100% cash at closing, the owner sells, for example, 70% of the business for cash and rolls the remaining 30% into equity in the recapitalized entity alongside the PE firm. The rollover equity participates in the PE firm’s exit three to seven years later, typically at a higher valuation if the sponsor’s value creation plan succeeds. Most financial advisors describe rollover equity as the best equity an owner will ever hold because it is backed by professional capital with a defined exit timeline.

What taxes apply to a recapitalization?

Tax treatment depends on the recapitalization type. In a leveraged recap, the special dividend the owner receives is taxed as a dividend, at qualified dividend rates if certain holding period conditions are met, or as ordinary income if not. In a PE majority recap structured as a stock sale, the cash proceeds are generally taxed as long-term capital gain if the owner held equity for more than one year. Rollover equity received in exchange for contributed equity is often tax-deferred under IRC 721 (partnership contributions) or IRC 351 (corporate contributions). Each structure requires independent tax analysis before closing.

Does a recapitalization require a business appraisal?

Yes, in most cases. Lenders providing leveraged recap financing require an independent business appraisal to confirm enterprise value and EBITDA coverage. PE firms require valuation support to document the equity purchase price and satisfy their own investor reporting obligations. Estate and gift tax planning associated with equity transfers in a recap requires a qualified appraisal meeting IRS standards under Treasury Regulation 1.170A-17. Even in a management buyout, lenders and the management team both need an independently established value to negotiate from a common reference point.

How long does a recapitalization take to complete?

A middle-market recapitalization typically requires three to six months from initial planning to closing, depending on the complexity of the transaction, the number of parties involved, and the time required for lender or investor due diligence. A leveraged recap with a single lender tends to close faster; a PE-sponsored majority recap involving financial sponsor diligence, management presentations, and legal document negotiation typically runs four to six months. The independent business appraisal, which anchors the deal price and satisfies lender and investor due diligence requirements, is typically completed in four to eight weeks from document receipt.

How much does a business valuation for a recapitalization cost?

A business appraisal from Sofer Advisors for a recapitalization transaction typically ranges from $7,500 to $25,000 depending on the company’s revenue, industry, and the complexity of the capital structure analysis required to support lender underwriting or PE equity pricing. Most standard recapitalization appraisals are completed in four to eight weeks from document receipt. For a fee estimate based on your specific transaction, contact Sofer Advisors.

When is a recapitalization better than a full sale?

A recapitalization is typically the better choice when the owner believes significant value creation remains in the next three to five years and wants to participate in it, when the owner is not ready to exit fully but needs personal liquidity now, when no acceptable full-sale buyer exists at the current price, or when the owner wants to fund management succession without requiring management to raise full purchase price financing independently. A full sale is better when the owner wants complete liquidity, is ready to exit all operational involvement, and the current market is providing attractive multiples relative to projected future performance.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

A recapitalization restructures a company’s capital composition, adjusting the balance between debt and equity to achieve a specific ownership, liquidity, or financing objective without requiring a complete sale of the business. The five primary structures used in middle-market transactions are leveraged recapitalization, equity recapitalization, PE-sponsored majority buyout, management buyout, and dividend recapitalization, each serving a different owner objective. Independent business valuation anchors every stage of the recapitalization process: it supports lender underwriting, establishes the equity price PE investors pay, satisfies IRS documentation requirements for tax and estate planning, and provides the WACC analysis that models whether the proposed debt load is appropriate for the business’s risk profile. Sofer Advisors provides recapitalization appraisals and capital structure analysis for middle-market business owners across all industries, with ABV and ASA credentialed oversight on every engagement.

What Should You Do Next?

If you are evaluating a recapitalization as an alternative to a full sale, understanding your business’s current enterprise value and normalized EBITDA is the starting point for every conversation with a lender, PE firm, or management team. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals, recapitalization baseline valuations, and capital structure analysis for middle-market business owners navigating leveraged recaps, PE partnerships, and management buyouts across all industries. Schedule your free consultation to understand what your business is worth and which recapitalization structure fits your liquidity, succession, and growth objectives.

People Also Read

- WACC for Business Valuation: Calculation and Application

- Business Valuation for Mergers: Buy-Side vs Sell-Side

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}