Last Updated: April 2026

An asset sale vs stock sale is the foundational structural choice in any business acquisition: in an asset sale, the buyer acquires specified individual assets and assumes only designated liabilities, while in a stock sale, the buyer purchases the seller’s equity interest directly, inheriting the entity and its entire history of assets, contracts, permits, and liabilities. The decision reshapes the tax outcome for both parties, determines whether the buyer receives a stepped-up basis in acquired property, and governs how goodwill and intangible assets are treated on the buyer’s books going forward.

For business owners receiving an acquisition offer, the structure chosen can shift after-tax proceeds by hundreds of thousands of dollars on the same gross purchase price. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides independent business appraisals that establish the defensible fair market value required for IRC 1060 purchase price allocation in asset sales, equity value documentation in stock sales, and IRS audit defense in both structures across middle-market transactions nationwide.

The tax, legal, and valuation differences between these two structures are consequential enough to determine whether a deal closes on acceptable terms or stalls at the letter of intent stage. The Key Takeaways below summarize the essential distinctions before the detailed analysis that follows.

Key Takeaways

- IRC 1060 Allocation Required in Asset Sales: Under IRC 1060, buyers and sellers must jointly allocate the purchase price across seven IRS asset classes, with each class carrying a different tax character for the seller, from ordinary income on inventory and recaptured depreciation to capital gains on goodwill.

- Capital Gains Treatment in Stock Sales: Individual sellers in a stock sale generally recognize the entire gain as long-term capital gains, avoiding the ordinary income exposure created by depreciation recapture on equipment and other depreciable assets in an asset sale.

- Buyers Get a Stepped-Up Basis in Asset Sales: The buyer’s cost basis in each acquired asset equals its allocated purchase price, enabling new depreciation schedules and 15-year goodwill amortization under IRC 197 — deductions unavailable in a stock sale where the buyer inherits the seller’s historic basis.

- Hidden Liabilities Transfer in a Stock Sale: The buyer acquires 100% of the legal entity, including all contingent, unknown, and undisclosed liabilities; an asset sale buyer assumes only explicitly named obligations.

- Valuation Supports Both Structures: An independent business appraisal establishes the defensible allocation basis for IRC 1060 in an asset sale and documents fair market value against IRS challenge in a stock sale.

Each of these distinctions creates real economic stakes at the negotiating table. The sections below examine how each structure is taxed, why buyers and sellers favor opposite structures, how IRC 1060 works, and where business valuation fits into both transaction types.

What Is the Difference Between Asset and Stock Sales?

An asset sale transfers specific named assets — equipment, inventory, receivables, contracts, intellectual property, and goodwill — from the seller’s entity to the buyer’s, with the seller’s legal entity surviving the transaction as a shell. Only liabilities the buyer explicitly agrees to assume transfer. The buyer typically forms a new entity to hold the acquired property and begins with a clean balance sheet except for those assumed obligations.

A stock sale transfers the equity interest itself. The buyer acquires shares or membership units, the entity continues without interruption, and all contracts, licenses, and regulatory permits remain in place because no change of ownership occurs at the entity level. This continuity is particularly valuable when key licenses are non-assignable or when customer contracts contain anti-assignment clauses that would require third-party consent in an asset deal.

| Feature | Asset Sale | Stock Sale |

|---|---|---|

| What transfers | Named assets and assumed liabilities | 100% of equity in the legal entity |

| Seller’s tax character | Ordinary income and capital gains (mixed) | Primarily capital gains for individuals |

| Buyer’s tax basis | Stepped up to allocated purchase price | Inherited (carryover) from seller |

| New depreciation for buyer | Yes, on full allocated value | No; continues seller’s existing schedule |

| Goodwill amortization for buyer | 15 years under IRC 197 | No new amortization on existing basis |

| Hidden liabilities | Buyer assumes named items only | All liabilities transfer, including unknown |

| License and contract continuity | May require assignment consent | Generally transfers automatically |

| IRS allocation required | Yes, under IRC 1060 (Form 8594) | No equivalent requirement |

How Is an Asset Sale Taxed for Both Sides?

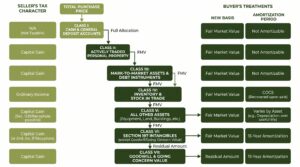

For the seller, asset sale tax treatment depends on the character of each asset class. Inventory and accounts receivable generate ordinary income. Equipment and machinery trigger depreciation recapture as ordinary income under IRC 1245 and 1250 — meaning previously deducted depreciation is taxed back at rates up to 37% before any capital gain analysis begins. Goodwill and going concern value, allocated last under IRC 1060’s residual method, generate long-term capital gain taxed at preferential rates of 15% to 20%. A business with $500,000 in depreciated equipment may recognize $500,000 of ordinary income from recapture alone, materially reducing net after-tax proceeds compared to a stock sale at the same headline price.

For the buyer, asset sale treatment is straightforward and advantageous. Each acquired asset receives a stepped-up cost basis equal to its allocated purchase price. Equipment can be placed on a new depreciation schedule, potentially eligible for 100% bonus expensing under current law. Customer lists, non-compete agreements, and other identifiable intangibles are amortized over 15 years under IRC 197. Goodwill is also amortized over 15 years, creating a predictable annual deduction stream that reduces the buyer’s post-close effective tax cost.

The seven IRC 1060 asset classes allocated in prescribed order, from first to last:

- Class I: Cash and cash equivalents — no gain in most cases.

- Class II: Actively traded securities and certificates of deposit.

- Class III: Mark-to-market assets including accounts receivable and loans.

- Class IV: Inventory and property held primarily for sale to customers.

- Class V: All other tangible assets, including equipment — subject to IRC 1245/1250 recapture.

- Class VI: IRC 197 intangibles other than goodwill, including customer lists and non-competes.

- Class VII: Goodwill and going concern value — taxed as long-term capital gain for the seller.

How Is a Stock Sale Taxed for Both Sides?

In a stock sale, an individual seller who has held equity for more than one year generally recognizes the entire gain as long-term capital gain, taxed at federal rates of 0%, 15%, or 20% depending on income level. There is no depreciation recapture at the shareholder level, no IRC 1060 allocation, and no ordinary income exposure from business assets unless the entity is a pass-through with separately identifiable hot assets. This single capital gains rate treatment on the full gain is the primary reason individual sellers — particularly founders who have held equity for years — prefer stock sale structures.

C-corporation sellers benefit most from stock sale capital gains treatment, since the alternative asset sale route would expose the corporation to ordinary income tax on recapture before the after-tax proceeds flow to the shareholder. S-corporation and partnership sellers must analyze whether built-in gains or ordinary income assets create exposure at the entity level under their specific tax elections, even in a nominally stock transaction. According to IRS Publication 544 (2024), the sale of partnership interests is generally treated as a capital asset transaction, but unrealized receivables and inventory items trigger ordinary income recognition even in an interest sale.

For the buyer, the stock sale tax disadvantage is significant. No new depreciation schedules begin, existing goodwill carries no additional amortization rights, and any built-in gain in the entity’s assets becomes the buyer’s future liability. Buyers in stock transactions often negotiate a price discount to compensate for the absence of the tax step-up benefit they would receive in an asset purchase.

Schedule your free consultation with Sofer Advisors to model how transaction structure affects your after-tax proceeds and understand how an independent appraisal protects your position in either an asset or stock sale. Discover The Sofer Difference.

Why Do Buyers and Sellers Disagree on Structure?

The asset sale vs stock sale preference creates a natural conflict at the negotiating table because each party benefits from opposite structures. Sellers want capital gains treatment on the full gain; buyers want a basis step-up to generate future deductions. This structural tension is the most common M&A negotiating point in middle-market transactions, and it is rarely resolved without some form of economic compromise, most often a purchase price adjustment or tax gross-up.

Sellers carry specific risks in asset sales that reinforce their preference for stock structures. In an asset sale, the seller pays taxes on ordinary income from recapture at or before closing, creating a cash timing problem when the deal includes earnout provisions or seller financing. The seller also retains the legal entity post-closing with potential ongoing obligations, including state filings, payroll tax, and residual liabilities, until the shell entity is formally wound down.

According to AICPA Forensic and Valuation Services (2023), contingent and undisclosed liabilities are among the leading sources of post-close M&A disputes, which explains why buyers push hard for asset structures. Representations and warranties insurance has grown as a tool to bridge this risk in stock sales, but it adds transaction cost and does not eliminate inherited liability exposure. Buyers accepting stock sale structure typically negotiate for indemnification escrows, lower price, or enhanced reps and warranties coverage to offset what they cannot recover through tax deductions.

What Is IRC 1060 and Why Does It Matter?

IRC 1060 governs purchase price allocation in every transaction treated as an asset acquisition for tax purposes. Both the buyer and seller must report a consistent allocation on their respective returns using IRS Form 8594 (Asset Acquisition Statement) for the tax year in which the sale closes. If the parties report inconsistent allocations, the IRS has authority to reallocate the purchase price to reflect arm’s-length fair market values under IRC 1060(d), exposing the non-compliant party to additional tax and penalties.

The allocation follows the residual method: the full purchase price is first applied to Class I assets at face value, then successively to each class in order through Class VII. Whatever remains after all other classes are satisfied flows to goodwill and going concern value. Because sellers prefer maximum allocation to Class VII (capital gains) and buyers prefer maximum allocation to Class V depreciable equipment (fast deductions under bonus depreciation), the allocation negotiation is effectively a second pricing discussion layered on top of the headline enterprise value.

An independent appraisal of individual asset classes — equipment at fair market value, customer relationships at their income-derived value, non-compete agreements at their economic cost — provides the arm’s-length support that prevents IRS reallocation and resolves buyer-seller allocation disputes before they reach the purchase agreement. Without documented values, the allocation is driven purely by negotiation, which the IRS treats skeptically.

How Does a Business Valuation Fit In?

In an asset sale, valuation serves two roles: establishing the aggregate fair market value that anchors the purchase price and supporting the IRC 1060 allocation across individual asset classes. A purchase price allocation under ASC 805 is also required after closing for financial reporting purposes, recognizing acquired tangible assets, identifiable intangibles, and residual goodwill at their acquisition-date fair values. Without credentialed appraisal support, the buyer’s auditors will challenge the allocation and the IRS may reallocate value on audit.

In a stock sale, valuation documents the equity fair market value against IRS challenge, supports estate tax reporting if the seller dies after closing, and anchors the buyer’s understanding of what they paid for against the business’s intrinsic worth. According to the American Society of Appraisers (ASA) (2023), stock sale transactions where the purchase price departs materially from independently appraised fair market value are vulnerable to IRS recharacterization as partial gifts in related-party transactions. Credentialed valuation firms including Kroll and Stout provide transaction support in large-cap M&A; for middle-market buyers and sellers, Sofer Advisors provides business valuation for mergers and acquisitions with direct ABV and ASA credentialed oversight on every engagement, ensuring the concluded value is documented and defensible regardless of deal structure.

Frequently Asked Questions

What is the main difference between an asset sale and a stock sale?

In an asset sale, the buyer acquires specific named assets and assumes only designated liabilities, with the seller’s legal entity surviving intact. In a stock sale, the buyer acquires the equity interest in the entity itself, which continues operating with all of its assets and liabilities unchanged. The primary practical consequence is tax treatment: asset sales produce a mix of ordinary income and capital gains for the seller, while stock sales generally produce all-capital-gains treatment for individual sellers on the same gain.

Why do buyers prefer asset sales over stock sales?

Buyers prefer asset sales because they receive a cost basis in each acquired asset equal to the allocated purchase price, enabling new depreciation schedules on equipment and 15-year amortization of goodwill and other IRC 197 intangibles. Buyers also avoid inheriting the seller’s unknown or contingent liabilities, since only specifically assumed obligations transfer. The combination of a basis step-up and liability protection creates a materially lower after-tax cost for the buyer compared to acquiring the same business through a stock purchase.

Why do sellers prefer stock sales over asset sales?

Sellers prefer stock sales because the gain on the sale of a qualifying equity interest held more than one year is generally taxed at long-term capital gains rates of 15% to 20%, rather than at ordinary income rates of up to 37% on depreciation recapture that an asset sale triggers. In an asset sale, previously deducted depreciation on equipment under IRC 1245 and 1250 is recaptured as ordinary income at closing. A stock sale bypasses this recapture entirely at the shareholder level, producing higher after-tax proceeds on the same gross purchase price.

What is IRC 1060 and when does it apply?

IRC 1060 applies to any direct or indirect acquisition of assets that constitute a trade or business. It requires both the buyer and seller to allocate the purchase price across seven prescribed asset classes using the residual method and to report the allocation consistently on IRS Form 8594. The law prevents parties from agreeing to allocations that benefit one side at the IRS’s expense by requiring arm’s-length fair market values at each class level. Inconsistent reporting between buyer and seller triggers IRS scrutiny of both returns.

How is goodwill taxed in an asset sale compared to a stock sale?

In an asset sale, goodwill allocated to Class VII under IRC 1060 generates long-term capital gain for the seller, taxed at 15% to 20%. For the buyer, goodwill is amortized over 15 years under IRC 197, creating a predictable annual deduction. In a stock sale, no goodwill is separately identified or amortized; the buyer inherits the entity’s existing tax basis without new deduction rights. Sellers negotiating allocation in an asset sale typically want maximum value assigned to Class VII to minimize ordinary income exposure.

Can the buyer and seller negotiate who pays the structural tax difference?

Yes. When a buyer requires an asset structure and the seller prefers a stock transaction, the parties often negotiate a tax gross-up in which the buyer pays an additional amount to compensate the seller for the incremental tax cost of depreciation recapture and ordinary income exposure. The gross-up is calculated by modeling the seller’s effective ordinary income rate on recaptured assets versus the capital gains rate on the same proceeds in a stock sale. A qualified business appraiser and tax advisor working together can produce a gross-up schedule both parties can use in negotiations.

Does deal structure affect the purchase price allocation after closing?

Yes. In an asset sale, the IRC 1060 allocation determines the tax character of the seller’s gain on each asset class and the buyer’s new depreciation schedule. After closing, the buyer also completes an ASC 805 purchase price allocation for financial reporting, recognizing acquired intangibles and goodwill at acquisition-date fair values. In a stock sale, no IRC 1060 allocation is required, but ASC 805 still applies for financial reporting. Both structures require the buyer to obtain a qualified appraisal for the ASC 805 allocation within the measurement period.

What is personal goodwill and how does it affect an asset sale?

Personal goodwill is the portion of a business’s value attributable to the individual owner’s relationships, skills, and reputation rather than to the enterprise itself. In an asset sale involving a C corporation, if personal goodwill can be separately documented and valued, the owner may sell it directly rather than routing it through the corporation, avoiding double taxation at the corporate level. The IRS recognizes personal goodwill in arm’s-length transactions when supported by a qualified appraisal that establishes its existence and quantifies it separately from enterprise goodwill.

How much does a business appraisal for an asset or stock sale cost?

A business appraisal from Sofer Advisors for an asset sale or stock sale transaction typically ranges from $7,500 to $25,000 depending on the company’s revenue, industry, and the complexity of the purchase price allocation required under IRC 1060 or ASC 805. Most standard transaction appraisals are completed in four to eight weeks from document receipt. For a fee estimate based on your specific transaction, contact Sofer Advisors.

How should sellers prepare before choosing a transaction structure?

Before accepting any offer, a seller should obtain an independent business appraisal to establish fair market value, engage a tax advisor to model after-tax proceeds under both asset and stock structures, and consult a business attorney about which contracts, permits, and licenses require third-party consent in an asset sale. Understanding the structural consequences before signing a letter of intent gives the seller the information needed to compare offers on a net after-tax basis rather than a gross price comparison. David Hern CPA ABV ASA, founder of Sofer Advisors, advises business owners on valuation for both transaction structures throughout the pre-sale planning process.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

An asset sale and a stock sale represent two fundamentally different ways to transfer a business, each with distinct tax consequences for both sides. Asset sales require IRC 1060 purchase price allocation across seven asset classes, creating ordinary income exposure for the seller through depreciation recapture while providing the buyer a stepped-up basis and new depreciation rights. Stock sales generally provide capital gains treatment for individual sellers but deny the buyer a basis step-up and expose them to all inherited liabilities. The structural conflict between buyer and seller preferences is resolved through price negotiation, tax gross-ups, or a combination of representations and warranties insurance and price adjustment. Sofer Advisors provides independent business appraisals and purchase price allocation analysis for middle-market transactions in both structures, ensuring every valuation conclusion is credentialed, documented, and defensible.

What Should You Do Next?

If you are preparing to sell your business or evaluating an acquisition offer, the choice between an asset sale and a stock sale will materially affect your after-tax proceeds and the buyer’s post-close economics. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide independent business appraisals and purchase price allocation analysis for middle-market sellers and buyers navigating both transaction structures across all industries. Schedule your free consultation to understand what your business is worth and how deal structure affects your net proceeds.

People Also Read

- Purchase Price Allocation ASC 805 and IFRS 3: Complete Guide for Business Leaders

- Business Valuation for Mergers: Buy-Side vs Sell-Side

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}