Last Updated: April 2026

A phantom stock plan is a deferred compensation arrangement in which a company grants key employees units that track the value of the company’s stock or the appreciation in that value over a defined period, paying out in cash rather than actual equity at vesting, termination, or a triggering event such as a sale of the business. Unlike stock options, restricted stock units, or employee stock ownership plans (ESOPs), phantom stock transfers no actual ownership interest to the employee, produces no dilution of existing shareholders, and requires no securities compliance under federal or state law. The company receives a tax deduction at the same time the employee recognizes income, and the employee receives a cash payout calculated by reference to the business’s fair market value.

For middle-market business owners who want to incentivize and retain key employees without diluting ownership, transferring equity to non-family members, or navigating the regulatory complexity of an ESOP or securities offering, phantom stock plans represent a practical alternative that aligns employee financial interests with business value creation. Sofer Advisors, a credentialed business valuation firm based in Atlanta, GA, provides the independent fair market value appraisals required to set phantom stock unit values, calculate payout amounts, and satisfy IRC 409A safe harbor requirements, with ABV and ASA oversight on every engagement.

Whether phantom stock is appropriate for your business depends on your retention goals, ownership structure, tax situation, and the financial profile of the key employees you are trying to incentivize. The Key Takeaways below summarize the core features of phantom stock plans before the detailed sections that follow.

Key Takeaways

- Phantom Stock Pays Cash, Not Shares: Employees receive a cash payment calculated by reference to the business’s share value or value appreciation at vesting or a triggering event. No actual equity is transferred and existing shareholders experience no dilution.

- Two Structures Exist: Full-value phantom stock mirrors the payout of a restricted stock unit, paying the entire per-unit fair market value at settlement. Appreciation-only phantom stock functions like a stock appreciation right (SAR), paying only the increase in value above the grant-date baseline.

- IRC 409A Compliance Is Required: Phantom stock plans are nonqualified deferred compensation arrangements subject to Internal Revenue Code Section 409A. Non-compliant plans trigger immediate income recognition for the employee plus a 20% excise tax on the deferred amount.

- Valuation Drives the Payout: The cash amount an employee receives is calculated by multiplying the number of phantom units by the business’s fair market value per unit at the settlement date. An independent appraisal or 409A safe harbor valuation establishes that value.

- Phantom Stock Is Not Appropriate for Every Business: It is most effective for profitable businesses with predictable value growth and a clear liquidity horizon. Businesses with irregular earnings, no succession plan, or no defined triggering event structure may find phantom stock difficult to administer and fund.

Each of these features determines whether a phantom stock plan fits the business’s retention goals and what operational and valuation infrastructure the plan requires to function correctly. The sections below examine how phantom stock works, what tax rules apply, how it is valued, how it compares to alternative structures, and when it makes sense to use one.

What Is a Phantom Stock Plan?

A phantom stock plan is a contractual arrangement between a company and a key employee in which the employee earns units of notional equity that increase in value as the business grows, with the accumulated value paid out in cash at a defined triggering event, typically separation from service, retirement, death, disability, or a sale of the business. The plan is created by a written agreement that specifies the number of units granted, the vesting schedule, the triggering events that cause a payout, the valuation methodology used to calculate payout value, and the distribution timing required to comply with IRC 409A.

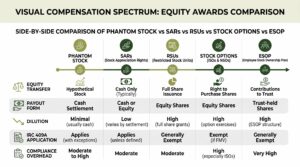

| Feature | Phantom Stock (Full Value) | Phantom Stock (Appreciation Only) | RSU | Stock Option | ESOP |

|---|---|---|---|---|---|

| Equity Transferred? | No | No | Yes (shares) | Yes (right to buy) | Yes (plan trust) |

| Payout Form | Cash | Cash | Shares or cash | Shares at exercise | Shares or cash at distribution |

| Dilution to Owners | None | None | Yes | Yes | Yes |

| IRC 409A Applies? | Yes | Yes | Depends on structure | Generally no | No |

| Independent Valuation Required? | Yes (FMV at payout) | Yes (FMV at grant and payout) | Yes | Yes | Yes (annual ESOP appraisal) |

| Securities Compliance | None | None | May apply | May apply | Yes (DOL and ERISA) |

Phantom stock is particularly common in S corporations, professional service firms, and family businesses where transferring actual ownership interests would create operational, legal, or family dynamics complications. Because no stock is actually issued, phantom stock plans require no shareholder agreement amendments, no securities registration, and no formal equity capitalization table update, which simplifies administration compared to actual equity plans.

How Does Phantom Stock Work?

Phantom stock works through a written grant agreement that establishes the baseline value per unit at the time of the grant, the vesting schedule over which the employee earns the right to a payout, and the triggering event that causes the cash distribution to occur. A full-value phantom stock plan sets the baseline at zero, entitling the employee to the full per-unit fair market value at payout. An appreciation-only plan sets the baseline at the per-unit fair market value at the time of the grant, entitling the employee only to the increase above that baseline, mirroring the economic exposure of a stock appreciation right without issuing actual equity.

Vesting schedules for phantom stock typically range from three to five years, with either cliff vesting (100% at a fixed date) or graded vesting (equal tranches earned annually over the vesting period). At the triggering event, the company calculates the payout by multiplying the number of vested units by the current per-unit fair market value, less the baseline for appreciation-only plans, and distributes the cash to the employee. The company must have liquidity sufficient to fund the payout, which is why phantom stock is most practical for businesses with reliable cash flow or a defined liquidity event such as a sale where the payout is funded from transaction proceeds.

What Are the Tax Implications of Phantom Stock?

Phantom stock payouts are taxed as ordinary compensation income to the employee in the year of distribution, not as capital gains, regardless of how long the employee held the units. The employer withholds federal and state income tax and Federal Insurance Contributions Act (FICA) taxes at the time of payout. The company receives a corresponding tax deduction in the year of distribution, which partially offsets the cash cost of the payout. Because phantom stock generates ordinary income rather than capital gains, it is less tax-efficient for the employee than incentive stock options or direct equity that qualifies for long-term capital gains treatment upon sale.

The primary compliance requirement is IRC 409A, which governs all nonqualified deferred compensation arrangements, including phantom stock plans. According to the Internal Revenue Service (IRS) (2024), deferred compensation subject to IRC 409A must be distributed only upon one of six permissible triggering events: separation from service, disability, death, a change in control, an unforeseeable emergency, or a fixed payment date elected before the compensation is deferred. Plans that fail to comply with 409A result in immediate income inclusion for the employee on all deferred amounts, plus a 20% excise tax on the deferred amount, plus interest on underpayments from the original deferral date.

A 409A valuation vs fair market value analysis is often required when a company establishes a phantom stock plan to confirm that unit values are set at arm’s-length fair market value, particularly for appreciation-only plans where an artificially low grant-date baseline would overstate the ultimate payout and create additional IRC 409A exposure.

How Is Phantom Stock Valued?

Phantom stock units are valued by reference to the fair market value of the business at each relevant date: the grant date for appreciation-only plans and the triggering event date for all plans. The business must have a supportable, defensible fair market value conclusion at each of these dates to calculate payout amounts accurately and to protect the company against IRS challenge to the compensation deduction. According to the American Institute of Certified Public Accountants (AICPA) (2023), a qualified independent appraisal using a 409A safe harbor methodology provides presumptive protection against IRS challenges to the fair market value used in nonqualified deferred compensation arrangements, with that presumption rebuttable only if the IRS demonstrates the valuation was grossly unreasonable given the information available at the time.

Phantom stock plans typically require an independent fair market value appraisal at the following points:

- At plan establishment: To set the baseline per-unit value, particularly for appreciation-only plans where the grant-date conclusion determines what appreciation the employee will ultimately receive.

- At each new grant date: When units are granted to new or existing participants, the company must document the per-unit fair market value for IRC 409A compliance and compensation records.

- At each triggering event: When an employee separates, retires, dies, becomes disabled, or when the company is sold, the payout is calculated using the fair market value at the triggering event date.

- At plan termination: When a plan is terminated under an IRC 409A permissible termination scenario, the fair market value at termination establishes final distribution amounts.

Schedule your free consultation with Sofer Advisors to receive an independent fair market value appraisal for your phantom stock plan that satisfies IRC 409A safe harbor requirements and supports payout calculations that will withstand IRS review. Discover The Sofer Difference.

How Does Phantom Stock Compare to Other Plans?

Phantom stock occupies a specific position in the equity compensation spectrum, offering employee incentives tied to business value without the ownership transfer, securities compliance, or regulatory overhead of formal equity plans. Compared to an ESOP transaction, which establishes a formal trust that acquires actual shares and is governed by Department of Labor and Employee Retirement Income Security Act (ERISA) regulations, a phantom stock plan requires no formal trust, no ERISA compliance, no DOL reporting, and no annual compliance filing, making it substantially simpler and less expensive to establish and maintain annually.

According to the National Center for Employee Ownership (NCEO) (2024), phantom stock and stock appreciation rights are among the most widely adopted equity-like compensation structures at privately held companies, chosen by owners who want to create meaningful financial incentives for key employees tied to business value creation without the complexity and cost of formal equity plans or the dilution that accompanies actual ownership transfers. Compensation advisory firms including RSM US and resources published by the NCEO provide general guidance on phantom stock design; Sofer Advisors provides the independent valuation component that establishes the defensible fair market value on which every payout calculation depends.

Compared to stock options, phantom stock requires no employee purchase at exercise and no securities compliance, but generates ordinary income rather than the potential capital gains treatment available under incentive stock options. Compared to restricted stock units, phantom stock generates no ownership interest at settlement, which avoids the need to add the employee as a shareholder, amend shareholder agreements, or manage an ongoing equity relationship with the recipient.

When Should a Business Use Phantom Stock?

A phantom stock plan is most appropriate when the business wants to incentivize and retain a small number of key employees, the owners are not ready to transfer actual equity or pursue an ESOP, the business has a clear triggering event horizon such as a planned sale in three to seven years, and the business has the cash flow or defined liquidity event to fund the payouts when triggered. Phantom stock is less appropriate for businesses with unpredictable earnings, no defined exit horizon, or a large number of intended recipients, because administering periodic valuations and maintaining cash reserves for multiple simultaneous payout obligations adds operational complexity that can outweigh the retention benefit.

Circumstances where phantom stock is commonly used include:

- Key employee retention before a business sale: Owners planning to sell within three to five years grant phantom units that vest and pay out at close, aligning the key employee’s financial interest with maximizing transaction value and completing the sale successfully.

- Succession plan bridge compensation: When a successor manager is identified but full equity transfer is premature, phantom stock provides economic alignment without the legal and relationship complications of partial ownership.

- Professional service firm leadership incentives: Law firms, accounting firms, and medical practices use phantom stock to retain senior non-equity professionals without the regulatory complexity of formal partnership admission.

- S corporation shareholder limitation avoidance: S corporations are limited to 100 eligible shareholders, so phantom stock avoids S-election risk while providing equivalent financial incentives to key employees.

- Family business non-family executive retention: When owners intend to pass the business to family heirs, phantom stock rewards key non-family executives without creating external shareholders who complicate the succession or dilute family control.

In each of these scenarios, the critical enabler is a current, documented fair market value conclusion on which the plan’s grant-date unit values and ultimate payout calculations can be reliably based.

Frequently Asked Questions

What is a phantom stock plan?

A phantom stock plan is a deferred compensation arrangement in which a company grants key employees notional units that track business value or value appreciation, with the accumulated value paid in cash at vesting, separation from service, or a triggering event such as a business sale. No actual equity is issued, shareholders experience no dilution, and the plan requires no securities registration. Phantom stock plans are subject to IRC 409A deferred compensation rules and must be structured carefully to avoid immediate income inclusion and the 20% excise tax penalty.

How does phantom stock differ from actual stock?

Actual stock represents a legal ownership interest with voting rights, a pro-rata claim on company assets, and equity participation at liquidation. Phantom stock represents a contractual right to receive cash calculated by reference to stock value, with no ownership interest, no voting rights, and no claim on company assets. Phantom stock is simpler to administer than actual equity because it requires no shareholder agreement amendment, no securities filing, no capitalization table update, and no ongoing equity relationship with the recipient employee after the payout is made.

Is phantom stock subject to IRC 409A?

Yes. Phantom stock plans are nonqualified deferred compensation arrangements fully subject to Internal Revenue Code Section 409A. The plan must specify permissible distribution events in advance, must not allow employee-directed acceleration of distributions, and must comply with the six allowable triggering events under the code: separation from service, disability, death, a change in control, an unforeseeable emergency, or a fixed payment schedule. Plans that fail 409A requirements expose the employee to immediate income inclusion plus a 20% excise tax on all deferred amounts plus interest from the original deferral date.

What triggers a phantom stock payout?

Phantom stock payouts are triggered by events defined in the plan document and must align with IRC 409A permissible distribution events. Common triggering events include separation from service, death or disability, a change in control or sale of the business, or a fixed payment date established in advance. Most middle-market phantom stock plans are designed to pay out at a business sale, which creates the liquidity to fund the payout and aligns the employee’s financial incentive with completing a successful transaction at the highest achievable price.

How is the payout amount calculated?

The payout is calculated by multiplying the number of vested phantom units by the per-unit fair market value of the business at the triggering event date, less the grant-date baseline for appreciation-only plans. The per-unit value is derived from an independent business appraisal or a formula defined in the plan document, such as a fixed multiple applied to the most recent twelve months of normalized earnings before interest, taxes, depreciation, and amortization (EBITDA). Plans using a formula-based value must ensure the formula produces a reasonable approximation of fair market value to avoid IRC 409A and income tax challenges.

What are the tax consequences for the employee?

Phantom stock payouts are taxed as ordinary compensation income in the year of distribution, subject to federal income tax, state income tax, Social Security tax up to the annual wage base, and Medicare tax including the additional 0.9% Medicare surtax for high-income employees. The payout is not eligible for long-term capital gains rates even if the employee held the units for more than one year. The employer withholds applicable taxes at the time of distribution and issues a W-2 reflecting the compensation income in the year paid.

What are the tax consequences for the company?

The company receives a tax deduction for the phantom stock payout in the same year the employee recognizes the income, assuming the plan complies with IRC 409A and the deduction timing rules under IRC 404. For C corporations, the deduction reduces taxable income at the corporate rate. For S corporations, the deduction flows through to the individual owners on their Schedule K-1s. The company must model the after-tax cost of the phantom stock liability as part of evaluating whether the plan is economically viable given current earnings, cash reserves, and anticipated payout timing.

How much does a phantom stock valuation cost?

An independent business appraisal to set phantom stock unit values and satisfy IRC 409A safe harbor requirements from Sofer Advisors typically ranges from $2,500 to $9,000 depending on the company’s revenue, industry, capital structure complexity, and whether the engagement requires a grant-date valuation, a triggering-event payout valuation, or both. Most 409A-compliant appraisals for phantom stock purposes are completed within two to four weeks of document receipt. For a fee estimate based on your specific situation, contact Sofer Advisors.

Can a phantom stock plan be terminated early?

Yes, with restrictions. IRC 409A permits plan termination in three specific circumstances: a change in control event with payout within twelve months of termination, a corporate dissolution approved by a bankruptcy court, or a discretionary termination where no new nonqualified deferred compensation plans are established within three years and distributions occur between thirteen and twenty-four months after the termination election. Outside these approved circumstances, accelerating distributions upon plan termination violates IRC 409A and triggers the 20% excise tax, so plan termination strategy requires qualified legal and tax guidance.

How does phantom stock compare to an ESOP?

An ESOP establishes a formal trust that acquires actual company shares, provides employees with ownership interests governed by ERISA and Department of Labor regulations, and requires annual valuations by an ERISA-qualified independent appraiser. Phantom stock requires no trust, no ERISA compliance, no DOL reporting, and no formal securities structure, making it faster to implement and less expensive to maintain. However, an ESOP provides significant tax advantages for selling shareholders of C corporations under IRC 1042, allowing capital gains deferral on proceeds reinvested in qualified replacement property, which phantom stock does not replicate.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

A phantom stock plan is a deferred compensation arrangement that provides key employees with cash payouts calculated by reference to business fair market value, without transferring actual equity or diluting existing ownership. The plan must comply with IRC 409A, which governs permissible distribution events, acceleration restrictions, and distribution timing. Payouts are taxed as ordinary income to the employee, with a corresponding deduction for the company in the year of distribution. The payout amount is driven by the business’s fair market value at the triggering event date, making an independent appraisal or 409A safe harbor valuation a required component of any well-structured phantom stock program. Sofer Advisors provides credentialed business appraisals for phantom stock plan establishment, grant-date documentation, and triggering-event payout calculations with ABV and ASA oversight on every engagement.

What Should You Do Next?

If you are evaluating a phantom stock plan for your business, the first step is confirming that the business has a supportable fair market value conclusion on which to base both the grant-date unit values and the ultimate payout calculation at the triggering event. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals for phantom stock plan documentation, IRC 409A safe harbor compliance, and triggering-event payout support for middle-market businesses across all industries. Schedule your free consultation to receive a credentialed appraisal that establishes defensible unit values for your plan and protects against IRS challenge.

People Also Read

- 409A Valuation vs Fair Market Value: Key Differences Explained

- ESOP Transaction Process Steps: Complete Guide for Business Owners

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}