Last Updated: April 2026

A stepped-up basis at death is the tax provision under Internal Revenue Code Section 1014 that resets the cost basis of an inherited asset to its fair market value on the date of the owner’s death, effectively eliminating federal capital gains tax on any appreciation that occurred during the decedent’s lifetime. For business owners, the step-up in basis is one of the most consequential estate planning provisions in the tax code: when a closely held business interest is inherited, the heir’s tax basis becomes the date-of-death fair market value, not the original owner’s acquisition cost, wiping out potentially decades of accumulated unrealized gain that would otherwise be taxable upon a future sale.

For business owners with significant equity in closely held companies, the value assigned to those business interests at death determines both the step-up in basis available to heirs and, if the estate exceeds the applicable exemption, the estate tax owed. Sofer Advisors, a nationally recognized business valuation firm headquartered in Atlanta, GA, provides IRS-compliant date-of-death appraisals that establish the defensible fair market value needed for estate tax filings, stepped-up basis calculations, and post-mortem planning under IRS Regulation §20.2031-1.

The rules governing what qualifies for a step-up, how it interacts with estate tax, and what documentation the IRS requires are not straightforward for business interests. A miscalculated or undocumented date-of-death value can expose heirs to IRS challenge, overstated estate tax liability, or an understated capital gains basis that triggers unnecessary tax on a future sale.

Key Takeaways

- Basis Reset at Death: Stepped-up basis resets an inherited asset’s cost basis to its fair market value on the date of death, eliminating capital gains tax on all pre-death appreciation under IRC §1014.

- Business Interest Impact: For closely held business interests, the step-up can eliminate decades of accumulated gain, but the correct fair market value must be established by a qualified appraisal to withstand IRS review.

- Estate Tax Interaction: If the estate exceeds the applicable exemption ($13.61 million per individual in 2024), estate tax is owed on the total estate value, but heirs still receive a stepped-up basis equal to that same fair market value.

- TCJA Sunset Impact: The estate tax exemption reverted from $13.61 million to approximately $7 million per individual on January 1, 2026 under the TCJA sunset, meaning business owners with estates between those two thresholds are now subject to federal estate tax where they previously owed none.

- IRS Documentation Standard: A qualified appraisal meeting IRS standards under Regulation §20.2031-1 is required to establish a defensible date-of-death fair market value for closely held business interests.

Each of these rules interacts directly with the structure and timing of an estate plan, and business owners with meaningful equity in closely held companies face the highest documentation and valuation stakes when a key owner passes away. The sections below examine each rule in detail so that owners and their advisors understand what is required and what is at risk.

What Is Stepped-Up Basis at Death?

Stepped-up basis at death is the tax law mechanism that adjusts the cost basis of an inherited asset upward (or, in rare cases, downward) to its fair market value as of the date of the decedent’s death. Before the step-up, the decedent may have held the asset for decades, with a cost basis reflecting what they originally paid. After the step-up, the heir’s basis is the current fair market value, erasing the entire history of appreciation for capital gains purposes. When the heir eventually sells the asset, capital gains tax is calculated only on appreciation above the date-of-death value, not the original purchase price.

The provision is codified in IRC §1014 and applies to assets included in the decedent’s taxable estate. The policy rationale is to avoid a double tax burden on inherited property: if an estate is large enough to owe estate tax, taxing the same appreciation again as capital gains when the heir sells creates an additional layer that Congress historically chose to eliminate. For business owners, understanding the difference between cost basis and fair market value is foundational to modeling the actual tax consequences of a business interest transferred at death.

How Does Step-Up in Basis Work?

Step-up in basis works by substituting the date-of-death fair market value for the decedent’s original cost basis at the moment of transfer. The heir acquires the asset as if they had purchased it at that fair market value on the date of death. If the heir sells immediately after inheriting, there is no capital gain because the sale price equals the stepped-up basis. If the heir holds the asset and it appreciates further before sale, capital gains tax applies only to the post-death appreciation, not to the gain accumulated during the decedent’s lifetime.

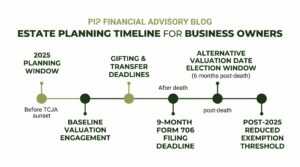

The IRS provides an alternative valuation date election under IRC §2032, which allows the executor to value the estate six months after the date of death if doing so would reduce both the gross estate value and the estate tax owed. This election can be strategically valuable if business values have declined since the owner’s death, though it applies uniformly to all estate assets, not selectively. The core steps in establishing and applying a stepped-up basis for a closely held business interest are as follows, each requiring documentation that can withstand IRS examination:

- Step 1 – Date of death: The decedent’s death triggers the step-up. The fair market value used for basis purposes is established as of this specific date, not when the estate is distributed.

- Step 2 – Qualified appraisal: A credentialed appraiser determines the fair market value of the closely held business interest as of the date of death under the IRS willing-buyer, willing-seller standard defined in Regulation §20.2031-1.

- Step 3 – Estate tax return (Form 706): If the estate exceeds the applicable exemption, the executor files Form 706 reporting the date-of-death fair market values. This return becomes part of the IRS record for the stepped-up basis.

- Step 4 – Distribution to heirs: Heirs receive the asset with a new cost basis equal to the reported date-of-death fair market value. This basis is their starting point for any future capital gains calculation.

- Step 5 – Basis tracking post-inheritance: If the heir later sells the asset, capital gains are calculated from the stepped-up basis to the sale price, not from the original owner’s acquisition cost.

Each step depends on the accuracy and defensibility of the date-of-death valuation, which is why a qualified appraisal is not optional for closely held business interests – it is the foundation of the entire stepped-up basis calculation.

What Assets Qualify for Stepped-Up Basis?

Not all assets transferred at death receive a step-up in basis. The general rule under IRC §1014 is that assets included in the decedent’s gross estate receive a stepped-up basis; assets transferred during the decedent’s lifetime as gifts use carryover basis instead. Understanding which assets qualify and which do not directly affects how an estate plan should be structured, particularly when the estate includes a mix of business interests, real property, retirement accounts, and gifted assets.

The distinction between stepped-up basis and carryover basis is one of the most consequential in estate planning. Carryover basis, which applies to lifetime gifts under IRC §1015, transfers the donor’s original cost basis to the recipient rather than resetting it to current fair market value. A business owner who gifts an interest during their lifetime transfers the accumulated gain along with the asset; an owner who retains the interest until death allows the step-up to eliminate that gain for their heirs.

| Stepped-Up Basis (Death Transfer) | Carryover Basis (Lifetime Gift) | |

|---|---|---|

| Governing code | IRC §1014 | IRC §1015 |

| Heir’s cost basis | Fair market value on date of death | Original owner’s cost basis (what they paid) |

| Pre-death capital gains | Eliminated – zero tax on pre-death appreciation | Preserved – heir inherits the donor’s gain |

| Example outcome | Business worth $5M at death; original cost $1M; heir sells at $5.5M; capital gain = $500K only | Business gifted at $5M FMV; donor’s cost $1M; recipient sells at $5.5M; capital gain = $4.5M |

| Estate tax exposure | Asset included in gross estate | Asset removed from gross estate (but gift tax may apply) |

| Best when | Preserving maximum heir benefit from low-basis assets | Reducing gross estate size when lifetime exemption is available |

What Is the Capital Gains Tax on Inherited Property?

Capital gains tax on inherited property is calculated based on the stepped-up basis, not the decedent’s original purchase price. When an heir sells an inherited asset, the taxable gain is the difference between the sale price and the date-of-death fair market value. If the sale occurs within one year of the date of death, the gain is classified as long-term regardless of the decedent’s holding period, per IRC §1223(11), which ensures heirs are not penalized with short-term rates simply because they sold quickly after inheriting.

According to the Tax Foundation (2024), the step-up in basis eliminates capital gains tax on an estimated $500 billion or more in unrealized gains transferred annually, making it one of the largest tax expenditures in the federal code. For business owners, the magnitude of unrealized gain in a closely held company can be substantial: a business acquired or built for $500,000 that is worth $8 million at the owner’s death would generate a $7.5 million long-term capital gain for heirs without the step-up. With the step-up, heirs can sell at $8 million with no capital gains tax liability on that history of appreciation.

Schedule your free consultation with Sofer Advisors to understand how a date-of-death valuation protects your heirs’ stepped-up basis, reduces estate tax exposure, and meets IRS documentation requirements for your closely held business interest. Discover The Sofer Difference.

How Does Stepped-Up Basis Affect Business Owners?

Stepped-up basis affects business owners differently than owners of publicly traded securities because the fair market value of a closely held business interest cannot be determined from a stock ticker. It must be established through a qualified appraisal that applies accepted valuation methodologies, including the income approach, market approach, and asset approach, under the IRS willing-buyer, willing-seller standard. Without a credentialed appraisal, heirs and executors face two risks: undervaluing the interest (reducing the step-up in basis and leaving capital gains exposure) or overvaluing it (increasing estate tax liability unnecessarily).

According to the IRS (2024), the basic exclusion amount for estate tax purposes was $13.61 million per individual for 2024 descendants under the Tax Cuts and Jobs Act (TCJA). That exemption reverted to approximately $7 million per individual on January 1, 2026 under the scheduled TCJA sunset. Business owners with estates between $7 million and $13.61 million who previously owed no estate tax now face a 40% federal estate tax on the excess, making the current planning environment materially different from even 18 months ago. Valuation firms including Kroll and Stout provide estate valuation services for large complex estates; for middle-market business owners, Sofer Advisors provides date-of-death appraisals with ABV and ASA credentialing that meet IRS and court standards.

According to AICPA Forensic and Valuation Services (2023), a properly prepared date-of-death appraisal for a closely held business interest must document the standard of value, valuation date, applicable discounts for lack of control or marketability, and the methodologies applied, all consistent with IRS Regulation §20.2031-1 and Revenue Ruling 59-60. Heirs who rely on an undocumented or non-compliant valuation face IRS challenges on both the estate tax return and the heir’s future capital gains calculation.

How Should Business Owners Plan for Step-Up Rules?

Planning for stepped-up basis requires a deliberate strategy that coordinates the timing of asset transfers, the use of the estate tax exemption, and the sourcing of a qualified date-of-death appraisal before the IRS filing deadline. For most estates, the executor must file Form 706 within nine months of the date of death (with a possible six-month extension). The appraisal supporting the business interest valuation must be completed and attached to that return, making it effectively one of the first post-death action items for an estate with closely held business interests.

The TCJA exemption reverted on January 1, 2026, and business owners who did not complete pre-sunset transfers are now subject to estate tax under the lower threshold. Planning using gifting strategies, grantor retained annuity trusts (GRATs), family limited partnerships (FLPs), or other techniques that shift value out of the estate while preserving cash flow can still reduce future estate tax exposure, though each strategy has its own cost basis and documentation implications and should be modeled against the current threshold, not the prior one.

Key planning steps for business owners to address now:

- Obtain a baseline valuation: A current-date appraisal of the closely held business interest establishes value for gifting, FLP planning, and estate tax projections under the current post-TCJA threshold.

- Model the current threshold exposure: Compare the current estate value to the post-TCJA approximately $7 million threshold to identify gap exposure now that the higher $13.61 million exemption has expired.

- Review asset transfer strategies: Decide which assets should be retained until death (for the step-up benefit) and which should be gifted now (to reduce estate size) based on basis, appreciation potential, and the owner’s liquidity needs.

- Engage an estate attorney and valuation firm together: The interaction between step-up rules, estate tax, gift tax, and business continuity planning requires coordinated advice, not a single-discipline review.

Business owners who do not plan for the stepped-up basis rules are not simply leaving a tax planning opportunity unused – they are shifting an avoidable capital gains liability onto their heirs, who may not have the same resources or flexibility to manage it.

Frequently Asked Questions

What is stepped-up basis at death in simple terms?

Stepped-up basis at death means that when you inherit an asset, your tax starting point is its current value on the date the original owner died, not what they originally paid for it. If a parent bought a business for $1 million and it was worth $6 million when they died, the heir’s cost basis is $6 million. If the heir sells for $6 million shortly after, no capital gains tax is owed on the $5 million of appreciation that occurred during the parent’s lifetime.

How does step-up in basis work for inherited business interests?

For inherited business interests, the step-up in basis works the same way as for other assets, but establishing the date-of-death value requires a qualified appraisal rather than a market quote. The appraiser determines fair market value using the income, market, and asset approaches under IRS standards, applies any appropriate discounts for lack of control or marketability, and documents the conclusion in a report that can withstand IRS examination. The resulting value becomes the heir’s cost basis for all future capital gains calculations.

Does stepped-up basis apply to all inherited assets?

Stepped-up basis applies to most assets included in the decedent’s gross estate under IRC §1014, including real estate, closely held business interests, investment accounts, and tangible personal property. It does not apply to assets transferred as lifetime gifts, which use carryover basis under IRC §1015. Retirement accounts such as IRAs and 401(k)s do not receive a step-up in basis because they are subject to income tax upon distribution, not capital gains tax. Tax-deferred accounts require separate planning.

What was the estate tax exemption for 2024 and 2025?

The estate tax basic exclusion amount was $13.61 million per individual for 2024 decedents, or approximately $27.22 million per married couple using the portability election. Estates below this threshold owed no federal estate tax, and heirs of those estates still received a stepped-up basis on all qualifying assets. Estates above the threshold owed a 40% federal estate tax on the excess, though heirs still received a stepped-up basis equal to the reported date-of-death fair market values used on Form 706.

What happened to the estate tax exemption in 2026?

The Tax Cuts and Jobs Act provisions expired on January 1, 2026, and the estate tax basic exclusion amount reverted to approximately $7 million per individual, adjusted for inflation from its pre-TCJA level. This change cut the exemption roughly in half. Business owners with estates between $7 million and $13.61 million who previously owed no federal estate tax now face a 40% tax on the excess above the lower threshold. Planning strategies that shift value out of the taxable estate remain the primary mitigation tools available.

Why does stepped-up basis matter for closely held business owners specifically?

Closely held business owners are more affected by stepped-up basis rules than owners of publicly traded assets because their business interest typically represents a large portion of their total estate value, is illiquid, and cannot be sold gradually to manage tax exposure. A business built over 30 years may have a very low original cost basis but a very high date-of-death value. Without the step-up, heirs would owe capital gains tax on the full difference, often a multimillion-dollar liability, before they could even access the proceeds from a sale.

What is the IRS standard for valuing a business interest at death?

The IRS requires that closely held business interests be valued using the fair market value standard defined in Regulation §20.2031-1: the price at which the property would change hands between a willing buyer and a willing seller, neither under any compulsion to buy or sell, both having reasonable knowledge of the relevant facts. The appraisal must comply with Revenue Ruling 59-60, which specifies the factors to be considered, including the nature of the business, earning capacity, dividend-paying capacity, goodwill, and recent sales of similar interests.

Can the IRS challenge a stepped-up basis reported on Form 706?

Yes. The IRS can challenge the valuation of closely held business interests reported on Form 706 and assert a higher value, which increases estate tax owed, or a different value that affects the heir’s stepped-up basis. IRS examiners compare the reported valuation to independent analysis, comparable transaction data, and the business’s own financial statements. A qualified appraisal prepared by a credentialed professional under IRS standards is the primary defense against these challenges, which is why the documentation quality matters as much as the concluded value.

How much does an estate tax valuation from Sofer Advisors cost?

An estate tax valuation from Sofer Advisors typically ranges from $7,500 to $25,000 depending on the complexity of the business interest, the number of entities involved, and the documentation required for IRS Form 706. Engagements are generally completed in four to eight weeks from document receipt. For a fee estimate based on your estate’s specific facts, contact Sofer Advisors.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Valuation Timing: Why the Right Date Changes Everything

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

Executive Summary

Stepped-up basis at death resets the cost basis of an inherited asset to its fair market value on the date of the owner’s death, eliminating capital gains tax on all pre-death appreciation under IRC §1014. For business owners, the provision is particularly valuable because closely held business interests often carry decades of accumulated unrealized gain that would otherwise be taxable when heirs sell. The estate tax exemption reverted from $13.61 million to approximately $7 million per individual on January 1, 2026, meaning business owners with estates in that range now face federal estate tax where they previously owed none. Sofer Advisors provides qualified, IRS-compliant date-of-death appraisals that establish the defensible fair market value required for estate tax returns, stepped-up basis documentation, and post-mortem planning under Regulation §20.2031-1.

What Should You Do Next?

If you own a closely held business and have not yet addressed the impact of the January 2026 TCJA exemption reversion or the date-of-death valuation requirements for your estate plan, the revised threshold is now in effect and planning under the lower exemption is the immediate priority. David Hern CPA ABV ASA, founder of Sofer Advisors, and his team of 14 credentialed valuation professionals provide IRS-compliant date-of-death appraisals, estate tax valuations, and gift tax valuations that protect heirs’ stepped-up basis, minimize estate tax liability, and withstand IRS examination. Schedule your free consultation to understand how a qualified appraisal fits into your estate plan and what the TCJA sunset means for your specific situation.

People Also Read

- Cost Basis vs Fair Market Value: Key Differences Explained

- Fair Market Value for Estate Tax: What Executors Need

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}