Last Updated: April 2026

An earnout is a contractual provision in a business acquisition that ties a portion of the purchase price to the future financial performance of the business being sold. Rather than paying the full agreed purchase price at closing, the buyer makes an upfront payment and commits to additional payments contingent on the business meeting specified revenue, EBITDA, or other operational targets during a defined post-closing period, typically one to three years. Earnouts are most common in transactions where buyer and seller disagree on the business’s current value, where the business depends heavily on the seller’s continued involvement, or where recent financial results do not yet fully reflect the company’s earning potential.

For business owners entering sale negotiations, an earnout can either bridge a valuation gap or introduce years of post-sale financial uncertainty depending entirely on how it is structured. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides independent business appraisals that establish the defensible baseline EBITDA and fair market value needed to set realistic earnout targets, satisfy ASC 805 contingent consideration requirements, and protect sellers from structurally disadvantaged payout terms in middle-market transactions nationwide.

Whether an earnout closes a deal or creates post-close litigation depends almost entirely on how the performance metrics, measurement rules, and payout schedule are negotiated before the letter of intent is signed. The Key Takeaways below summarize the essential mechanics every seller should understand before accepting an earnout provision.

Key Takeaways

- Earnouts Bridge Valuation Gaps: When buyer and seller cannot agree on current value, an earnout defers a portion of the price to future performance, allowing the deal to close at a lower upfront payment with additional consideration contingent on results the seller believes the business will achieve.

- Earnout Periods Typically Run 1 to 3 Years: Most earnout provisions span one to three years post-close, with milestones measured quarterly or annually; longer periods increase dispute risk and reduce the present value of contingent payments received by the seller.

- Metric Selection Determines Earnout Safety: Revenue-based earnouts expose sellers to buyer cost decisions that suppress EBITDA; EBITDA-based earnouts expose sellers to accounting adjustments the buyer controls; negotiated metric definitions and accounting guardrails protect the seller from outcome manipulation.

- Earnout Payments Are Contingent Consideration Under ASC 805: For financial reporting, the buyer must record earnout obligations at fair value on the acquisition date and remember them each quarter, creating accounting volatility that makes credentialed fair value support important for both parties.

- Valuation Anchors Both Negotiation and Measurement: An independent business appraisal establishes the pre-close performance baseline from which earnout targets are set and provides the documented fair market value required for ASC 805 contingent consideration accounting.

Each of these mechanics creates negotiating leverage or financial exposure depending on which side of the table you sit on. The sections below examine how earnouts are structured, why they are used, what risks sellers face, how they are valued, and where business valuation enters both the negotiation and the post-close measurement process.

What Is an Earnout and How Does It Work?

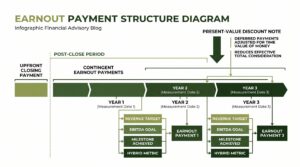

An earnout divides the total acquisition price into two components: a fixed amount paid at closing and a contingent amount paid only if the business achieves defined performance thresholds after closing. The contingent payment is calculated as a percentage of revenues above a floor, a multiple of EBITDA within a defined range, a flat payment triggered by a binary milestone such as a product launch or regulatory approval, or a sliding scale tied to a range of outcomes. At the end of each measurement period, typically a fiscal quarter or year, the buyer calculates actual results against the agreed targets and disburses the earnout payment if the threshold is met.

| Feature | Earnout Structure | Full Cash at Close |

|---|---|---|

| Upfront payment | Lower than full value | Full agreed purchase price |

| Seller’s post-close involvement | Often required or incentivized | Optional; seller exits fully |

| Buyer’s risk | Lower; contingent on future performance | Higher; buyer pays regardless of results |

| Seller’s risk | Higher; contingent payments may not materialize | Lower; all cash received at close |

| Valuation gap resolution | Yes, defers disputed value to actual results | No; both parties must agree on value at close |

| Common trigger types | Revenue, EBITDA, milestones, customer retention | N/A |

| Typical earnout period | 1 to 3 years post-close | None |

| Accounting treatment (buyer) | Contingent consideration at fair value under ASC 805 | No contingent liability recorded |

Earnout mechanics are governed by the purchase agreement, which specifies the measurement methodology, the accounting standards applied to determine what counts as revenue or EBITDA, and the dispute resolution process if buyer and seller reach different conclusions on what was achieved during a measurement period.

How Are Earnout Payments Structured?

Earnout structures vary by industry, deal size, and the specific source of the valuation disagreement between buyer and seller. In service businesses with strong recurring revenue, earnouts are commonly tied to revenue retention, measuring whether the seller’s existing client base continues generating contracted revenue during the earnout period. In manufacturing or distribution businesses, earnouts are commonly tied to EBITDA margins, measuring whether the business achieves the operating performance the seller projected. In early-stage or growth companies, earnouts are commonly tied to binary milestones such as achieving a specified contracted customer count, completing a regulatory submission, or closing a named strategic partnership.

Common earnout performance metrics negotiated in middle-market transactions:

- Revenue-based: Total recognized revenue compared to a defined threshold or tiered schedule; simplest to measure but susceptible to buyer cost decisions that shift profitability without affecting the top line.

- EBITDA-based: Earnings before interest, taxes, depreciation, and amortization compared to a target; more predictive of seller value but vulnerable to post-close accounting adjustments the buyer controls.

- Gross profit-based: Revenue minus cost of goods sold compared to a target; excludes the buyer’s overhead and SG&A decisions from the measurement, providing a middle ground between revenue and EBITDA.

- Milestone-based: Binary triggers such as regulatory approvals, product launches, or contract signings; common in life sciences, technology, and startup acquisitions where revenue has not yet materialized.

- Customer retention-based: Percentage of revenue from existing customers retained post-close; used in service businesses and software-as-a-service (SaaS) companies where client concentration is the primary value driver.

- Hybrid metrics: A combination of revenue and EBITDA thresholds with separate triggers and payment schedules; most protective for sellers but most complex to negotiate, administer, and audit.

The payout schedule, whether the earnout is paid as a lump sum at the end of the measurement period or in quarterly installments, materially affects the present value the seller actually receives after accounting for the time value of money and the probability of non-achievement.

Why Do Buyers and Sellers Use Earnouts?

Buyers use earnouts to manage acquisition risk when the target company’s projected performance is uncertain, when the seller’s continued involvement is essential to business continuity, or when the business has been growing rapidly and the buyer is skeptical that the growth rate is sustainable without the founder’s direct involvement. An earnout shifts the financial risk of optimistic seller projections back to the seller, aligning the seller’s financial incentive with the business’s post-close results. For buyers, this reduces capital deployed at risk on day one and creates contractual alignment with the person who knows the business best.

Sellers accept earnouts when their business has strong performance momentum not yet fully reflected in trailing financials, when they are confident the targets will be met and want the upside, or when accepting an earnout is the only path to closing a deal that cannot otherwise bridge a valuation disagreement. Sellers who have contracted backlog, signed customer agreements, or active pipeline that has not yet converted to recognized revenue are in the strongest position to accept earnout risk because they have independent evidence the targets will be achieved.

According to AICPA Forensic and Valuation Services (2023), earnouts are present in approximately 20% to 30% of middle-market M&A transactions and are most concentrated in industries with high growth rates, key person dependency, or significant intangible asset value that is difficult to independently verify at the time of sale.

What Are the Risks of an Earnout for Sellers?

The central risk of an earnout for sellers is loss of control over the business operations that determine whether the earnout is achieved. After closing, the buyer controls hiring, spending, pricing, customer strategy, and financial reporting, all of which directly affect the metrics the seller’s earnout payment depends on. A buyer who redirects resources, charges new overhead allocations, or changes revenue recognition policies can suppress reported EBITDA below the earnout threshold without violating the letter of the purchase agreement.

Seller risks in earnout agreements include:

- Metric manipulation: Buyer adjusts cost allocations, overhead charges, or depreciation schedules to suppress EBITDA below the earnout floor through accounting decisions rather than actual underperformance.

- Customer reassignment: Buyer reassigns key accounts to other business units, removing revenue from the earnout measurement entity without losing the relationship.

- Integration interference: Post-close integration decisions, system migrations, or brand changes disrupt customer relationships and suppress performance during the earnout measurement period.

- Accounting policy changes: Buyer changes revenue recognition timing or expense treatment in ways that reduce measured results below the contractual threshold.

- Definition disputes: Buyer and seller interpret the purchase agreement’s measurement definitions differently, requiring arbitration or litigation to resolve at significant legal cost.

- Present value erosion: Even when earnout payments are made in full, a three-year deferred contingent payment discounted at 15% to 20% to reflect risk of non-achievement is worth materially less than a cash-at-close equivalent on the same headline amount.

Schedule your free consultation with Sofer Advisors to understand how an independent appraisal establishes a defensible performance baseline before you negotiate earnout terms, and how valuation supports your position if a post-close dispute arises. Discover The Sofer Difference.

How Is an Earnout Valued?

Valuing an earnout requires estimating the probability that the contingent payment will be triggered, projecting the timing of when payments will be received, and discounting those probabilistic cash flows to present value as of the acquisition date. The most common methods applied in middle-market transactions are scenario-based analysis, which assigns probability weights to two or three performance outcomes (base, upside, and downside), calculates the probability-weighted expected payment at each outcome, and discounts the result at a rate reflecting the earnout’s specific risk; and option pricing models, which treat the earnout as a financial option on the business’s future performance with a defined strike price equal to the earnout threshold.

According to FASB ASC 805 (Business Combinations), the buyer must recognize earnout obligations as contingent consideration measured at fair value on the acquisition date. After closing, the buyer measures the earnout liability to fair value each reporting period, with changes flowing through the income statement rather than being treated as an adjustment to goodwill. This remeasurement requirement creates quarterly earnings volatility for the buyer that makes accurately established earnout fair values, supported by a qualified appraiser, important for both parties’ financial reporting and auditor sign-off.

How Does Business Valuation Support Earnouts?

In earnout transactions, business valuation serves three roles before, at, and after the close. Before closing, the independent appraisal establishes the baseline fair market value and normalized EBITDA from which earnout targets are calibrated. Without an independent baseline, sellers risk accepting targets set at levels the business cannot realistically achieve given its actual cost structure, customer concentration, and market position rather than the buyer’s optimistic assumptions. An earn-out valuation and M&A support engagement from Sofer Advisors documents the pre-close operating baseline so that both parties negotiate earnout thresholds from a shared, arm’s-length reference point.

At closing, the valuation provides the ASC 805 contingent consideration fair value required for the buyer’s purchase price allocation and the seller’s tax reporting. After closing, if an earnout dispute arises, a credentialed valuation professional provides expert analysis of whether the business should have achieved the earnout threshold given the operating decisions made by the buyer post-close. According to the American Society of Appraisers (ASA) (2024), earnout disputes are among the most common post-close M&A litigation matters, frequently requiring a valuation expert to establish whether underperformance was caused by market conditions, pre-close seller misrepresentation, or post-close buyer interference. Credentialed firms including Morgan and Westfield and BDO provide transaction advisory in larger earnout deals; for middle-market sellers, Sofer Advisors provides business valuation for mergers and acquisitions with direct ABV and ASA credentialed oversight on every engagement, ensuring the concluded value is documented and defensible at every stage of the earnout lifecycle.

Frequently Asked Questions

What is an earnout in a business sale?

An earnout is a contractual provision that ties a portion of the business sale price to the future performance of the business after closing. The seller receives a fixed upfront payment at close and additional payments only if the business meets defined revenue, EBITDA, or milestone targets during a specified post-closing period. Earnouts are used to bridge valuation disagreements between buyer and seller when both parties have different views of what the business is currently worth or will achieve.

How long does an earnout period typically last?

Most earnout provisions in middle-market transactions span one to three years post-close, with annual measurement periods being most common. Shorter earnout periods reduce dispute risk and are preferred by sellers because they preserve the present value of the contingent payment; longer periods are preferred by buyers who want more time to observe whether the seller’s performance projections were accurate. Earnout periods exceeding three years are uncommon and typically indicate significant uncertainty in projected results.

What is the most common earnout metric?

Revenue is the most commonly negotiated earnout metric in middle-market transactions because it is objectively measurable and less susceptible to buyer accounting adjustments than EBITDA. EBITDA-based earnouts are more common in transactions where operating margin is the primary driver of value, but they require careful contractual definitions to prevent the buyer from suppressing reported EBITDA through overhead allocations or policy changes. Milestone-based earnouts are most common in technology and life sciences acquisitions where the value-creating event is a defined future outcome rather than a run-rate financial result.

Can a seller negotiate the terms of an earnout?

Yes. Earnout terms are negotiable at the letter of intent stage and in the definitive purchase agreement. Sellers should negotiate the metric definition precisely, including which revenue is counted and which expenses are included in EBITDA; the accounting policies that will govern measurement; the seller’s operational autonomy during the earnout period; acceleration provisions that pay out the full earnout if the buyer sells the business or materially changes operations before the earnout period ends; and the dispute resolution mechanism, including the use of an independent valuation expert to resolve disagreements.

What happens if earnout targets are not met?

If the business does not meet the defined performance threshold during a measurement period, the earnout payment for that period is either reduced proportionally on a sliding scale or forfeited entirely, depending on how the earnout is structured. A floor payment, if negotiated, ensures the seller receives a minimum amount even if performance falls short. Sellers should always model the downside scenario before accepting an earnout: if the earnout represents a significant portion of the total purchase price and the targets are not met, the effective net proceeds at close may be materially below the headline deal value.

How does an earnout affect the seller’s taxes?

Earnout payments are generally recognized as income by the seller in the year they are received, not in the year of the closing. The tax character of each earnout payment, whether it is capital gain or ordinary income, depends on the nature of the underlying asset to which it is attributed. Earnout payments tied to goodwill or the equity sale are generally taxed as capital gain; payments tied to services, consulting obligations, or covenant-not-to-compete agreements are taxed as ordinary income. Sellers should engage a qualified tax advisor before signing any earnout agreement to model the expected after-tax proceeds under each performance scenario.

What is contingent consideration under ASC 805?

Contingent consideration under ASC 805 (Business Combinations) is the obligation a buyer recognizes when it commits to pay the seller additional amounts contingent on future events, such as an earnout. Under ASC 805, the buyer must record the earnout at its fair value on the acquisition date, based on the probability-weighted present value of expected future payments. After closing, the buyer remeasures the contingent consideration to fair value each reporting period, with changes recorded in the income statement rather than as goodwill adjustments, creating ongoing earnings volatility until the earnout period ends.

How can sellers protect themselves in an earnout agreement?

Sellers protect themselves by negotiating specific metric definitions in the purchase agreement that limit the buyer’s discretion to change accounting policies or overhead allocations post-close; by requiring the buyer to operate the business in the ordinary course during the earnout period without material changes that would affect earnout measurement; by including acceleration provisions that pay out the remaining earnout if the buyer sells the business or undergoes a change of control before the earnout period ends; and by specifying an independent accountant or valuation expert as the binding dispute resolution mechanism if buyer and seller reach different conclusions on measured results.

How much does an earnout valuation from Sofer Advisors cost?

A business appraisal and earnout baseline valuation from Sofer Advisors typically ranges from $7,500 to $25,000 depending on the company’s revenue, industry, and the complexity of the contingent consideration analysis required under ASC 805. Most standard earnout valuation engagements are completed in four to eight weeks from document receipt. For a fee estimate based on your specific transaction, contact Sofer Advisors.

When is an earnout a good deal for a seller?

An earnout is a favorable structure for a seller when the business has a strong contracted backlog, signed customer agreements, or identifiable pipeline that has not yet converted to recognized revenue, giving the seller confidence the targets will be met independently of the buyer’s post-close decisions. Sellers with key-person-independent businesses that can perform without the founder’s day-to-day involvement are also better positioned to accept earnout risk. An earnout is a poor structure for sellers who will lose operational control of the drivers that determine whether targets are met, or who need certainty of proceeds for personal financial planning, estate planning, or retirement.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

An earnout is a contingent payment provision in a business acquisition that ties part of the purchase price to the target’s future financial performance, typically measured over one to three years post-close. Buyers use earnouts to reduce acquisition risk when projected performance is uncertain; sellers accept them to close deals where historical financials understate future value or where a valuation disagreement cannot otherwise be bridged at the letter of intent stage. The earnout metric, whether revenue, EBITDA, gross profit, or a binary milestone, determines the seller’s exposure to post-close buyer decisions that can suppress measured performance below the threshold. Independent business valuation establishes the baseline performance from which earnout targets are set, satisfies ASC 805 contingent consideration fair value requirements, and provides expert analytical support if earnout disputes require arbitration. Sofer Advisors provides earnout baseline valuations, ASC 805 contingent consideration fair value analysis, and M&A transaction support for middle-market buyers and sellers across all industries.

What Should You Do Next?

If you are selling your business and an earnout is on the table, understanding the structure, the metrics, and the risks before you sign the letter of intent gives you the information needed to negotiate from a position of knowledge rather than urgency. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals, earnout baseline valuations, and ASC 805 contingent consideration fair value support for middle-market sellers navigating complex deal structures across all industries. Schedule your free consultation to understand your business’s value and how earnout mechanics will affect your after-tax proceeds.

People Also Read

- Earn-Out Valuation in M&A: Structuring and Fair Value

- Business Valuation for Mergers: Buy-Side vs Sell-Side

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}