Last Updated: June 2026

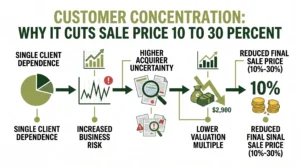

Customer concentration is one of the most consistent and quantifiable deal-killers in small and mid-market M&A. When a single customer generates more than 20% of a business’s revenue, buyers apply a discount. The discount is typically 10% to 20% at the 20%–35% concentration level. It rises to 20% to 30% or more when one customer represents 40%+ of revenue. The discount reflects the buyer’s rational assessment of what happens to cash flow if that relationship ends the week after closing.

The mechanism is simple. A buyer who pays 5x EBITDA for a business generating $1M in EBITDA is paying $5M. If the key customer, who generates 40% of revenue, terminates within 18 months, the business’s EBITDA might drop to $600K. The buyer just overpaid by $2M. Buyers have seen this play out. They price it in upfront. Sofer Advisors helps owners and their advisors work through exactly these questions and turn the analysis into a defensible business valuation they can act on.

The following takeaways summarize the key valuation and transaction factors covered in this guide.

Key Takeaways

- Single Customer Representing 20+ – A single customer representing 20%+ of revenue is flagged in every serious M&A due diligence process.

- Concentration 40 One Customer – Concentration above 40% in one customer typically reduces purchase price 20%–30% and often changes deal structure.

- Lenders Conservative Buyers SBA – Lenders are more conservative than buyers. SBA lenders frequently cap financing at 30% customer concentration. Conventional lenders may decline.

- Longterm Contracts Autorenewal Terms – Long-term contracts with auto-renewal terms and early termination penalties mitigate concentration risk and reduce buyer discounts.

- It Typically Takes 18 – It typically takes 18–36 months of active business development to meaningfully reduce a concentrated revenue base.

- Earnouts Escrow Holdbacks Seller – Earnouts, escrow holdbacks, and seller notes tied to customer retention are common structural responses to concentration.

Each of these factors is examined in depth in the sections that follow.

What Is Customer Concentration and When Does It Become a Problem?

Customer concentration is the degree to which a business’s revenue depends on a small number of customers. The standard metric is the percentage of total annual revenue from any single customer. But buyers and lenders also look at concentration by the top three or top five customers combined.

The 20% threshold is widely used as the first flag. At 20%+, most professional buyers, private equity sponsors, strategic acquirers, and experienced independent operators, will explicitly model what happens if that customer leaves. The analysis is not theoretical. Buyer due diligence typically includes a review of the customer’s contract terms, the length of the relationship, any prior service issues or disputes, the customer’s own financial health, and whether the customer has made comments about changing suppliers.

The 40% threshold is where deals begin to break down or require significant structural accommodation. A business where 40%+ of revenue comes from one customer is, in economic terms, not fully an independent business, it is a sub-contractor to that customer. Buyers who proceed at 40%+ concentration require protections that match the risk.

Some buyers use tiered frameworks:

| Concentration Level | Typical Buyer Response |

|---|---|

| <15% per customer | No adjustment; normal underwriting |

| 15% – 25% per customer | Inquiry and monitoring; minor multiple compression |

| 25% – 40% per customer | 10% – 20% price discount; possible deal structure adjustment |

| 40% – 60% per customer | 20% – 30% price discount; earnout or escrow typically required |

| >60% per customer | Financing often unavailable; deal frequently restructured or declined |

The top-five concentration threshold is also important. A business where no single customer exceeds 20%, but the top five customers represent 80% of revenue, has significant cluster risk. Buyers model that as well.

Analysis at this level is the work of a credentialed valuation professional operating under the AICPA Statement on Standards for Valuation Services, which governs how a defensible conclusion of value is developed and documented.

How Do Buyers Quantify the Concentration Discount?

There is no universal formula. Experienced buyers apply concentration discounts using two methods: a direct multiple reduction or a risk-adjusted cash flow adjustment in the DCF model.

Under the multiple reduction approach, a buyer who would otherwise pay 5x EBITDA reduces the offered multiple to 4x or 3.5x to account for concentration risk. That multiple reduction is equal to a $500K–$750K price reduction on a $1M EBITDA business.

Under the DCF approach, the analyst builds separate revenue scenarios. One where the key customer continues (base case). One where the customer reduces scope by 50% (downside case). One where the customer exits entirely (stress case). The probability-weighted present value across scenarios produces a valuation below the base case. In practice, buyers who use this method tend to produce similar discounts to the multiple reduction approach, they just document it differently.

Sellers often push back by arguing that the key customer has been with them for 10 or 15 years and is not going anywhere. Buyers hear this in every concentrated deal. The correct response from a sophisticated seller is not to argue the point. Produce a long-term contract, a documented renewal history, and references that a buyer can contact during due diligence.

How Do Lenders View Customer Concentration?

Lender underwriting is more conservative than buyer underwriting on concentration risk. SBA lenders, who finance most small business acquisitions, generally apply a hard threshold of 25%–30% customer concentration before reducing the loan amount or declining to finance the deal. Some SBA lenders will not finance a business where one customer represents more than 20% of revenue without meaningful structural support.

Conventional commercial lenders are similarly conservative. A business with 50% concentration in one customer may receive a loan commitment with a significant restriction. If that customer departs post-close, the loan becomes immediately callable or the lender requires excess cash flow to pay down the loan faster. These provisions transfer the concentration risk from the lender back to the borrower. They also limit the buyer’s operational flexibility.

The practical effect for sellers is that concentration limits who can buy the business. A highly concentrated business restricts the buyer pool to all-cash buyers and buyers who can self-finance. That smaller buyer pool reduces competition and, so, price.

What Deal Structures Address Customer Concentration?

When buyers proceed despite meaningful concentration, they use structural protections to allocate the risk. The four most common mechanisms are:

- Earnout tied to customer retention. A portion of the purchase price, often 15%–25% of total consideration, is deferred and paid to the seller over 12–24 months. Payment is contingent on the key customer remaining in good standing and continuing to generate revenue at or above a defined threshold. The earnout protects the buyer if the customer leaves early. It rewards the seller if the customer stays.

- Escrow holdback. Instead of an earnout, a portion of the closing proceeds, typically 10%–15% of purchase price, is held in escrow for 12–18 months. If the key customer terminates during the escrow period, the buyer draws from escrow to cover revenue shortfall. Remaining escrow is released to the seller at the end of the period.

- Seller note with concentration condition. The seller carries a portion of the purchase price as a seller note. The note payment schedule may be accelerated or deferred based on whether the key customer remains active. This aligns the seller’s payout incentive with customer retention through the transition period.

- Reduced upfront price, no earnout. Some buyers simply reduce the headline price to account for the risk and pay cash at closing. Sellers who want certainty of payment often prefer this to earnouts or holdbacks, even if the total consideration is lower.

David Hern CPA ABV ASA, founder of Sofer Advisors, brings a Heart of a Teacher to every engagement – translating complex valuation methodology into clear, actionable guidance that clients can act on before and after the report is delivered. With 15+ years of valuation experience, 11+ expert witness cases across multiple jurisdictions, and 180+ five-star Google reviews, David built Sofer Advisors into an Inc. 5000-recognized firm. The Sofer Difference is a four-phase process of Discovery, Diligence, Analysis, and Delivery that ensures every conclusion is defensible, documented, and tied to the specific facts of the business.

While national firms like Stout and Kroll serve large enterprise clients, Sofer Advisors specializes in middle-market businesses that require personalized attention, direct access to credentialed professionals, and a next business day response policy.

When Is Customer Concentration Acceptable?

Not all concentration is equally risky. The nature of the customer relationship, its contractual basis, renewal history, switching cost, and credit quality, dramatically affects how a buyer views concentration.

A government contract that represents 40% of revenue is different from a commercial customer at 40%. Government contracts are generally competitive bid requirements with defined terms. The “customer” is a regulatory agency with procurement rules that create significant institutional inertia. Buyers discount government concentration much less than commercial concentration.

Blue-chip or investment-grade commercial customers, Fortune 500 companies, major retailers, large health systems, are viewed more favorably than small or private commercial customers. A large customer with strong credit, a multi-year contract, and a procurement relationship rather than a personal one with the owner is less risky than a smaller company where the relationship runs through a personal friendship.

Long-term contracts with meaningful termination penalties and auto-renewal terms are the single strongest mitigation available to sellers. A 5-year contract with a 12-month termination notice requirement effectively gives the business 12 months of protected revenue even if the customer decides to leave. That runway for replacement lets the acquirer manage the risk.

How Long Does It Take to Reduce Customer Concentration?

The standard timeline for a sustained effort is 18–36 months. Not because it is hard to add customers, but because meaningful revenue from new relationships takes time to ramp. Signing a new contract is not the same as generating material revenue from that contract.

The practical point is that sellers who want to sell in 12 months should accept the concentration discount as a deal reality. Sellers who can plan ahead, 2–3 years before intended exit, have the runway to actively pursue new accounts, bring in a business development resource, and document the progress in their CIM.

Buyers are not only looking at current concentration, they are looking at the trend. A business that was 50% concentrated two years ago and is now 30% concentrated shows active management of the risk. A buyer who sees that path will apply a smaller discount than one who sees concentration unchanged over many periods.

How Should Concentration Be Disclosed in a CIM?

A Confidential Information Memorandum (CIM) that buries or obscures concentration data signals poor preparation. Professional buyers will find the concentration in the financial statements, the question is whether they find it with good context or without it.

The correct approach is to address concentration directly in the CIM. Include: (1) the percentage of revenue from the top 1, 3, and 5 customers; (2) the tenure of each relationship; (3) the contract status and term; (4) any steps already taken to reduce concentration; and (5) a clear explanation of why the key customer relationship is durable. Buyers who receive this level of transparency have less reason to apply a panic discount.

The questions below address the most common issues business owners raise before engaging a qualified appraiser for a customer concentration acquisition risk engagement.

Frequently Asked Questions

What percentage of revenue from one customer is too much?

There is no universal rule, but 20% is the standard first flag in M&A due diligence. Above 40%, most buyers apply a meaningful price discount and often require deal structure protections. Above 60%, some buyers decline to proceed altogether.

How much does customer concentration reduce a business sale price?

Concentration in the 25%–40% range typically reduces price 10%–20% relative to a well-diversified comparable business. Concentration above 40% can reduce price 20%–30% or more, depending on the nature of the relationship and the availability of contract mitigation.

Can I still sell my business if I have one big customer?

Yes, but the buyer pool narrows, deal structure becomes more complex, and price is affected. Buyers who are comfortable with concentration risk include strategic acquirers who may already have a relationship with the key customer, and cash buyers who are not limited by lender concentration covenants. The most important step is to have strong contracts and transparent records.

Do long-term contracts eliminate the concentration discount?

Contracts reduce the discount significantly but rarely eliminate it entirely. A 5-year contract with a 12-month termination notice reduces buyer risk materially. Buyers still apply some discount for concentration, but the magnitude is smaller, often in the 5%–10% range versus 20%–30% for month-to-month arrangements.

How do I calculate customer concentration for my business?

Divide annual revenue from each customer by total annual revenue. If your top customer generated $400K of a total $1M in revenue last year, that customer is 40% concentrated. Run this analysis for the top 3 and top 5 customers as well, buyers look at cluster concentration in addition to single-customer concentration.

What is an earnout and how does it relate to concentration?

An earnout is a deferred payment tied to post-close performance. In concentration-heavy deals, the earnout is often specifically tied to whether the key customer stays. The seller receives the deferred payment only if the customer remains active at defined revenue levels during the earnout period, typically 12–24 months.

How do buyers verify whether a key customer will stay?

Buyers typically request customer references, review service agreements, look at renewal history, and sometimes request the ability to contact the customer directly late in due diligence. Sellers who can arrange a brief conversation between a buyer and the key account manager provide the strongest possible reassurance about relationship durability.

Does customer concentration affect business valuation for estate planning?

Yes. In estate and gift tax valuations, customer concentration is a documented risk factor. A credentialed appraiser incorporates it into the discount for lack of marketability or through a direct adjustment to the expected income stream. A business with 50% concentration in one customer will receive a lower valuation than a comparable business with a spread base.

Can customer concentration be mitigated without losing the customer?

Yes. The goal is not to reduce revenue from the key customer, it is to grow revenue from other customers so that the key account becomes a smaller percentage of total revenue. Proactive business development aimed at replicating the key customer relationship with similar-profile accounts is the most effective path.

What happens if I disclose concentration and the buyer uses it against me?

This is a valid concern. The answer is preparation: if you know concentration is an issue, address it proactively in the CIM with contract records, relationship history, and evidence of steps taken before the buyer raises it as a negotiating point. Sellers who control the narrative around concentration are better positioned than sellers who let buyers discover it during diligence.

Related Case Studies

- Business Valuation For Mergers Buy Side Vs Sell Side

- Key Person Discount How Owner Dependence Reduces Business Value

- Business Valuation Mistakes To Avoid What Can Go Wrong

Executive Summary

- Customer concentration above 20% in a single account is flagged in every professional M&A process and applies downward pressure on multiples.

- Buyers discount concentrated revenue 10%–30% depending on severity. Lenders apply even more conservative thresholds and may decline to finance concentrated businesses.

- Long-term contracts with auto-renewal and termination penalties are the most effective structural mitigation available to sellers before going to market.

- Sellers with 2–3 years of runway can meaningfully reduce concentration before a sale. Sellers with 12 months must accept the discount or manage it through deal structure.

What Should You Do Next?

If customer concentration is affecting your business’s valuation or your ability to close a sale, a credentialed valuation professional can quantify the specific impact and identify the structural options available to you. David Hern CPA ABV ASA, founder of Sofer Advisors, holds dual ASA and ABV credentials recognized by the IRS, SEC, and FINRA, with 15+ years of valuation experience and 180+ five-star Google reviews. Schedule a consultation to discuss your business valuation needs.

People Also Read

- Hidden Risk In Atlanta Retirement Plans Annual Valuation Requirements

- Why You Must Start Planning Your Business Exit Now With The Right Valuation Expert

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com/about-us/ or schedule a consultation at soferadvisors.com/contact-us/.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}