Last Updated: April 2026

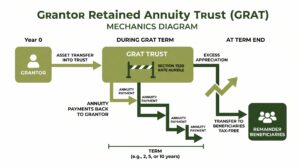

A Grantor Retained Annuity Trust (GRAT) is an irrevocable trust designed to transfer the future appreciation of an asset, including a closely held business interest, to heirs at a significantly reduced or zero gift tax cost. The grantor transfers assets into the trust and retains the right to receive a fixed annuity payment each year for a specified term, typically two to ten years. If the transferred assets grow faster than the IRS-prescribed hurdle rate, known as the Section 7520 rate, the excess appreciation passes to the trust’s remainder beneficiaries, usually children or a dynasty trust, free of additional gift tax. When properly structured and supported by a qualified business appraisal, a GRAT can transfer millions of dollars in business value to the next generation with a taxable gift close to zero.

For business owners, the GRAT strategy depends entirely on the accuracy of the initial business valuation. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides IRS-compliant fair market value appraisals for GRAT funding, ensuring the asset transfer is priced at a defensible value that satisfies gift tax reporting requirements under Treasury Regulation §25.2512-1.

The rules governing what qualifies for a step-up, how a GRAT interacts with the gift tax, what happens when business interests are the funded asset, and what documentation the IRS expects are not self-evident from the statute. A GRAT funded with an improperly valued asset exposes the grantor to gift tax, IRS audit, and the potential for the entire strategy to fail.

Key Takeaways

- Zero-Out Gift Strategy: A “zeroed-out” GRAT is structured so the present value of the annuity payments equals the transferred asset’s value, resulting in a taxable gift close to zero at funding while still transferring post-hurdle appreciation to heirs.

- Section 7520 Hurdle Rate: All appreciation above the monthly IRS Section 7520 rate (3.8% as of April 2026) passes to remainder beneficiaries free of additional gift tax, making GRATs most effective when rates are low and assets are expected to appreciate significantly.

- Business Valuation Is Critical: The gift tax value of assets transferred into a GRAT is set by the initial appraisal; an overstated value reduces the strategy’s efficiency, while an understated value creates gift tax liability and potential IRS penalties.

- Term Risk: If the grantor dies during the GRAT term, the trust assets are pulled back into the gross estate, negating the transfer tax benefit, which is why shorter GRAT terms are often preferred to reduce mortality risk.

- Rolling GRAT Strategy: Business owners frequently use a series of short-term (two-year) GRATs, recycling annuity payments into new GRATs, to reduce term risk while accumulating successive rounds of tax-free appreciation transfer.

Each of these mechanics interacts with the structure and timing of the business owner’s estate plan. The sections below explain each in detail so owners and their advisors understand how GRATs work, when to use them, and what documentation is required.

What Is a GRAT and How Does It Work?

A Grantor Retained Annuity Trust is an estate freeze strategy authorized under IRC §2702. The grantor transfers an asset to an irrevocable trust and retains an annuity stream for a fixed term. The annuity is calculated so that its present value, discounted at the Section 7520 rate, equals the full fair market value of the assets transferred. Because the retained annuity is deemed to equal the gift, the taxable gift at funding approaches zero.

If the asset grows faster than the Section 7520 rate during the trust term, that excess appreciation is captured by the trust and passes to remainder beneficiaries at term end without incurring additional gift tax. The grantor remains the income tax owner of the trust during the term, meaning the trust’s income and gain are reported on the grantor’s return, further enhancing wealth transfer by allowing the trust to grow without being reduced by income taxes paid by the trust itself.

| Feature | GRAT | Outright Gift | Irrevocable Life Insurance Trust |

|---|---|---|---|

| Gift tax on transfer | Near zero (if zeroed out) | Full FMV at transfer | Premiums (annual exclusion eligible) |

| Estate inclusion if grantor dies | Trust assets pulled back | None | None |

| Income tax during term | Grantor pays | Donee pays | Trust/beneficiary pays |

| Appreciation transfer | Excess above 7520 rate | All future appreciation | Death benefit |

| IRS audit risk | Moderate (valuation-driven) | Low | Low |

What Assets Work Best in a GRAT?

GRATs perform best when funded with assets expected to appreciate significantly above the Section 7520 rate. Closely held business interests are among the most common GRAT assets because they can be legitimately valued at a discount at funding using minority interest and lack of marketability adjustments, then appreciated (or be sold) at a higher value during the trust term. Pre-IPO shares, carried interest in private equity funds, and real estate interests with near-term development potential are also common candidates.

Cash and low-yield publicly traded bonds are poor GRAT candidates because their expected return may not exceed the Section 7520 hurdle rate. For business owners, funding a GRAT with an operating company interest shortly before a planned sale or recapitalization can produce a substantial tax-free transfer if the transaction value significantly exceeds the appraised funding value.

According to the American College of Trust and Estate Counsel (ACTEC) Foundation (2023), GRATs funded with closely held business interests accounted for the largest median transfer values in estate freeze strategies, with the median successfully transferred amount exceeding $4 million in transactions where the Section 7520 rate was below 2%. Practitioners including Kroll‘s estate tax advisory group and Stout’s gift and estate tax valuation practice report that the most effective GRAT funding assets share three characteristics: strong projected appreciation, a supportable minority interest discount at funding, and adequate liquidity or cash flow to sustain annuity payments without liquidating the contributed interest.

The key characteristics of assets suited to GRAT funding include:

- Significant projected appreciation: The asset must be expected to outperform the Section 7520 rate to generate any transfer benefit.

- Supportable minority interest discount: For business interests, a qualified appraiser can apply discounts for lack of control and lack of marketability, reducing the taxable gift value at funding.

- Pre-transaction potential: An operating company interest contributed before a recapitalization or sale often generates the highest excess appreciation relative to the funding appraisal.

- Annuity payment sustainability: The grantor’s other assets or the contributed asset itself must support annuity payments without requiring liquidation of the trust asset.

These characteristics should be evaluated by a qualified appraiser and estate planning attorney before selecting a GRAT as the transfer vehicle.

How Is a Business Interest Valued for GRAT Funding?

The IRS requires that assets transferred to a GRAT be reported at fair market value on the gift tax return filed for the funding year. For closely held business interests, this means a qualified appraisal meeting the standards of Treasury Regulation §25.2512-1 and IRS Notice 2006-96. The appraisal must establish the price at which the interest would change hands between a willing buyer and a willing seller, neither under compulsion, with full knowledge of the relevant facts.

For minority interests, a qualified appraiser will typically apply a discount for lack of control and a discount for lack of marketability, reducing the taxable gift value at funding and improving the strategy’s efficiency. According to the American Society of Appraisers (ASA) (2024), business interest discounts for lack of control in closely held entities typically range from 15% to 35%, and discounts for lack of marketability range from 20% to 45%, depending on the entity’s operating characteristics, distribution history, and redemption provisions. Because the IRS scrutinizes GRAT funding valuations, the appraisal must be defensible under audit and supported by income approach, market approach, and asset approach analysis as appropriate for the business’s industry and financial profile.

What Happens If the Grantor Dies During the GRAT Term?

Mortality risk is the primary structural risk in a GRAT. If the grantor dies before the trust term expires, IRC §2036 causes the trust assets to be included in the grantor’s gross estate for federal estate tax purposes, effectively unwinding the transfer. The strategy produces no estate tax benefit in that scenario, though it also produces no net harm beyond the administrative cost of the trust.

To manage mortality risk, practitioners typically use short GRAT terms, with two-year rolling GRATs being most common, because a two-year term reduces the probability that the grantor will die before the annuity period ends. Some practitioners pair a GRAT with a second-to-die or survivorship life insurance policy held in an irrevocable life insurance trust to provide liquidity if the GRAT fails due to grantor death. For business owners in good health, short-term rolling GRATs provide the most efficient balance between mortality risk and repeated opportunities to capture appreciation.

Ready to fund a GRAT with a closely held business interest? Sofer Advisors provides IRS-compliant business valuations specifically structured for GRAT funding, gift tax reporting, and estate planning documentation. Contact us to request a GRAT funding appraisal.

How Should Business Owners Use a Rolling GRAT Strategy?

A rolling GRAT strategy involves establishing a series of two-year GRATs in sequence, with each annuity payment received from the prior GRAT immediately transferred into a new GRAT. This approach allows the grantor to capture year-over-year appreciation on a rolling basis while limiting exposure to term risk. If any single GRAT fails because the asset underperforms the Section 7520 rate, the grantor simply receives back the annuity payments and the trust winds down with no gift tax cost and no penalty.

According to the Journal of Financial Planning (2023), rolling two-year GRATs funded annually produce a statistically higher probability of successful wealth transfer than single longer-term GRATs in low-interest-rate environments, primarily because each two-year window independently captures any above-hurdle appreciation regardless of underperformance in adjacent years. The key operational requirements for a rolling GRAT program include:

- Annual qualified appraisal: Each time a closely held business interest is contributed to a new GRAT, a fresh appraisal is required to establish the updated fair market value for gift tax reporting purposes.

- Timely Form 709 filing: A gift tax return must be filed for each funding event, even when the taxable gift is zero, to start the IRS statute of limitations on the valuation.

- Precise annuity payment schedule: Payments must be made on the exact schedule required by the trust document to avoid inadvertent modifications that could jeopardize the GRAT’s tax treatment.

- Reinvestment discipline: Annuity payments received from expiring GRATs must be promptly contributed to new GRATs to maintain the rolling strategy’s compounding effect.

These requirements make a rolling GRAT program an operational undertaking that requires coordination between the estate planning attorney, the CPA, and the business appraiser throughout the program’s life.

What Are the Gift Tax Reporting Requirements for a GRAT?

The grantor must file a federal gift tax return (Form 709) in the year the GRAT is funded, even if the taxable gift is zero. The return must disclose the assets transferred, the fair market value at the date of funding, the annuity retained, and the calculation of the taxable gift. A qualified appraisal must be attached to the return if the contributed asset is a closely held business interest, real estate, or other non-publicly traded property.

The IRS has authority to audit the GRAT funding valuation for three years from the date the return is filed, or six years if the value is understated by more than 25%. Filing a complete and defensible Form 709 with a qualified appraisal starts the statute of limitations and protects the grantor from indefinite IRS exposure on the funding valuation. Sofer Advisors provides appraisals prepared to the standards required for Form 709 attachment, including full compliance with IRS Notice 2006-96 and the Uniform Standards of Professional Appraisal Practice (USPAP).

Frequently Asked Questions

What does GRAT stand for?

GRAT stands for Grantor Retained Annuity Trust. It is an irrevocable trust under IRC §2702 in which the grantor transfers assets and retains the right to receive annual annuity payments for a fixed term. If the assets appreciate above the Section 7520 hurdle rate, the excess passes to remainder beneficiaries, typically heirs, with little or no gift tax.

How is the taxable gift calculated in a GRAT?

The taxable gift equals the fair market value of the assets transferred minus the present value of the annuity the grantor retains, discounted at the IRS Section 7520 rate for the month of funding. In a zeroed-out GRAT, the annuity is set so the present value of the retained payments equals the full funding value, producing a taxable gift of approximately zero.

Can a GRAT be funded with a minority interest in a closely held business?

Yes, and this is one of the strategy’s most powerful applications. A minority interest in a closely held business can be valued with discounts for lack of control and lack of marketability, reducing the amount treated as a taxable gift at funding. If the business then sells or appreciates significantly, the excess value above the Section 7520 rate passes to heirs free of gift tax, creating a highly leveraged transfer.

What is the Section 7520 rate and why does it matter?

The Section 7520 rate is the IRS hurdle rate used to calculate the present value of the grantor’s retained annuity. It is published monthly and equals 120% of the applicable federal midterm rate. A lower Section 7520 rate means smaller annuity payments are needed to zero out the gift, while a higher rate makes it harder for assets to outperform the hurdle. GRATs are most efficient when the 7520 rate is low.

What happens if the GRAT assets underperform the 7520 rate?

If the assets grow slower than the Section 7520 rate, the annuity payments will exhaust the trust assets before the term ends, and nothing passes to the remainder beneficiaries. The grantor receives back the asset value through annuity payments with no gift tax cost and no penalty. The strategy produces no benefit but also no harm beyond administrative cost.

Does the grantor pay income tax on GRAT earnings?

Yes. A GRAT is a grantor trust for income tax purposes during the trust term, meaning the grantor, not the trust or its beneficiaries, reports all income, gains, and deductions on their personal income tax return. This is beneficial because the grantor’s payment of income taxes on GRAT assets effectively constitutes an additional tax-free gift to the trust, allowing the trust’s assets to grow without being reduced by taxes paid by the trust itself.

Is a GRAT appropriate for all business owners?

GRATs are most appropriate for business owners with significant closely held business interests, who are in good health (to reduce mortality risk), who expect the business to appreciate substantially above the Section 7520 rate, and who have completed basic estate planning. Business owners in poor health, with businesses with uncertain growth trajectories, or who have already exhausted their lifetime exemption may find other strategies, such as an installment sale to an intentionally defective grantor trust, more suitable.

How does a GRAT differ from a family limited partnership?

A family limited partnership transfers business interests to family members by shifting ownership through partnership units, typically claiming valuation discounts at the partnership level. A GRAT transfers the economic benefit of asset appreciation to remainder beneficiaries through an annuity mechanism, with the grantor retaining the annuity stream rather than ongoing partnership income. Both strategies rely on qualified business appraisals, but the legal structure, transfer mechanics, and IRS audit patterns differ materially.

How much does a GRAT funding appraisal from Sofer Advisors cost?

A GRAT funding appraisal from Sofer Advisors typically ranges from $7,500 to $25,000 depending on the complexity of the business interest, the applicable minority interest discounts, and the documentation required for Form 709 gift tax reporting. Engagements are generally completed in four to eight weeks from document receipt. For a fee estimate based on your specific estate planning facts, contact Sofer Advisors.

Related Case Studies

- Estate Tax Valuation: Defensible Appraisal for Executor Planning

- Valuation Timing: Why the Right Date Changes Everything

- Closely Held Business Valuation for Estate Planning and Gift Tax

Executive Summary

A Grantor Retained Annuity Trust allows business owners to transfer the future appreciation of a closely held business interest to heirs with minimal or zero gift tax cost by retaining an annuity stream during a fixed trust term. The strategy works when the business grows faster than the IRS Section 7520 hurdle rate, with excess appreciation passing to remainder beneficiaries free of additional gift tax. Key risks include grantor mortality during the trust term, which causes estate inclusion, and underperformance below the 7520 rate, which returns assets to the grantor with no benefit but no penalty. Short-term rolling GRATs reduce mortality risk while accumulating tax-free transfers over successive rounds. The strategy requires a qualified business appraisal at funding and Form 709 gift tax reporting, and business owners should work with an estate planning attorney and a qualified appraiser to implement it correctly.

What Should You Do Next?

Sofer Advisors provides IRS-compliant appraisals structured specifically for GRAT funding, gift tax reporting, and estate planning purposes. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals have delivered qualified business appraisals for GRAT funding transactions across professional services, real estate holding companies, and manufacturing businesses. Schedule a free consultation to discuss the valuation documentation your estate plan requires.

People Also Read

- Valuation of Closely Held Business for Estate Tax Purposes

- Fair Market Value for Estate Tax: What Executors Need

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}