Last Updated: April 2026

An ESOP feasibility study is a structured financial and operational analysis that determines whether a company can support the debt, repurchase obligations, and share value required for an employee stock ownership plan. The study outputs a go or no-go recommendation and a preliminary valuation range. According to the NCEO (2024), approximately 6,500 ESOP-owned companies operate in the United States, covering nearly 14 million employee-owners, most of which began with exactly this kind of preliminary review.

At Sofer Advisors, we provide independent business valuations and ESOP feasibility reviews for owners evaluating employee ownership as an exit strategy. A credentialed feasibility analysis identifies whether your company meets the requirements before you invest in a full ESOP transaction.

Business owners evaluating an ESOP need to understand what the study covers, who qualifies, what it costs, and what risks to anticipate. The sections below walk through each component in the order advisors and owners follow during a typical preliminary review.

Key Takeaways

- Definition – an ESOP feasibility study is a preliminary financial analysis determining whether a company’s cash flows, debt capacity, and share value can support an employee ownership plan transaction.

- Qualifying Threshold – most ESOP transactions require at least $1 million in annual EBITDA, 20 or more employees, and an owner willing to sell at least 30 percent of equity in the initial transaction.

- Study Components – a complete feasibility study covers valuation range, debt capacity, repurchase obligation modeling, employee census, and tax benefit projections.

- Cost Range – a feasibility study typically costs $7,500 to $25,000 depending on company complexity, the depth of valuation analysis, and whether repurchase obligation modeling is included.

- Primary Purpose – the study confirms transaction viability before legal and financing commitments are made, protecting both the owner and the lender.

Each of these components determines whether an ESOP transaction is viable at the proposed ownership transfer size and price. The sections below examine each in detail.

What Is an ESOP Feasibility Study?

An ESOP feasibility study is a preliminary analysis commissioned before a company proceeds with a formal employee stock ownership plan transaction. The study answers three foundational questions: Can the company afford the debt required to buy out the owner? Can the business sustain the annual repurchase obligation as employees retire and redeem their shares? Does the estimated share value support a transaction price acceptable to both the owner and the ESOP trust?

The study is not a full ESOP transaction. It is a structured screen that filters out companies whose cash flows, ownership structure, or employee base make a formal ESOP impractical or unaffordable before $50,000 or more in transaction costs are committed. According to the AICPA (2023), the fair market value standard applies to all ESOP trustee appraisals, requiring a credentialed independent appraiser regardless of whether the engagement is a feasibility screen or a full transaction opinion.

Who Qualifies as a Good ESOP Candidate?

A strong ESOP candidate is a profitable company with stable cash flows, a workforce of 20 or more employees, and an owner ready to sell at least 30 percent of equity in the initial transaction. Companies with predictable recurring revenue, low customer concentration, and a capable management team make the strongest candidates. Seasonal, owner-dependent, or heavily indebted companies face structural challenges the feasibility study will identify.

The four characteristics most associated with successful ESOP candidates are:

- Sufficient EBITDA – minimum $1 million in annual normalized EBITDA provides the cash flow base required to service the acquisition debt and fund the annual repurchase obligation

- Qualified Workforce – at least 20 full-time employees creates a meaningful ownership base; below this threshold, plan administration costs make an ESOP economically inefficient

- Transferable Management – a leadership team capable of operating without the selling owner reduces key-person risk and increases lender confidence in the transaction

- Owner Flexibility – owners willing to remain involved post-transaction and accept deferred proceeds through a seller note or staged sale create more financeable structures

Companies with $500,000 to $999,000 in EBITDA are not automatically disqualified, but they require deeper scrutiny during the feasibility review. The debt service on even a modest ESOP transaction can consume 30 to 40 percent of pre-tax cash flow, leaving thin coverage for operating contingencies. An independent appraisal at the feasibility stage gives the owner a realistic valuation range before the company takes on the debt load of a formal transaction.

What Does an ESOP Feasibility Study Cover?

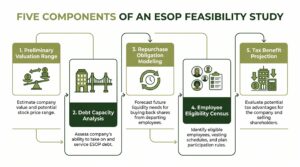

A complete ESOP feasibility study covers five analytical components: a preliminary business valuation range, a debt capacity analysis, a repurchase obligation model, an employee eligibility census, and a tax benefit projection. Each component feeds into the final go or no-go recommendation, and each must be completed by an independent appraiser before the owner and trustee commit to a formal transaction structure.

The five components of a standard feasibility study are:

- Preliminary Valuation Range – an estimated fair market value range for the company stock, based on normalized EBITDA and comparable transaction multiples, before a full formal appraisal is commissioned

- Debt Capacity Analysis – tests whether the business can service the acquisition loan (typically 4x to 6x EBITDA) from operating cash flow at the 1.25x coverage ratio lenders require

- Repurchase Obligation Modeling – projects the annual cash cost of buying back shares from retiring employees over a 10 to 20-year horizon, a long-term liability frequently underestimated in informal ESOP assessments

- Employee Eligibility Census – identifies which employees will participate, how quickly shares vest, and what the demographic mix means for repurchase timing and cost

- Tax Benefit Projection – quantifies the federal income tax advantages under IRC Section 1042, including the capital gains rollover for C corporation sellers and the S corporation income tax exclusion

The repurchase obligation component is the most frequently underestimated risk in ESOP transactions. A company that can service its acquisition debt may still face a cash crisis 10 to 15 years post-transaction if the repurchase obligation grows faster than earnings. The feasibility study models this liability explicitly, allowing the owner and trustee to structure the initial transaction at a size and debt level the company can sustain across an entire employee generation without triggering a cash shortfall. National advisory firms such as Stout and Kroll perform ESOP trustee valuations in institutional-scale transactions. Sofer Advisors delivers the same credentialed independent analysis for lower middle market ESOP candidates at a cost structure appropriate to the transaction size.

How Much Does an ESOP Feasibility Study Cost?

An ESOP feasibility study costs $7,500 to $25,000 depending on company size, the complexity of the normalized EBITDA calculation, whether a formal preliminary valuation opinion is included, and the depth of the repurchase obligation model. Studies for companies with complex capital structures or disputed normalizations sit at the upper end; straightforward privately held companies fall in the $7,500 to $12,000 range.

| Study Component | Basic Study | Full Study |

|---|---|---|

| Preliminary Valuation Range | Yes | Yes |

| Debt Capacity Analysis | Yes | Yes |

| Repurchase Obligation Model | No | Yes |

| Employee Eligibility Census | No | Yes |

| Tax Benefit Projection | No | Yes |

| Formal Written Valuation Opinion | No | Yes |

| Lender-Ready Documentation | No | Yes |

The feasibility study is not the same cost as the full ESOP valuation. A formal ESOP valuation (the independent appraisal the trustee requires to close the transaction) is a separate engagement costing $15,000 to $35,000 and taking six to ten weeks. Owners who complete the feasibility study first avoid commissioning the full valuation for a company that cannot meet the basic financial thresholds, saving $15,000 to $35,000 in unnecessary advisory spend.

What Are the Risks of an ESOP Transaction?

An ESOP transaction carries structural risks distinct from a third-party sale because the purchase is financed with company debt that must be repaid from future earnings. Over-leverage is the most common failure mode: a transaction sized too aggressively against projections leaves the company unable to service debt during a revenue shortfall. The repurchase obligation creates a second long-term liability that compounds the leverage risk if not modeled accurately during the feasibility phase.

The four risks most frequently identified in ESOP transactions are:

- Over-Leverage Risk – acquisition debt exceeding sustainable debt service capacity forces management to cut investment or seek emergency refinancing; lenders require 1.25x coverage as a standard covenant floor

- Repurchase Obligation Risk – as employees retire and redeem shares, the company must fund repurchases from operating cash; this obligation grows over time and can exceed the original acquisition debt in a mature ESOP

- Valuation Dispute Risk – the ESOP trustee has a fiduciary duty under ERISA (2024) to pay no more than fair market value; when the selling owner’s expectation diverges from the independent appraisal, the transaction stalls

- Key Person Dependency – if the company’s value is tied to the selling owner’s relationships or expertise, the ESOP trustee will apply a discount to the preliminary valuation that reduces total proceeds

A feasibility study that identifies these risks early allows the owner and advisors to restructure or scale the proposed transaction before committing to legal and financing costs. Owners who discover a repurchase obligation problem or leverage constraint during the feasibility phase can adjust the transaction size, extend the seller note, or implement a staged ownership transfer rather than discovering the structural problem after the transaction has closed and the debt obligations are fixed.

Completing the feasibility study before engaging a trustee or ESOP counsel is the most cost-effective decision an owner can make. An independent preliminary valuation anchors the transaction price where the trustee and lender will support it, protecting the owner from mispriced expectations that unravel at closing.

Frequently Asked Questions

What is a feasibility study for ESOP?

An ESOP feasibility study is a preliminary financial analysis that evaluates whether a company can support an employee stock ownership plan transaction. It covers business value, debt capacity, repurchase obligations, and employee eligibility before the owner commits to full transaction costs. The study produces a go or no-go recommendation and a preliminary value range before legal and financing commitments are made.

What is the ESOP 30% rule?

The ESOP 30 percent rule refers to the minimum ownership threshold that qualifies selling shareholders of a C corporation for the IRC Section 1042 tax-deferred rollover. A selling owner who sells at least 30 percent of outstanding C corporation stock to an ESOP can defer capital gains tax by reinvesting the proceeds in qualified replacement property. The rule does not apply to S corporations.

How much does an ESOP feasibility study cost?

An ESOP feasibility study typically costs $7,500 to $25,000 depending on company size, the complexity of the EBITDA normalization, and whether a formal preliminary valuation opinion is included. Studies for companies with complex capital structures sit at the upper end. A basic feasibility screening for a straightforward privately held company falls in the $7,500 to $12,000 range. The feasibility study is a separate, lower-cost engagement from the full ESOP valuation, which costs $15,000 to $35,000.

What size business qualifies for an ESOP?

Most ESOP transactions require a minimum of $1 million in annual normalized EBITDA and at least 20 full-time employees to make the plan economically viable. Companies below these thresholds face disproportionate plan administration costs relative to the benefit per employee-owner. Enterprise value typically ranges from $5 million to several hundred million for viable ESOP candidates. Companies with lower EBITDA need a more conservative debt structure and a longer seller note.

How long does an ESOP feasibility study take?

A complete ESOP feasibility study typically takes four to eight weeks from receipt of financial information to delivery of the final report. Companies with complex ownership structures or disputed EBITDA normalizations may require eight to twelve weeks. The timeline depends on the speed of financial document production. A basic feasibility screening can be completed in two to three weeks when financials are clean.

What happens after the ESOP feasibility study?

If the feasibility study produces a positive recommendation, the next step is engaging a trustee, ESOP counsel, and a lender to structure the formal transaction. The appraiser then issues a full formal valuation opinion confirming the transaction price does not exceed fair market value. If the study identifies obstacles, the owner can restructure the proposed transaction or pursue an alternative exit strategy.

Can an S corporation do an ESOP?

Yes, an S corporation can sponsor an ESOP, and S corporation ESOPs carry significant tax advantages. Income attributable to ESOP-owned shares is exempt from federal income tax, meaning a 100 percent ESOP-owned S corporation pays no federal corporate income tax on that portion. However, S corporation shareholders do not qualify for the IRC Section 1042 capital gains deferral available to C corporation sellers. Owners of S corporations often evaluate converting to C corporation status to access the Section 1042 rollover.

How much does an ESOP valuation cost from Sofer Advisors?

An independent ESOP valuation from Sofer Advisors typically costs $15,000 to $35,000 depending on company size, the complexity of the capital structure, and whether the engagement includes a repurchase obligation study alongside the formal share valuation. A feasibility-level engagement costs $7,500 to $25,000 and is typically completed four to eight weeks from receipt of financial materials. Contact Sofer Advisors to scope the right engagement for your transaction stage.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

An ESOP feasibility study determines whether a company can support an employee ownership plan transaction before the owner commits to full legal and financing costs. The study covers five components: preliminary valuation, debt capacity, repurchase obligation, employee census, and tax benefit projection. Strong candidates have at least $1 million in EBITDA and 20 or more employees. Over-leverage and repurchase obligation growth are the primary risks; both are manageable with an independent credentialed feasibility study before the formal transaction begins.

What Should You Do Next?

Commission a feasibility study before engaging an ESOP trustee or transaction counsel. A credentialed preliminary analysis gives you a defensible value range and identifies structural obstacles before you commit to $50,000 or more in transaction costs.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides ESOP valuations and feasibility studies for business owners evaluating employee ownership as an exit strategy. Schedule a consultation to discuss the right approach for your transaction.

People Also Read

- ESOP Transaction Process: A Complete Guide for Business Owners

- Business Succession Planning Tips for Smooth Ownership Transfers

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}