Last Updated: June 2026

This article is written for business owners, attorneys, and financial professionals in commercial disputes. After reading it, you will understand how experts build a damages model, what courts accept as proof, and which mistakes destroy credibility at trial.

A lost profits damages calculation is the process of measuring the income a business or individual would have earned if a wrongful act had not occurred. It matters because courts require a credible, evidence-based number – not a guess – to award money to an injured party. Applied in breach of contract, tortious interference, and fraud cases, this calculation forms the financial core of many commercial disputes.

When a business suffers harm from another party’s conduct, the gap between actual earnings and projected earnings can be worth millions of dollars. Sofer Advisors, headquartered in Atlanta, GA, provides lost profits analysis for commercial litigation across the United States. Getting this number right protects your recovery. Getting it wrong can sink an otherwise strong case before it reaches a jury.

Key Takeaways

- But-For Revenue Baseline – Every lost profits calculation projects what the business would have earned without the wrongful act, typically using 3-5 years of historical data.

- Variable vs. Fixed Cost Offset – Only incremental (variable) costs are deducted; fixed costs already incurred do not reduce the damages award.

- Reasonable Certainty Standard – Federal and most state courts require lost profits to be proven to “reasonable certainty” – above mere possibility but below absolute proof.

- Expert Witness Qualification – Damages experts holding ABV or ASA credentials carry more weight with juries than unqualified in-house witnesses.

- Mitigation Obligation – The injured party must show it took reasonable steps to reduce losses; failure to mitigate can reduce the final award by 20-100%.

- Discount Rate Application – Future lost profits must be discounted to present value at a rate typically ranging from 8-15% for small to mid-size businesses.

The sections below examine each component in detail.

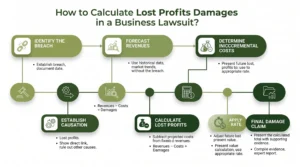

What Is the But-For Method?

The “but-for” method is the most common framework courts use to calculate lost profits. It asks one question: what would the business have earned but for the defendant’s wrongful conduct? The expert builds two financial scenarios – one showing actual performance and one showing projected performance without the harmful event. The difference is the claimed lost profits figure.

To build the but-for scenario, the expert first establishes a baseline revenue trend using historical data. The baseline typically covers three to five years before the harmful event. Industry growth rates, signed contracts, customer pipeline data, and comparable company performance all feed into the projection. The more concrete the evidence, the harder it is for opposing counsel to attack.

Courts treat the but-for method as the standard starting point for economic damages. A well-built model documents sources for each input and shows sensitivity ranges. For example, it shows how the damages figure changes if revenue growth was 5% instead of 8%. That rigor separates defensible models from ones that collapse on cross-examination.

Why Does the Reasonable Certainty Standard Matter?

The reasonable certainty standard is the legal threshold that determines whether a damages claim survives in court. It sits above mere speculation and below absolute proof. Courts accept uncertainty about the amount of damages while requiring certainty about the fact of harm.

New businesses face a harder challenge under this standard. Without historical revenue data, projections rest on market surveys and comparable businesses. Established businesses have a natural advantage because their baseline is well-documented.

The AICPA Forensic and Valuation Services section publishes guidance on applying this standard in forensic engagements. Experts who follow AICPA standards and document their methodology are better positioned to survive Daubert challenges. State courts vary in how strictly they apply this standard. Knowing the jurisdiction’s rules before building the model saves time and cost.

How Do You Calculate But-For Revenue?

Calculating but-for revenue starts with the injured business’s own financial records. Tax returns, audited financial statements, management accounts, and customer contracts are the primary inputs. The expert extracts a trend line. This is often a compound annual growth rate or a regression of historical revenue against time and industry variables.

The damages period runs from the date of the harmful act to either the date the business recovered or the end of a reasonable recovery horizon. In breach of contract cases, it often matches the remaining contract term. In tortious interference, it may run three to seven years or longer.

Three factors most commonly affect the revenue projection:

- Signed contracts or purchase orders that were interrupted by the harmful act

- Historical growth rates from the business’s own financial records over the prior three to five years

- Industry data from comparable companies or market research showing expected sector growth

Each input should come with documented source citations. Unexplained assumptions invite cross-examination attacks and reduce the weight a jury gives the damages figure. Once the but-for revenue figure is established, the expert deducts only variable costs. These are costs the business would have actually spent to earn the projected revenue. The result is net lost profits.

What Evidence Do Courts Require for Lost Profits?

Courts look at four categories of evidence when evaluating a lost profits claim. Financial records form the first category. Tax returns, bank statements, and audited financials establish the baseline. Courts treat audited statements as most reliable because a third-party CPA verified them.

Contracts and business records make up the second category. Signed agreements that were broken show directly what revenue the business expected. Emails and customer communications can support projections even without a signed contract.

Expert testimony is the third category. A qualified damages expert holding ABV or ASA credentials applies an accepted methodology, documents assumptions, and presents findings clearly. Methodology transparency is what survives the Daubert review.

Industry and market data form the fourth category. Trade association reports, Census Bureau data, and industry databases provide corroboration. Courts accept this data when a business cannot rely solely on its own records and the expert explains why the benchmark applies.

How Do You Deduct Costs From Lost Revenue?

Deducting the right costs is where many damages models fail. The rule is straightforward: subtract only the costs the business would have incurred to generate the lost revenue. Classifying costs as variable or fixed requires judgment and documentation.

Variable costs typically include direct labor, raw materials, sales commissions, and shipping. Fixed costs are overhead that continues regardless of revenue volume. They do not reduce the award because the business already paid them without getting the offsetting revenue.

A common table used in damages reports compares cost types:

| Cost Category | Fixed or Variable | Deductible From Lost Profits |

|---|---|---|

| Direct labor (incremental) | Variable | Yes |

| Raw materials | Variable | Yes |

| Sales commissions | Variable | Yes |

| Rent and facilities | Fixed | No |

| Base salaries (existing staff) | Fixed | No |

| Administrative overhead | Fixed | No |

| Equipment depreciation | Fixed | No |

| New staff hired for lost work | Variable | Yes |

A service firm with mostly fixed costs will show higher net lost profits than a manufacturer with high variable input costs for the same revenue loss. The expert must analyze each cost line in the specific business’s financial statements rather than applying a generic rule. Documenting classification decisions early reduces the risk of a successful rebuttal at trial.

What Mistakes Reduce a Lost Profits Award?

Several recurring errors weaken damages claims and reduce final awards.

The most damaging error is using speculative assumptions without supporting data. Courts and opposing experts identify unsupported growth rates immediately. Every assumption needs a documented source – whether the business’s own historical trend, a signed contract, or an industry benchmark.

A second error is failing to address mitigation. The injured party has a legal duty to reduce its losses after the harm. If it did nothing, the court may reduce the award. A third error is including fixed costs in the deductions, which overstates the net loss.

A Heart of a Teacher approach matters: present the calculation in plain, clear terms that a non-financial juror can follow. That increases the probability of a full award. The Sofer Difference is a four-phase process of Discovery, Diligence, Analysis, and Delivery. It drives pre-trial preparation at Sofer Advisors, producing reports that hold up under cross-examination and present clearly to judges and juries.

The questions below address the most common practical issues before engaging an expert.

Frequently Asked Questions

What is a lost profits damages calculation?

A lost profits damages calculation measures the income a business lost because of another party’s wrongful conduct. The expert projects what revenue and profit would have been earned but for the harmful act, then subtracts actual results. Courts use this figure to award compensatory damages in breach of contract, fraud, and tortious interference cases.

How much does a lost profits analysis from Sofer Advisors cost?

A lost profits analysis typically ranges from $7,500 to $25,000 depending on case complexity, damages period length, and document volume. Engagements involving multiple business units may run higher. Most standard engagements complete in four to eight weeks. Rush engagements are available at a 25-50% premium. Schedule a free consultation to receive a scoped estimate for your case.

How long does it take to prepare a lost profits report?

Most lost profits reports take four to eight weeks once the expert receives complete financial records. Complex cases can run ten to fourteen weeks. Expedited timelines are available but require complete document production upfront. The largest time variable is how quickly the client provides tax returns, financials, and contract documentation.

What is the difference between lost profits and lost business value?

Lost profits measure the specific income stream harmed during a defined damages period. Lost business value measures the reduction in the overall worth of the business caused by the wrongful act. Courts treat these as distinct theories. A plaintiff may claim both, but careful coordination is needed to avoid double-counting damages.

What is the reasonable certainty standard?

The reasonable certainty standard requires that the fact of harm be proven with certainty. The amount need only be estimated with reasonable confidence. Courts allow approximation as long as the methodology is sound and assumptions are grounded in real evidence. This standard prevents speculative claims while not denying recovery when exact figures are impossible to determine.

Does the injured party have to prove it tried to reduce losses?

Yes. The duty to mitigate requires the injured party to take reasonable steps to reduce losses after the harmful act. Courts will reduce a damages award if the plaintiff made no effort to replace lost revenue or cut costs. The damages expert should address mitigation directly. The report should document what the plaintiff did or explain why further mitigation was not commercially reasonable.

Can a new business recover lost profits?

A new business faces a higher burden of proof because it lacks historical financial data. Courts have allowed recovery when the plaintiff shows signed contracts that were prevented, business plans with market support, or comparable company data. The key is credible evidence of expected revenue, not speculation. Several states bar recovery entirely under a strict new business rule, so jurisdiction matters significantly.

How do courts evaluate damages expert testimony?

Federal courts use the Daubert standard, which requires the judge to screen out unreliable methodology before the expert testifies. The judge considers whether the methodology is accepted in the field and whether the expert applied it correctly. Experts with ABV or ASA credentials who follow AICPA forensic standards are more likely to pass the Daubert review. Those relying on undocumented methods rarely do.

What financial records does an expert need to start?

An expert typically needs three to five years of tax returns or audited financials, monthly profit and loss statements, and customer-level revenue data. Cost records broken down by fixed and variable categories are also required. Banking records and CRM data help. The more complete the records provided upfront, the faster the engagement proceeds.

How is a lost profits calculation different from a business valuation?

A business valuation determines the overall worth of a company at a point in time using the income, market, or asset approach. A lost profits calculation measures the specific income harm caused by a wrongful act over a defined period. Both use discounted cash flow concepts but serve different purposes. A valuation answers “what is the business worth?” A lost profits calculation answers “how much income did the act take away?”

Related Case Studies

- Expert Witness Business Valuation Georgia What Attorneys Need To Know

- How Do You Determine What A Business Is Worth Complete Guide

- Shareholder Dispute Valuation Atlanta Resolving Georgia Business Partner Conflicts

Executive Summary

Calculating lost profits requires a credible but-for revenue projection, accurate cost classification, and a defensible discount rate. Courts demand the reasonable certainty standard: the fact of harm proven firmly, the amount estimated with sound methodology. Variable costs reduce the award; fixed costs do not. Mitigation must be addressed directly. Expert witnesses with ABV or ASA credentials grounded in AICPA forensic standards carry the most weight at trial. Every assumption needs a documented source.

What Should You Do Next?

If you face a commercial dispute involving lost income, act quickly – damages models take time to build, and late-stage expert retention limits the analysis. Gather three to five years of tax returns, monthly profit and loss statements, and copies of any contracts at issue. Share that package with a qualified damages expert as early in the litigation as possible.

David Hern CPA ABV ASA, founder of Sofer Advisors, has served as an expert witness in 11+ cases across multiple jurisdictions. Schedule a consultation to discuss your lost profits claim and get a scoped estimate.

People Also Read

- Expert Witness Business Valuation Georgia What Attorneys Need To Know

- Shareholder Dispute Valuation Atlanta Resolving Georgia Business Partner Conflicts

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm based in Atlanta, GA. David holds the Accredited Senior Appraiser (ASA) and Accredited in Business Valuation (ABV) credentials, recognized by the IRS, SEC, and FINRA, plus the Certified Exit Planning Advisor (CEPA) designation. He has served as an expert witness in 11+ cases across multiple jurisdictions. The firm holds 180+ five-star Google reviews.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}