Last Updated: June 2026

Earnouts are a tool buyers use to bridge a valuation gap and shift risk onto the seller. If the business hits defined targets after closing, the seller receives more consideration. In practice, most earnouts are written in ways that make them difficult for sellers to collect. A buyer who has operational control post-close also has the ability, intentionally or not, to make choices that reduce the metrics on which the earnout is measured. That is the core problem sellers must address before signing.

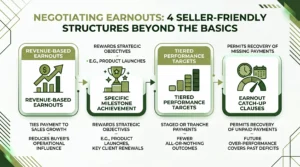

The four seller-friendly structures that matter most are: (1) revenue-based earnouts instead of EBITDA-based earnouts, (2) earnout accelerators that reward outperformance, (3) earnout floors that guarantee a minimum payment, and (4) independent accounting and binding arbitration clauses that remove measurement disputes from the buyer’s control. Together, these provisions shift the earnout from a buyer-favorable deferred payment into something closer to a genuine partnership in post-close performance. Sofer Advisors helps owners and their advisors work through exactly these questions and turn the analysis into a defensible business valuation they can act on.

The following takeaways summarize the key valuation and transaction factors covered in this guide.

Key Takeaways

- Revenuebased Earnouts Significantly Harder – Revenue-based earnouts are significantly harder for buyers to manipulate than EBITDA-based earnouts. Always push for revenue as the metric where possible.

- Earnout Accelerators Reward Outperformance – Earnout accelerators reward outperformance and ensure sellers benefit fully if the business grows faster than the deal model assumed.

- Earnout Floors Minimum Payment – Earnout floors – minimum payment guarantees – protect sellers from the single most common complaint: buyer operational decisions that suppress earnout metrics.

- Independent Accounting Review Binding – Independent accounting review and binding arbitration for disputes are non-negotiable provisions in well-drafted earnout agreements.

- Typical Earnout Duration 1 – Typical earnout duration is 1–3 years. Longer earnouts compound operational exposure and should require higher floors and better dispute resolution mechanisms.

- Valuing Earnout Closing Requires – Valuing an earnout at closing requires probability-weighting the scenarios under which it pays. Sellers who do not model this accept uncertainty they could quantify.

Each of these factors is examined in depth in the sections that follow.

What Is an Earnout and Why Do Buyers Love Them?

An earnout is a contingent payment mechanism in an M&A deal. The seller receives more consideration after closing if the acquired business meets defined financial or operational performance targets. The earnout amount, duration, and measurement criteria are negotiated as part of the purchase agreement.

Buyers love earnouts for two reasons. First, earnouts bridge valuation gaps. When a buyer and seller disagree on what the business is worth, an earnout lets both sides get what they want in theory. The seller gets full value if the projections hit. The buyer pays full price only if they do.

Second, earnouts shift risk. A buyer paying 6x EBITDA is accepting the risk that EBITDA declines. An earnout converts that risk into a contingent payment. If EBITDA does not grow as projected, the seller does not collect.

For sellers, the picture is less rosy. Studies of earnout disputes show that sellers collect less than the face value of their earnouts far more often than they collect more. The reasons are predictable: integration decisions that redirect revenue, cost allocations that inflate expenses and suppress EBITDA, management changes that affect customer relationships, and measurement disagreements that end up in arbitration years after close.

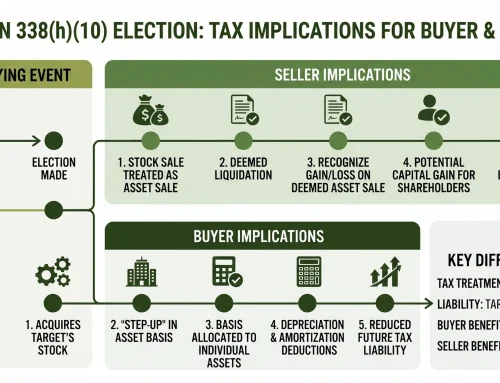

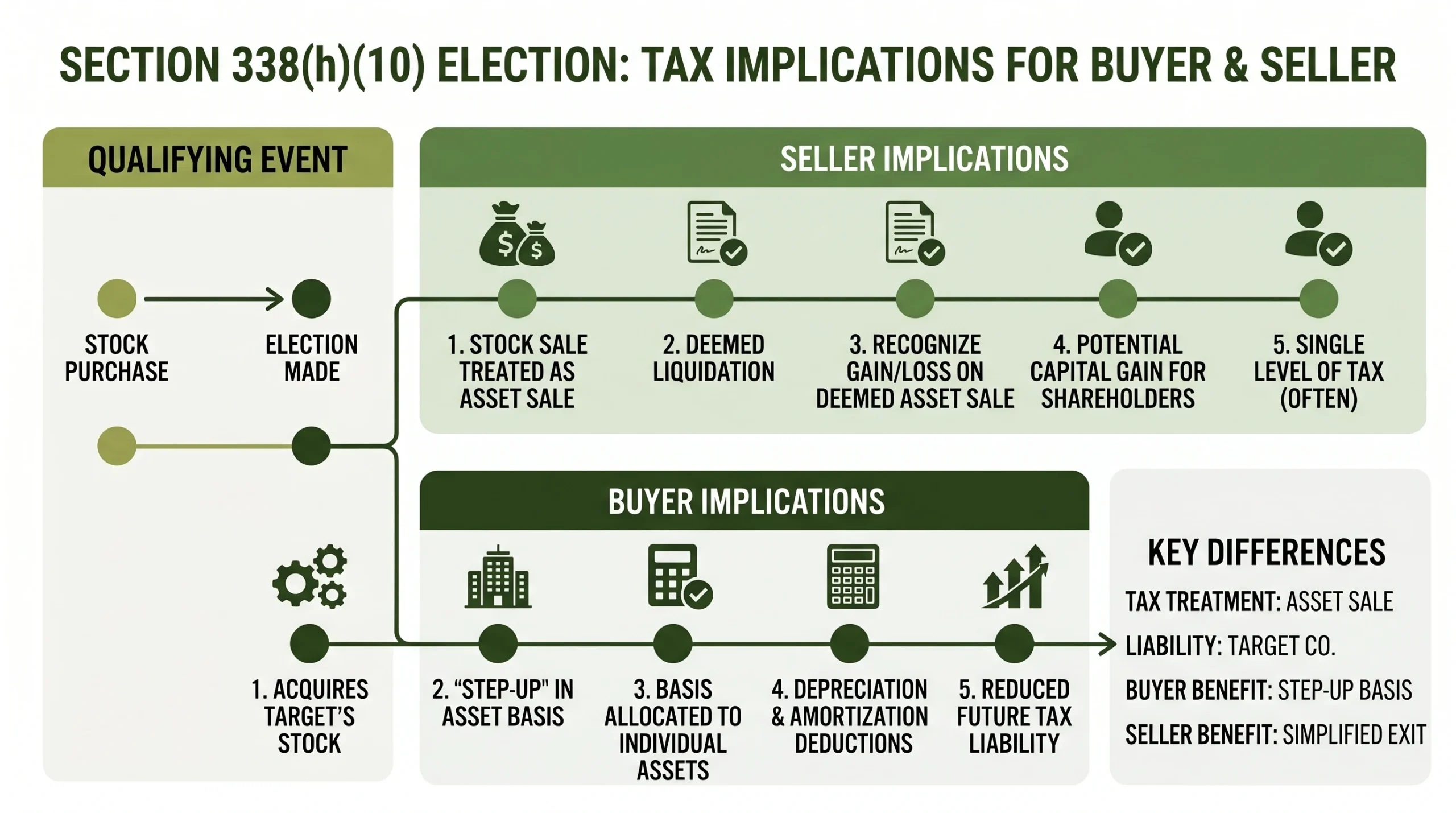

When payments are received across more than one tax year, the installment method may apply, as detailed in IRS Publication 537, Installment Sales.

Why Do Most Earnouts Fail Sellers?

EBITDA is the most common earnout metric, and it is the most open to buyer influence. After closing, the buyer controls the accounting. The buyer decides whether to allocate shared services overhead to the acquired entity, what depreciation schedule to apply to newly acquired equipment, how to account for intercompany deals, and what management fee to charge for parent company services. Each of these decisions directly affects reported EBITDA.

A buyer who acquires a business and then charges it a 5% management fee for “corporate overhead services” has added an expense line that did not exist pre-close. If the earnout is EBITDA-based, that management fee reduces EBITDA below the earnout threshold. The seller collects nothing. The buyer has not technically breached the contract. They have exercised operational discretion.

Revenue is harder to manipulate because it requires moving customer relationships or revenue streams out of the acquired entity entirely. That is a more visible and legally riskier action than cost allocation decisions. This is why revenue-based earnouts are better for sellers.

The second major failure mode is buyer underinvestment. A buyer who believes the earnout target is unlikely to be hit has no financial incentive to invest in the business. They may not hire the sales team the seller wanted, fund the marketing campaign, or accelerate the product development that would have driven growth.

Structure 1: Revenue-Based Earnouts Instead of EBITDA-Based

The first and most important seller-protective provision is the choice of earnout metric. Revenue is better than EBITDA for sellers in most situations because of three facts.

Revenue is a line item the buyer cannot reduce through cost allocation, depreciation choices, or management fee charges. To reduce revenue recognized in the acquired entity, the buyer would have to redirect customer contracts to a different entity. That is visible, often contractually prohibited, and legally actionable if done to suppress an earnout payment.

Revenue targets are simpler to measure and verify. A revenue-based earnout with a well-defined revenue recognition policy requires less accounting interpretation than EBITDA, which involves multiple below-the-line adjustments.

Practical use: the revenue earnout agreement should specify exactly which revenue streams are included (total net revenue of the acquired entity, using the same accounting policies as pre-close), how revenue from new products or markets is treated, and what happens if the buyer moves existing customers to a different entity.

Sellers negotiating EBITDA-based earnouts, when revenue is not acceptable to the buyer, should require explicit covenants prohibiting new management fees, capping shared services allocations at pre-close levels, and requiring seller consent for capital expenditure decisions above a defined threshold.

Structure 2: Accelerators That Reward Outperformance

A standard earnout pays the seller a defined amount if the target is met, nothing more. An earnout with an accelerator pays the seller a higher amount for performance above the target. It rewards outperformance rather than capping the seller’s upside at the base target.

Example: A seller negotiates an earnout of $2M if the business hits $10M in revenue in Year 1 post-close. Without an accelerator, the seller collects $2M regardless of whether revenue is $10M or $14M. With an accelerator, the seller might collect $2M for hitting $10M, $2.5M for $11M, $3M for $12M, and so on, with each more $1M in revenue above target generating $500K in earnout consideration.

Accelerators matter for sellers because they reflect the asymmetric upside that motivated the earnout. If the seller believed the business was worth more than the buyer was willing to pay at closing, and the business then performs above the buyer’s model, the accelerator ensures the seller participates in that outperformance. Without it, the seller gifts that value to the buyer.

Buyers resist accelerators because they cap their upside.

Structure 3: Earnout Floors, The Minimum Guarantee

An earnout floor is a minimum payment that the seller receives regardless of post-close performance. It is the provision that most directly protects sellers from the scenario where buyer operational decisions suppress earnout metrics below threshold.

A floor guarantees that a portion of the deferred consideration is, in effect, treated as non-contingent. The seller collects the floor regardless of outcome. Only the amount above the floor is contingent on performance.

Example: A seller negotiates a $3M earnout with a $1M floor. The buyer pays $1M at the end of Year 1 no matter what. If performance triggers earn $2M above the floor, the seller collects $3M total. If performance is weak, the seller still collects $1M.

Floors are negotiated as a percentage of the total earnout, typically 25%–40% of the earnout value. Buyers resist floors for the same reason they like earnouts: they want all consideration to be contingent. Sellers should frame the floor as the portion that compensates for operational risk they cannot control, specifically, the risk that buyer decisions affect the metric, not just market conditions.

David Hern CPA ABV ASA, founder of Sofer Advisors, brings a Heart of a Teacher to every engagement – translating complex valuation methodology into clear, actionable guidance that clients can act on before and after the report is delivered. With 15+ years of valuation experience, 11+ expert witness cases across multiple jurisdictions, and 180+ five-star Google reviews, David built Sofer Advisors into an Inc. 5000-recognized firm. The Sofer Difference is a four-phase process of Discovery, Diligence, Analysis, and Delivery that ensures every conclusion is defensible, documented, and tied to the specific facts of the business.

While national firms like Stout and Kroll serve large enterprise clients, Sofer Advisors specializes in middle-market businesses that require personalized attention, direct access to credentialed professionals, and a next business day response policy.

Structure 4: Independent Accounting and Binding Arbitration Clauses

The fourth seller-protective structure is procedural rather than financial. It is the mechanism through which earnout measurement disputes are resolved. Without it, the buyer controls the measurement, and the seller’s only recourse is litigation, which is expensive, slow, and uncertain.

A well-drafted earnout agreement includes three procedural protections:

- Independent accounting review. The buyer provides earnout calculations within a defined period after each measurement date (e.g., 60 days after each fiscal year-end). The seller has the right to review and dispute the calculation within a defined window (e.g., 30 days). If disputed, the parties engage an independent accounting firm to review the calculation and issue a binding determination.

- Binding arbitration. If the independent accounting review does not resolve the dispute, the matter goes to binding arbitration rather than litigation. Arbitration is faster, less expensive, and private. The arbitration clause should specify the rules (e.g., AAA commercial arbitration), the selection method for the arbitrator, and allocation of fees.

- Pre-defined accounting method. The earnout agreement should specify, in explicit detail, the accounting policies to be used in earnout calculations, matching the pre-close accounting policies to the maximum extent possible. Ambiguity in accounting method is the primary source of earnout disputes.

How Do Buyers Destroy Earnout Value Without Technically Breaching?

The behaviors that most commonly suppress earnout payments, short of outright fraud, include the following:

- Loading expenses. Charging new management fees, allocating corporate overhead, or changing depreciation and amortization schedules in ways that suppress EBITDA below earnout thresholds. This is the most common issue in EBITDA-based earnouts.

- Deferring revenue recognition. Shifting revenue recognition timing to push revenue into a period after the earnout window closes.

- Starving sales investment. Not approving headcount, marketing budgets, or capital projects that the seller’s projections assumed would drive earnout performance.

- Restructuring the business. Merging the acquired entity into a parent entity or moving customers to related entities, each making it impossible to measure earnout performance at the entity level.

The protection against these behaviors is a combination of operational covenants and measurement specificity, ensuring the earnout agreement defines which entity’s financials are measured and prohibits intercompany transfers.

How Long Should an Earnout Last?

The standard earnout duration in small and mid-market M&A is 1–3 years. One year is buyer-friendly because a single bad year can wipe out the entire earnout. Three years allows for multiple periods in which strong performance can overcome a weak year, but it also extends the seller’s operational exposure.

Sellers generally prefer shorter earnout periods with higher floors rather than longer periods with lower floors.

The earnout period should match the specific performance scenario being bridged. If the valuation gap relates to Year 1 and Year 2 growth projections, a 2-year earnout is appropriate.

How Do You Value an Earnout at Closing?

For financial accounting purposes under ASC 805, a contingent consideration earnout must be recognized at fair value at the closing date. For sellers, understanding the economic value of the earnout they are accepting is essential before signing.

The valuation of an earnout involves assigning probabilities to the scenarios under which it pays, full payment, partial payment, and no payment, and discounting the resulting expected cash flows at an appropriate risk rate. A seller who models this analysis honestly often finds that the stated earnout value overstates the expected value they will actually receive.

Example: A $3M earnout with no floor, EBITDA-based, over 2 years. The probability of full payment is 50%. Partial payment of $1M is 30%. No payment is 20%. The probability-weighted expected value is ($3M x 50%) + ($1M x 30%) + ($0 x 20%) = $1.8M. The seller should compare $1.8M against what more upfront consideration they could extract from the buyer in lieu of the earnout.

This analysis gives sellers the quantitative basis to negotiate more upfront consideration or demand the structural protections that bring the earnout’s expected value closer to its stated value.

The questions below address the most common issues business owners raise before engaging a qualified appraiser for a negotiating earnout seller protections engagement.

Frequently Asked Questions

What is an earnout in M&A?

An earnout is a contingent payment mechanism where the seller receives more consideration after closing if the acquired business meets defined performance targets.

Why do sellers often dislike earnouts?

Buyers control the business post-close and can make operational and accounting decisions that reduce the metrics on which earnout payments are based.

What is better for a seller, a revenue earnout or EBITDA earnout?

Revenue earnouts are generally better for sellers because revenue is harder for buyers to manipulate through cost allocation or accounting adjustments.

What is an earnout accelerator?

An accelerator pays the seller an increasing amount for performance above the earnout target, rewarding outperformance rather than capping the seller’s upside.

What is an earnout floor?

An earnout floor is a minimum guaranteed payment that the seller receives regardless of post-close performance.

How long do earnouts typically last?

Most earnouts in small and mid-market deals run 1–3 years.

What happens if there is a dispute about earnout calculations?

Without dispute resolution provisions, the seller’s only recourse is litigation. A well-drafted earnout agreement includes an independent accounting review process and binding arbitration.

Can an earnout be paid in stock rather than cash?

Yes. Some earnouts are payable in buyer equity or a combination of cash and stock.

What covenants should sellers require during the earnout period?

Key covenants include: prohibition on new management fees charged to the acquired entity, a cap on shared services allocations at pre-close levels, requiring seller consent for capital expenditure decisions above a defined threshold, and maintaining the acquired entity’s separate legal existence.

How is an earnout taxed for the seller?

Earnout payments are generally taxed as ordinary income or capital gains depending on how the deal is structured and what the earnout consideration is deemed to relate to, services, IP, or equity.

Related Case Studies

- Business Valuation For Mergers Buy Side Vs Sell Side

- Fairness Opinion In MA Atlanta What Georgia Business Owners And Boards Need To Know

- Selling A Business In Georgia Complete Exit Planning Guide 2026

Executive Summary

- Earnouts are structurally advantaged toward buyers because buyers control post-close operations and the accounting decisions that determine earnout metrics.

- Revenue-based earnouts are the most important seller protection – harder to manipulate than EBITDA-based earnouts through cost allocation and accounting decisions.

- Accelerators ensure sellers benefit from outperformance. Floors ensure sellers receive minimum consideration regardless of buyer operational choices.

What Should You Do Next?

If you are in a deal where an earnout is on the table, understanding its true economic value, and the structural provisions that protect that value, requires expertise in both valuation and deal structure. David Hern CPA ABV ASA, founder of Sofer Advisors, holds dual ASA and ABV credentials recognized by the IRS, SEC, and FINRA, with 15+ years of valuation experience and 180+ five-star Google reviews. Schedule a consultation to discuss your business valuation needs.

People Also Read

- Why You Must Start Planning Your Business Exit Now With The Right Valuation Expert

- When To Start Succession Planning Your Strategic Timeline Guide

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com/about-us/ or schedule a consultation at soferadvisors.com/contact-us/.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}