Last Updated: April 2026

A leveraged buyout (LBO) is an acquisition in which a buyer, typically a private equity (PE) firm, uses a combination of equity and substantial borrowed capital, often 60% to 80% of the total purchase price, to acquire a company, with the acquired business’s own cash flows expected to service and repay the debt over the holding period. LBOs are one of the most common transaction structures in middle-market and large-cap mergers and acquisitions (M&A), making them a critically important concept for any business owner evaluating exit options, fielding offers from financial sponsors, or trying to understand what a PE firm’s acquisition inquiry actually means for their company’s value and future.

For business owners navigating a potential LBO inquiry, understanding the deal structure, how the buyer models returns, and what drives the offer price is essential for evaluating whether the terms reflect genuine enterprise value. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides independent business appraisals that give sellers the analysis they need to assess LBO offers, negotiate from a position of informed certainty, and meet IRS, lender, and transaction requirements.

The mechanics of an LBO, including the financing layers, return targets, and valuation methodology the buyer applies, are not simply financial engineering. Each component directly affects what the buyer is willing to pay, how earnout and rollover provisions are structured, and what the seller ultimately takes home.

Key Takeaways

- Debt-Driven Structure: LBOs typically use 60% to 80% debt and 20% to 40% equity, with the acquired company’s own operating cash flows servicing the debt over a 4- to 7-year holding period.

- Private Equity Buyers: Most LBOs are executed by PE firms targeting an internal rate of return (IRR) of 20% to 30%, a threshold that directly constrains how much the buyer is willing to pay at entry.

- Target Characteristics: LBO candidates typically have stable, recurring cash flows, established market positions, and earnings before interest, taxes, depreciation, and amortization (EBITDA) margins that support the debt service coverage required by lenders.

- Seller Implications: Sellers in an LBO transaction typically receive a premium over standalone value, but deal structure, post-close earnouts, and management rollover requirements all affect net proceeds at closing.

- Independent Valuation: A credentialed independent appraisal helps sellers verify the offer price reflects true enterprise value, not merely the buyer’s leverage capacity and return model.

Understanding these fundamentals matters for any business owner who receives an LBO inquiry, evaluates a private equity offer, or is preparing for a business exit planning process. The sections below examine each component of an LBO, from deal structure to financing layers to valuation mechanics, so that sellers can engage more effectively with buyers and advisors.

What Is a Leveraged Buyout?

A leveraged buyout is the acquisition of a company funded primarily with debt rather than the buyer’s own capital, structured so that the acquired company’s cash flows repay the borrowings over time. The term “leveraged” reflects the financial leverage applied: by using borrowed capital to fund the majority of the purchase price, the buyer can acquire a business that would otherwise require far more equity capital, amplifying both the potential return and the risk if the business underperforms. The buyer retains a smaller equity stake but controls the business and captures the remaining value after debt repayment.

LBOs are most commonly executed by private equity firms, which pool investor capital into funds and deploy it across a portfolio of acquisitions. The PE firm acquires the target, installs or retains management, implements operational improvements, grows EBITDA, and eventually exits via a strategic sale, secondary buyout to another PE firm, or initial public offering (IPO). The equity invested at entry is expected to grow in value through EBITDA growth, debt paydown, and multiple expansion over the holding period, which typically spans four to seven years.

How Does an LBO Work?

An LBO follows a defined sequence of steps that begins with target identification and ends with an exit event. The sequence is consistent whether the deal is a $20 million middle-market transaction or a multi-billion-dollar large-cap acquisition; the difference lies in the financing sources, number of parties, and regulatory complexity involved. Understanding each step helps a business owner anticipate what a PE firm is doing during due diligence, why certain financial questions are asked, and how the offer price is ultimately derived.

The core steps in a typical LBO process are as follows, each building directly on the prior:

- Step 1 — Target identification: The PE firm screens for businesses that meet its investment criteria, including EBITDA size, industry sector, growth profile, management quality, and free cash flow consistency.

- Step 2 — Letter of intent (LOI): After initial diligence, the firm submits a non-binding offer letter outlining the indicative price, structure, and key conditions. The LOI typically triggers an exclusivity period.

- Step 3 — Due diligence: The buyer conducts detailed financial, legal, tax, and operational review. Quality of earnings (QoE) analysis is standard; independent valuations may be ordered for specific assets.

- Step 4 — Financing commitments: The PE firm arranges debt financing from senior lenders, mezzanine providers, or other capital sources, with commitments conditioned on the deal closing.

- Step 5 — Closing: The acquisition closes, ownership transfers, the target’s balance sheet is loaded with the deal debt, and the PE firm’s equity is invested through a new holding company structure.

- Step 6 — Value creation period: The PE firm works with management to grow revenue and EBITDA, optimize working capital, reduce costs, and service debt over the holding period.

- Step 7 — Exit: The firm sells the business at a higher EBITDA multiple or higher absolute EBITDA, ideally achieving the target IRR for its fund investors.

Each step in this sequence creates pressure on specific financial metrics, and business owners who understand the model can position their companies more strategically before and during a sale process.

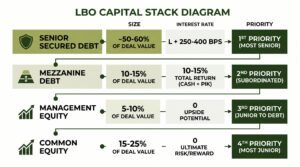

What Financing Structure Does an LBO Use?

The financing structure of an LBO, often called the capital stack, consists of multiple layers of debt and equity ranked by seniority, each with different interest rates, risk profiles, and repayment terms. The composition of the capital stack varies by deal size, industry, and market conditions, but the general hierarchy is consistent. Senior debt has the first claim on assets and cash flows in a default, carries the lowest interest rate, and represents the largest portion of the purchase price; equity sits at the bottom of the stack, absorbs first losses, but also captures the residual upside when the business is sold.

The typical layers of an LBO capital stack, from most senior to most junior:

- Senior secured debt: First-lien bank loans or term loans, typically 3.0x to 4.5x EBITDA; lowest cost, highest priority in liquidation; often provided by commercial banks or direct lenders.

- Senior unsecured / unitranche debt: Second-lien or blended first-and-second-lien facilities; higher interest rate than senior secured; increasingly common in middle-market LBOs.

- Subordinated or mezzanine debt: Hybrid instruments with higher interest rates and sometimes equity warrants; subordinated to senior debt but senior to equity; often used to bridge the gap between available bank debt and required equity.

- Preferred equity: Used in some structures as a quasi-debt layer with preferred return rights ahead of common equity holders; less common in straightforward LBOs.

- Common equity: The PE firm’s invested capital, representing 20% to 40% of the purchase price; residual claim on business value after all debt is repaid.

The interaction between these layers determines the total debt load the business must service, which in turn constrains the maximum purchase price the PE firm can offer while still achieving its target IRR.

What Is the Purpose of a Leveraged Buyout?

The purpose of an LBO depends on which party is being considered. For the PE firm, the primary objective is financial return: by using leverage, the firm amplifies the equity return on its invested capital. If a business is acquired at 8x EBITDA and sold at 9x EBITDA after five years of EBITDA growth and debt repayment, the equity return can be multiples of what would have been earned in an all-cash acquisition at the same price. For this reason, leveraged buyouts allow PE funds to generate the 20% to 30% IRR that their limited partner investors require.

For the seller, the purpose of accepting an LBO offer is typically to achieve a full exit at a price that reflects the business’s going-concern value, often at a premium to what a strategic buyer would pay in a competitive process. Sellers who receive LBO offers from multiple PE firms benefit from a competitive auction, which tends to drive offer prices higher. According to Bain & Company‘s Global Private Equity Report (2024), PE-backed buyouts globally averaged approximately 5.6x debt/EBITDA leverage, with middle-market transactions typically ranging from 4.0x to 6.5x depending on industry and cash flow stability. Understanding where your business falls in that range helps frame realistic price expectations.

For the broader market, LBOs provide liquidity to business owners who want to exit fully, give management teams a path to co-invest alongside a PE firm and share in future upside, and drive operational improvements that can increase the long-term value of businesses before they are eventually sold again to a strategic acquirer.

Schedule your free consultation with Sofer Advisors to understand how your business would be modeled in a leveraged buyout, what entry multiple a buyer might apply, and how an independent appraisal protects your negotiating position. Discover The Sofer Difference.

How Is a Business Valued in an LBO?

LBO valuation is distinct from traditional discounted cash flow (DCF) or market approach valuation because the entry price is partially constrained by the financing available, not just by the intrinsic value of the business. A PE firm builds an LBO model that starts with the proposed entry price, layers in the capital stack, projects EBITDA growth and cash flow generation over the holding period, applies an exit multiple, and solves backward to determine whether the deal achieves the target IRR. If the model does not produce the required return at a given entry price, the buyer lowers the offer, not the return requirement.

According to the AICPA Forensic and Valuation Services (2023), LBO acquisition multiples in middle-market transactions typically range from 6x to 10x EBITDA, with the specific entry multiple constrained by the leverage available, the sponsor’s return hurdle, and the business’s demonstrated cash flow consistency. This is meaningfully different from how a strategic buyer values the same business, since a strategic acquirer can underwrite synergies and cost savings that a financial buyer cannot. Business owners considering a sale should understand which type of buyer is making the offer and how the valuation methodology differs, as the type of buyer directly affects the price and structure. Credentialed valuation firms including Kroll and DFIN provide transaction advisory and financial analysis in large-cap LBO transactions; for middle-market sellers, Sofer Advisors provides independent fairness opinions and buy-side vs sell-side valuation analysis to ensure the offer price is defensible and well-informed.

| LBO (Financial Buyer) | Strategic Acquisition | SPAC Merger | |

|---|---|---|---|

| Buyer type | Private equity firm | Corporate acquirer | Blank check company |

| Valuation basis | Entry multiple + leverage + IRR model | Synergy-adjusted DCF or comparable company | Negotiated enterprise value at merger agreement |

| Typical EBITDA multiple | 6x to 10x (middle market) | 7x to 13x (synergy premium possible) | Varies widely; often 10x to 15x for growth targets |

| Post-close structure | Debt-loaded balance sheet; PE ownership | Absorbed into acquirer; standalone division or subsidiary | Public company; PE-like sponsor promotes retained |

| Seller liquidity | Full exit at close (or partial rollover) | Full exit typically at close | Partial; subject to redemption mechanics |

| Best for seller when | Clean exit at premium; no strategic fit required | Strategic fit exists and synergies justify premium | High-growth narrative; willing to accept public market risk |

What Does an LBO Mean for Business Sellers?

For a business owner receiving an LBO offer, the headline price is only one component of the economic outcome. Several structural features common to LBO transactions affect what the seller ultimately receives, and each should be reviewed carefully with legal, tax, and valuation advisors before signing a letter of intent.

According to PitchBook (2024), the median holding period for PE-backed businesses before exit is approximately 5.1 years, which means a seller who rolls over a portion of their equity into the new deal structure is committing to a multi-year path to liquidity. Understanding the rollover percentage, preferred return structure, and exit rights is as important as the headline enterprise value in evaluating the total deal economics.

The key seller-side considerations in an LBO transaction:

- Management rollover: PE firms frequently require sellers who remain in management to reinvest 10% to 30% of their proceeds into the new equity structure, aligning incentives but deferring full liquidity.

- Earnout provisions: Buyers may structure a portion of the purchase price as contingent on future financial performance, reducing closing proceeds and introducing performance risk.

- Representations and warranties: Sellers provide contractual representations about the business; breaches can result in indemnification claims against escrowed or rolled-over proceeds.

- Tax structure: Deal structure as an asset sale versus stock sale has significant income tax consequences for the seller; a pre-sale tax analysis is essential.

- Leverage impact on operations: A business carrying significant post-close debt has less flexibility for capital investment, hiring, or weathering a revenue downturn during the PE holding period.

Each of these provisions interacts with the others, and a seller who evaluates only the headline price without reviewing the full purchase agreement structure may significantly overestimate their net proceeds.

Frequently Asked Questions

What is a leveraged buyout in simple terms?

A leveraged buyout is the acquisition of a business using mostly borrowed money, where the loan is repaid using the acquired company’s operating income rather than the buyer’s own cash. The buyer, usually a private equity firm, invests a smaller amount of equity and borrows the rest, then works to grow the business and repay the debt before selling it at a profit. The structure allows buyers to control large businesses with relatively small equity commitments.

How does an LBO work step by step?

An LBO begins when a PE firm identifies a target business, submits a letter of intent with an indicative price, and conducts due diligence on financial, legal, and operational factors. The firm then arranges debt financing from banks or direct lenders, closes the acquisition by loading debt onto the target’s balance sheet, and works to grow EBITDA and reduce debt over a four- to seven-year holding period. The process ends with an exit, typically a sale to a strategic buyer or another PE firm.

What types of businesses are LBO targets?

Ideal LBO targets have stable, predictable cash flows sufficient to service acquisition debt, established customer relationships with low churn, defensible market positions, experienced management teams willing to remain post-close, and asset-light or capital-efficient operating models. Businesses in sectors with high revenue cyclicality, customer concentration above 20% to 25%, or heavy capital expenditure requirements are generally less attractive LBO candidates because the cash flow available for debt service is less predictable.

What is a typical LBO debt-to-equity ratio?

In a typical middle-market LBO, the capital structure is approximately 60% to 70% debt and 30% to 40% equity, though ratios vary significantly based on industry, market conditions, and the target’s cash flow profile. High-cash-flow businesses with strong EBITDA margins may support debt/EBITDA ratios of 5x to 6x, allowing the buyer to apply higher leverage and achieve better equity returns. Lower-margin or more cyclical businesses will support lower leverage, reducing the maximum affordable purchase price.

How is enterprise value calculated in an LBO?

Enterprise value in an LBO is typically calculated as a multiple of EBITDA, most commonly in the range of 6x to 10x for middle-market companies. The PE firm applies this multiple to the target’s normalized, trailing twelve-month EBITDA to arrive at an entry enterprise value, then subtracts existing debt and adds existing cash to derive the equity value paid to the seller. The multiple used reflects comparable transaction data, the company’s growth profile, and the leverage available, not simply the intrinsic value of the business.

What is the difference between an LBO and a strategic acquisition?

An LBO is made by a financial buyer, typically a PE firm, that does not operate in the same industry and cannot underwrite cost synergies. A strategic acquisition is made by an operating company in the same or adjacent industry that can realize revenue or cost synergies from combining the two businesses. Strategic buyers generally pay higher multiples because synergies justify a larger premium; LBO buyers are constrained by leverage capacity and their IRR return model, which limits how much they can pay.

What happens to employees in a leveraged buyout?

Employee outcomes in an LBO vary widely based on the PE firm’s strategy and the condition of the business. Some PE firms invest aggressively in headcount, technology, and operations to grow EBITDA; others identify cost reduction as the primary value creation lever. For businesses with experienced management teams and strong EBITDA margins, employee continuity is typically prioritized. Business owners who care about employee outcomes post-close should evaluate the PE firm’s operational track record across its prior portfolio companies.

What should a business owner know before agreeing to an LBO?

Before agreeing to an LBO, a business owner should obtain an independent, credentialed business appraisal to verify the offer price reflects genuine enterprise value rather than only what the buyer’s leverage model supports. They should also understand the full economic structure of the deal, including rollover requirements, earnout terms, tax consequences, and representations and warranties provisions. Engaging a valuation professional early in the process, before signing a letter of intent, provides the most negotiating leverage.

How much does a business appraisal for a sale or LBO from Sofer Advisors cost?

A business appraisal from Sofer Advisors for a sale or leveraged buyout transaction typically ranges from $7,500 to $25,000 depending on the company’s revenue, industry complexity, and the number of valuation approaches required. Engagements are generally completed in four to eight weeks from document receipt. For a detailed fee estimate based on your company’s situation, contact Sofer Advisors.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

A leveraged buyout is the acquisition of a business using primarily borrowed capital, with the acquired company’s cash flows repaying the debt over a four- to seven-year holding period. PE firms execute LBOs to amplify equity returns through financial leverage, targeting IRRs of 20% to 30% at entry multiples that typically range from 6x to 10x EBITDA in middle-market transactions. For business sellers, an LBO offer requires careful evaluation of the full economic structure, including rollover requirements, earnout provisions, and tax implications, not just the headline enterprise value. Sofer Advisors provides independent business appraisals and transaction valuation analysis that helps sellers assess LBO offers, verify offer prices against fair market value, and enter negotiations fully informed.

What Should You Do Next?

If your business has received a private equity inquiry or you are preparing for a sale process that may attract financial buyers, an independent appraisal gives you the data to evaluate any LBO offer on its merits. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals, fairness opinions, and transaction valuation analysis for middle-market sellers navigating PE acquisition inquiries and competitive sale processes. Schedule your free consultation to understand what your business is worth and how an LBO buyer would model your company.

People Also Read

- Business Exit Planning Strategies Guide for Owners in 2025

- Business Valuation for Mergers: Buy-Side vs Sell-Side

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}