Last Updated: April 2026

ASC 820 is the Financial Accounting Standards Board’s authoritative guidance on fair value measurement. It defines fair value as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. According to FASB, ASC 820 does not tell companies which assets to measure at fair value; it establishes how that measurement must be performed once another standard requires it.

At Sofer Advisors, we perform ASC 820 fair value analyses for business combinations, equity compensation plans, and impairment testing. The measurement date, the hierarchy level selected, and the documentation of inputs all affect whether an analysis withstands audit review. Getting these elements right at the outset avoids costly restatements.

Private company owners encounter ASC 820 more often than they realize. Any transaction involving a business combination, equity award, or impairment test triggers the standard. Understanding which hierarchy level governs your assets and what documentation auditors expect is the first step before commissioning any fair value analysis.

Key Takeaways

- Definition – ASC 820 defines fair value as the exit price received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.

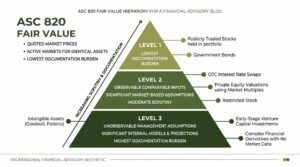

- Three-Level Hierarchy – Level 1 uses quoted market prices for identical assets, Level 2 uses observable comparable inputs, and Level 3 relies on unobservable management assumptions including discounted cash flow models.

- Private Company Default – most private company assets have no active market, placing them at Level 2 or Level 3 where documented assumptions and independent appraisals are required.

- Common Applications – ASC 820 applies in business combinations (ASC 805), equity compensation grants (ASC 718), goodwill impairment testing (ASC 350), and financial instrument disclosures under GAAP.

- Valuation Cost – a fair value analysis supporting ASC 820 typically costs $7,500 to $25,000 depending on asset complexity and the purpose of the engagement.

Each of these components interacts with how auditors and external reviewers evaluate fair value disclosures. The sections below examine each in detail.

What Is ASC 820 Fair Value Measurement?

ASC 820, codified by FASB, defines fair value as an exit price: the price a company would receive to sell an asset, or pay to transfer a liability, in an orderly transaction between market participants on the measurement date. The standard assumes a hypothetical transaction in the principal market for the asset, or the most advantageous market if no principal market exists. It applies whenever another accounting standard requires or permits fair value measurement.

The exit price concept means ASC 820 does not allow companies to measure fair value based on what they paid for an asset or what they believe it is worth internally. According to the PwC Fair Value Measurement Guide (2024), this market-participant perspective is the most common source of errors in private company analyses, because management naturally values assets on internal projections rather than observable market pricing assumptions. Fair value reflects the exit price, not the owner’s intended use or replacement cost.

What Are the Three Levels of Fair Value?

ASC 820’s fair value hierarchy ranks the inputs used to measure fair value from most reliable (Level 1) to least reliable (Level 3). The ranking reflects how observable inputs are in the market, and therefore how verifiable they are by auditors. A company must use the highest level of inputs available for any given measurement and disclose which level governs each item in the financial statement notes.

The three levels are:

- Level 1 Inputs – quoted prices in active markets for identical assets or liabilities accessible at the measurement date; the most reliable and requires no adjustment

- Level 2 Inputs – observable inputs other than Level 1, including prices for similar assets, interest rates, and yield curves; requires some adjustment for differences between the asset being measured and the observable comparable

- Level 3 Inputs – unobservable inputs based on the entity’s own assumptions about what market participants would use; includes DCF models, projected revenue multiples, and internally developed data not corroborated by external sources

The hierarchy determines disclosure scope and auditor scrutiny. Level 3 measurements require reconciliations of opening and closing balances, descriptions of unobservable inputs, and sensitivity analysis. Auditors test every assumption in a Level 3 model, including the discount rate, projected cash flows, and any control premium or minority discount. Companies that cannot defend Level 3 inputs with independent appraisal support face restatement risk and additional audit procedures on related balance sheet items.

Which Level Applies to Private Companies?

Private companies operate almost entirely at Level 2 and Level 3 because their assets have no quoted market prices. A private company’s equity is not exchange-traded, its customer relationships have no observable market price, and its real property is valued by comparables or income models. Level 1 applies only when the company holds publicly traded securities on its balance sheet.

| Asset or Liability | Typical Level | Rationale |

|---|---|---|

| Publicly traded securities | Level 1 | Quoted price in active market |

| Interest rate swaps | Level 2 | Observable yield curve inputs |

| Customer relationships | Level 3 | No market; requires income approach |

| Trade names and patents | Level 3 | Internally developed royalty model |

| Goodwill (impairment test) | Level 3 | Reporting unit DCF model |

| Real estate (privately held) | Level 2 or 3 | Comparables vs. appraised income model |

| Equity compensation (409A) | Level 3 | Option pricing model with private inputs |

Operating at Level 3 means private companies carry the full burden of documenting every model assumption. Unlike public companies with observable market prices, private companies must support discount rates, revenue projections, and obsolescence assumptions with industry data and comparable transaction evidence. National advisory firms such as Stout and Kroll perform the same Level 3 analyses in institutional-scale M&A transactions. Sofer Advisors delivers the same independent appraisal layer for private companies requiring audit-ready documentation without the cost structure of a national firm.

When Does ASC 820 Apply to a Private Company?

ASC 820 applies whenever GAAP requires fair value measurement and the company follows GAAP, either because it has audited financial statements, lender debt covenants requiring full GAAP compliance, or is preparing for a sale. The standard does not require all assets to be measured at fair value; it applies only where another standard invokes fair value as the measurement basis.

The four most common triggering events are:

- Business Combination (ASC 805) – all acquired assets and assumed liabilities must be measured at fair value at the acquisition date, including intangibles such as customer relationships, trade names, technology, and non-compete agreements

- Equity Compensation (ASC 718) – stock options and equity awards require a fair value measurement of the underlying equity at the grant date, typically performed through a 409A valuation following ASC 820 principles

- Goodwill Impairment Testing (ASC 350) – companies with goodwill must test it for impairment at least annually by measuring the fair value of the reporting unit under ASC 820

- Financial Instruments (ASC 825) – certain debt instruments, derivatives, and convertible notes carried or disclosed at fair value trigger ASC 820 measurement requirements

According to Carta (2024), equity compensation grants are among the most frequent initial triggers for ASC 820 compliance at growth-stage private companies, where the 409A valuation is often the first formal fair value analysis commissioned. That analysis establishes the documentation framework drawn on when the company later encounters ASC 820 in a business combination or impairment test. Owners who understand which trigger applies and what hierarchy level it requires can scope engagements accurately and avoid audit delays from undocumented Level 3 inputs.

What Valuation Methods Does ASC 820 Require?

ASC 820 does not mandate a specific valuation method; it requires the selected method to be appropriate for the asset and maximize observable inputs at the highest available hierarchy level. Three approaches are recognized under ASC 820: the market approach, the income approach, and the cost approach. The selection depends on the asset’s nature, available market data, and the applicable hierarchy level.

The three approaches are:

- Market Approach – uses prices from market transactions involving identical or comparable assets; most appropriate for Level 1 and Level 2 measurements where observable comparables exist

- Income Approach – converts expected future cash flows to present value using a market-based discount rate; most commonly applied to customer relationships, trade names, and reporting unit goodwill at Level 3

- Cost Approach – reflects the cost to replace an asset’s service capacity net of obsolescence; used for specialized equipment, assembled workforce, and assets where future cash flows are difficult to isolate

In practice, appraisers apply more than one approach to the same asset and reconcile the results. For intangible assets in a purchase price allocation, the income approach is almost always primary because customer relationships and trade names generate identifiable cash flows discounted via relief-from-royalty or excess earnings methodology. Sofer Advisors applies all three approaches across ASC 820 engagements, selecting the method that maximizes observable inputs and reduces audit exposure on Level 3 measurements.

Getting the hierarchy level right and documenting every input before audit fieldwork begins is the difference between a clean opinion and a restatement process. An independent credentialed appraisal is the most efficient way to satisfy auditor requirements for Level 3 estimates in any triggering event.

Frequently Asked Questions

What is ASC 820 in simple terms?

ASC 820 is the GAAP standard that defines how to measure fair value when another accounting rule requires it. Fair value is the price you would receive to sell an asset or pay to transfer a liability in an orderly market transaction today. ASC 820 establishes three levels of inputs, from most reliable quoted prices to least reliable management assumptions, creating a consistent framework for how that measurement is performed and disclosed.

What is the fair value hierarchy under ASC 820?

The hierarchy has three levels. Level 1 uses quoted prices in active markets for identical assets. Level 2 uses observable inputs other than Level 1, such as prices for similar assets or yield curves. Level 3 uses unobservable inputs based on management’s assumptions about what market participants would use. A company must use the highest level available and disclose which level governs each measurement in the financial statement footnotes.

What triggers ASC 820 for a private company?

ASC 820 is triggered whenever another GAAP standard requires fair value measurement. Common triggers include a business acquisition (ASC 805) requiring purchase price allocation; annual goodwill impairment testing (ASC 350); equity compensation grants (ASC 718); and financial instrument disclosures (ASC 825). Any of these events requires the company to follow ASC 820’s input hierarchy and disclosure rules in the financial statements.

What is the difference between fair value and fair market value?

Fair value under ASC 820 and fair market value under IRS and 409A standards are related but legally distinct. Fair value is an exit price based on market participant assumptions in an orderly GAAP transaction. Fair market value is the price at which property would change hands between a willing buyer and seller, neither under compulsion. The two produce similar conclusions in most cases but diverge for minority interests, control premiums, and the discount for lack of marketability in private company equity contexts.

Does ASC 820 apply to all private companies?

ASC 820 applies to private companies required to prepare GAAP financial statements, including those with lender covenants requiring GAAP compliance, audited statements for investor or transaction purposes, or companies preparing for a sale. Private companies with equity compensation plans, goodwill on the balance sheet, or multiple owners with differing valuation interests will almost always encounter ASC 820 measurement requirements during normal operations.

What disclosures does ASC 820 require?

Financial statements must disclose the hierarchy level for each fair value measurement, the valuation techniques and inputs used, and any transfers between levels during the period. For Level 3 measurements, companies must also provide a reconciliation of opening and closing balances, a description of unobservable inputs, and sensitivity of the estimate to changes in those inputs. Companies should review disclosure requirements with their auditors before each reporting period closes.

Can a private company use in-house valuations for ASC 820?

A private company can use an in-house team if it has relevant expertise and the analysis is sufficiently documented. In practice, most auditors require independent third-party appraisals for Level 3 measurements because management cannot objectively verify its own assumptions. For purchase price allocations and goodwill impairment testing, auditors routinely engage their own valuation specialists to review or reperform the analysis, making an independent appraisal the more defensible starting point.

How much does an ASC 820 valuation cost?

An ASC 820 fair value analysis typically costs $7,500 to $25,000 depending on the number and complexity of assets, the triggering event (business combination, impairment test, or equity compensation), and documentation depth required. Engagements involving multiple intangible assets, litigation support, or contested valuations sit at the upper end. Turnaround is generally four to eight weeks from receipt of all financial and operational data. Contact Sofer Advisors to scope your engagement.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

ASC 820 establishes how fair value must be measured whenever GAAP requires it. The three-level hierarchy ranks inputs from quoted market prices to management assumptions, with Level 3 carrying the highest documentation burden. Private companies operate almost entirely at Level 2 and Level 3 because their assets lack observable market prices. The standard is triggered by business combinations, equity compensation grants, goodwill impairment testing, and financial instrument disclosures. An independent appraisal from a credentialed professional reduces audit risk and supports the footnote disclosures required in GAAP financial statements.

What Should You Do Next?

If your company is planning an acquisition, issuing equity awards, or carries goodwill subject to annual impairment testing, begin with an ASC 820 scoping conversation before your next audit cycle. Understanding which hierarchy level governs your assets and what documentation auditors require is the difference between a clean audit opinion and a restatement.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides fair value analyses for business combinations, goodwill impairment testing, and equity compensation under ASC 820. Schedule a consultation to discuss the right approach for your business.

People Also Read

- 409A Valuation vs. Fair Market Value: Key Differences Explained

- Goodwill Impairment Testing Under ASC 350: Complete Guide

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}