Last Updated: June 2026

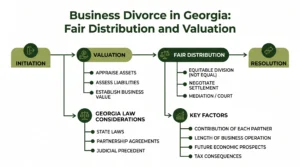

A Georgia divorce business valuation determines what a privately held business interest is worth so a court can divide marital property under the state’s fair distribution rule, which splits property fairly but not necessarily 50/50. The first question is whether the business interest is marital property, separate property, or a mix of both. The second is how to value whatever portion is subject to division. Both questions require expert analysis, and the answers directly determine how much one spouse owes the other.

Georgia courts have developed a body of case law on business valuation in divorce. It differs from the standards used in M&A deals. The standard of value is typically fair market value. But Georgia courts have also accepted investment value in specific contexts. More importantly, Georgia distinguishes between enterprise goodwill, which is marital and divisible, and personal goodwill, which belongs to the individual and is generally excluded from the marital estate. That distinction alone can shift a business valuation by hundreds of thousands of dollars. Courts examine this distinction closely. Sofer Advisors helps owners and their advisors work through exactly these questions and turn the analysis into a defensible business valuation they can act on.

The following takeaways summarize the key valuation and transaction factors covered in this guide.

Key Takeaways

- Georgia Uses Fair Distribution – Georgia uses fair distribution, not equal division. The court allocates marital property based on fairness, not a 50/50 formula.

- Business Interests Grown Marriage – Business interests grown during the marriage are generally marital property. Pre-marital businesses may be partly or fully separate property depending on active vs. passive appreciation.

- Personal Goodwill Value Tied – Personal goodwill – the value tied to the owner’s individual reputation, relationships, and skills – is generally not divisible in Georgia divorce proceedings.

- Enterprise Goodwill Value Would – Enterprise goodwill – value that would survive the owner’s departure – is marital property subject to division.

Each of these factors is examined in depth in the sections that follow.

How Does Georgia Handle Business Valuation in Divorce?

Georgia follows the fair distribution standard under O.C.G.A. § 19-3-9. The court divides marital property in a manner that is fair. It considers all relevant factors. Those factors include the duration of the marriage and each spouse’s contributions. They also include the future financial circumstances of each party and any dissipation of marital assets.

The starting point is classifying the business interest. Property brought into the marriage is separate property. Property received by gift or inheritance during the marriage is also separate property. It is not subject to division. A business founded before the marriage is separate property. But only to the extent its value has not increased due to marital effort. The increase in value, the “active appreciation”, is marital. Passive appreciation from market forces remains separate. This applies when no marital effort drove the growth.

This distinction creates real complexity. Suppose a spouse owned a landscaping company worth $200,000 at marriage. By divorce, it’s worth $1.2M. If $800,000 of that growth came from the owning spouse’s efforts, building the customer base, adding employees, developing service lines, that $800,000 is marital property. If $200,000 grew simply because the industry inflated, that portion may be separate. A credentialed valuator is needed to separate these components. The work requires historical financial records and industry benchmarking. Expert judgment is also needed.

For businesses founded during the marriage, the analysis is more direct. The entire value as of the valuation date is presumptively marital. The owning spouse can rebut that presumption. They must show that specific value components are tied to pre-marital capital contributions.

Engagements like this are performed under the AICPA Statement on Standards for Forensic Services, which sets enforceable standards for litigation and investigative work.

What Is Personal Goodwill vs. Enterprise Goodwill in Georgia?

The personal goodwill distinction is one of the most litigated concepts in Georgia business divorce. Georgia courts have held that personal goodwill is not marital property. It cannot be transferred independent of the individual who created it.

Personal goodwill includes the owner’s personal reputation in the community. It includes their professional licenses and credentials. It also includes personal relationships with clients who would follow them if they left the business. Any value that depends on the owner’s continued active role is personal goodwill. In a small professional services firm, a law firm, medical practice, or consulting business, personal goodwill can easily represent 60%–80% of total goodwill value. That is a very large share of total business value.

Enterprise goodwill is the value that would survive the owner’s departure. It includes established systems and processes. It includes brand recognition independent of any individual. It also includes long-term contracts, trained workforce, geographic footprint, and institutional client relationships that belong to the entity. Enterprise goodwill is marital property and is subject to fair distribution.

Valuing personal vs. enterprise goodwill requires judgment and a clear method. Common approaches include the excess earnings method. This method separates the return on tangible assets from the goodwill premium. It then allocates that premium between personal and enterprise components. Market comparisons of absentee-owned versus owner-operated businesses are also used. Each method has strengths and limits.

In Georgia divorce cases, this allocation is often contested. The owning spouse wants to maximize the personal goodwill allocation. This reduces the divisible marital estate. The non-owning spouse wants to minimize it. Both sides typically engage separate experts. Courts decide based on the credibility of the methods presented.

What Standard of Value Do Georgia Courts Use?

Georgia courts generally apply fair market value. This is the price at which a willing buyer would purchase the business from a willing seller. Both parties are assumed to have reasonable knowledge of the facts. Neither is compelled to transact. This standard is the same used in M&A deals and in federal tax matters.

Fair market value in a divorce context has nuances. Unlike a true M&A sale, the “market” for a small business interest held by one spouse is typically not an active market. Discounts for lack of marketability and lack of control are standard in minority interest valuations for tax purposes. But they are applied on their own terms in Georgia divorce. Some courts apply them. Others have refused. Their concern is that minority discounts would allow a majority owner to reduce the marital estate artificially.

Investment value, the value to a specific buyer given their particular strategic advantages, is occasionally argued in Georgia divorce. Courts have accepted investment value arguments in specific fact patterns. But it is not the default standard.

The date of valuation is a separate and often contested issue. Georgia courts have applied several dates: the date of separation, the date of filing for divorce, and the date of trial. The choice can matter greatly if business value changed a lot during the case. The safer approach is to set the valuation date early in litigation. Update the analysis if the value changes a lot before trial.

What Business Assets Are Untouchable in a Georgia Divorce?

Not all business-related assets are divisible. Several categories are typically protected from fair distribution.

- Pre-marital equity. The portion of business value tied to the owner’s contribution before the marriage is separate property. The burden of tracing falls on the owning spouse. Commingling of assets can destroy the separate property claim.

- Inherited business interests. If a spouse inherited a family business or received a business interest as a gift during the marriage, that interest is separate property. But active appreciation may convert a portion to marital property.

- Personal goodwill. The value component tied to the individual’s personal relationships, reputation, and skills is not marital property under Georgia case law.

- Passive appreciation of separate property. If a pre-marital business increased in value solely due to market forces, without the active contribution of either spouse, that appreciation remains separate.

What is not protected: operating profits and retained earnings built during the marriage, enterprise goodwill built during the marriage, appreciation tied directly to marital effort, and business assets purchased with marital funds.

David Hern CPA ABV ASA, founder of Sofer Advisors, brings a Heart of a Teacher to every engagement – translating complex valuation methodology into clear, actionable guidance that clients can act on before and after the report is delivered. With 15+ years of valuation experience, 11+ expert witness cases across multiple jurisdictions, and 180+ five-star Google reviews, David built Sofer Advisors into an Inc. 5000-recognized firm. The Sofer Difference is a four-phase process of Discovery, Diligence, Analysis, and Delivery that ensures every conclusion is defensible, documented, and tied to the specific facts of the business.

While national firms like Stout and Kroll serve large enterprise clients, Sofer Advisors specializes in middle-market businesses that require personalized attention, direct access to credentialed professionals, and a next business day response policy.

How Much Is a $500,000 Revenue Business Worth in a Georgia Divorce?

A business with $500,000 in annual revenue has a value that depends on its profitability, industry, growth path, and the personal vs. enterprise goodwill breakdown. Revenue is not a valuation metric, earnings are.

| Scenario | Revenue | EBITDA Margin | EBITDA | Multiple | Enterprise Value |

|---|---|---|---|---|---|

| Professional services (solo) | $500K | 30% | $150K | 3x | $450K |

| Trade business (crew-based) | $500K | 20% | $100K | 4x | $400K |

| Recurring-contract business | $500K | 25% | $125K | 5x | $625K |

After the personal goodwill allocation, the divisible marital estate will be smaller. For a solo consulting practice, personal goodwill may represent 70% of total value. For a crew-based trade business with trained employees and recurring contracts, enterprise goodwill may dominate. The non-owning spouse’s share depends on the court’s analysis of contribution, need, and circumstances.

Should You Use a Neutral Expert or Dueling Experts?

In Georgia divorce litigation, both sides typically retain separate business valuation experts who present competing analyses at trial. Each expert’s report is disclosed to opposing counsel. The experts are cross-examined on their method.

The practical problem with dueling experts is cost. Each engagement typically runs $5,000–$30,000 or more. Courts sometimes split the difference between two reasonable valuations rather than adopting one wholesale. This creates incentives for settlement.

A neutral expert, appointed by agreement of both parties or by the court, can reduce costs and speed up resolution. Courts generally give significant weight to neutral expert opinions. The risk is that neither party controls the outcome of the analysis.

In high-conflict divorce cases with complex business structures or disputed personal goodwill allocation, the adversarial expert model is often necessary. The stakes are too high to rely on a single expert.

The questions below address the most common issues attorneys raise before engaging a qualified appraiser for a georgia divorce business valuation engagement.

Frequently Asked Questions

How do you determine the value of a business in a divorce?

A credentialed business appraiser applies one or more of three approaches: income (capitalized or discounted earnings), market (comparable company deals), and asset-based (net asset value). In Georgia divorce, the valuation must also distinguish between marital and separate property components and between personal and enterprise goodwill.

What is fair distribution in Georgia?

Georgia divides marital property fairly, meaning equitably, not necessarily equally. Courts consider the length of the marriage, each spouse’s contributions, financial circumstances, and any dissipation of marital assets. A 60/40 split is common; 50/50 is possible but not guaranteed.

Is a business started before marriage separate property in Georgia?

Yes, but only to the extent its value hasn’t increased through marital effort. Active appreciation, growth tied to either spouse’s contributions during the marriage, is marital property subject to fair distribution. Passive appreciation (market factors alone) generally remains separate.

How much is a business worth with $500,000 in sales?

Revenue alone doesn’t determine value. A $500K revenue business is worth whatever its normalized earnings support, typically 2x–6x EBITDA depending on industry, margins, and risk profile. At 20% margins and a 4x multiple, that’s roughly $400,000 in enterprise value before personal goodwill adjustments.

What is personal goodwill and why does it matter in Georgia divorce?

Personal goodwill is the value tied to an individual owner’s reputation, relationships, and skills. It cannot be transferred without the person. Georgia courts exclude personal goodwill from the marital estate. This can reduce the divisible value of professional service businesses.

What assets are untouchable during a Georgia divorce?

Separate property (pre-marital assets, gifts, and inheritances) is generally not subject to fair distribution. Personal goodwill is excluded from the marital estate. Passive appreciation of separate property that occurred without marital effort is also typically protected.

How long does a business valuation take in a Georgia divorce case?

A thorough business valuation for divorce typically takes 4–12 weeks. The timeline depends on business size, complexity, and the availability of financial records. Contested cases with extensive discovery may take longer.

Should a business owner get their own valuation expert in a divorce?

Yes. The non-owning spouse will typically retain an expert who has an incentive to maximize value. The owning spouse needs a credentialed expert to present a rigorous alternative analysis. That expert can also identify legitimate adjustments, including personal goodwill, adjustment of owner pay, and applicable discounts.

Can a business be sold to pay a divorce settlement in Georgia?

Courts can order a buyout of one spouse’s interest as part of the fair distribution award. Forced liquidation of an operating business is rare and a last resort. More commonly, the owning spouse buys out the non-owning spouse using cash, other marital assets, or structured payments.

How does owner pay affect business value in a divorce?

Above-market owner pay reduces reported earnings and, so, income-based valuations. Experts on both sides will adjust pay, replacing the actual owner salary with a market-rate salary, to produce defensible normalized earnings. This adjustment can increase or decrease the reported value.

Related Case Studies

- Divorce Business Valuation Georgia What Business Owners Need To Know

- Expert Witness Business Valuation Georgia What Attorneys Need To Know

- Personal Goodwill Vs Enterprise Goodwill Tax Divorce Guide

Executive Summary

- Georgia’s fair distribution standard means courts divide marital property fairly, not equally – the analysis is highly fact-specific.

- Business interests are marital property to the extent they reflect active appreciation during the marriage. Pre-marital equity and passive appreciation may be excluded.

- Georgia’s personal goodwill doctrine can reduce the divisible value of owner-dependent businesses – a critical issue in professional practices and small closely-held companies.

- A certified business valuation by a credentialed appraiser is essential for any business owner facing divorce litigation in Georgia.

What Should You Do Next?

If you are a business owner, attorney, or CPA involved in a Georgia divorce where a business interest is in dispute, a certified valuation is the foundation of any credible negotiating or litigation position. David Hern CPA ABV ASA, founder of Sofer Advisors, holds dual ASA and ABV credentials recognized by the IRS, SEC, and FINRA, with 15+ years of valuation experience and 180+ five-star Google reviews. Schedule a consultation to discuss your business valuation needs.

People Also Read

- Divorce Business Valuation Georgia What Business Owners Need To Know

- Small Business Valuation Georgia What Every Owner Should Know

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com/about-us/ or schedule a consultation at soferadvisors.com/contact-us/.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}