Last Updated: April 2026

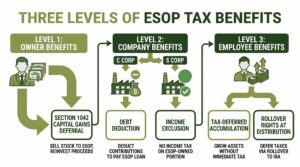

ESOP tax benefits operate at three levels: the selling owner receives capital gains treatment at the time of sale, the company gains ongoing income tax advantages through the plan structure, and employees accumulate tax-deferred ownership stakes without paying income tax on share allocations until distribution. According to the NCEO (2024), approximately 6,500 ESOP-owned companies covering nearly 14 million employee-owners operate in the United States, with tax advantage as the primary driver of adoption for both C and S corporation owners.

At Sofer Advisors, we provide independent ESOP valuations, including the formal share appraisal trustees require to confirm the transaction price does not exceed fair market value. A credentialed valuation is a prerequisite for each.

Business owners evaluating an ESOP need to understand how the tax benefits apply at each level, what conditions must be met, and where each benefit’s limits lie. The sections below walk through each in the order the IRS and plan counsel address them.

Key Takeaways

- C Corporation Owner Benefit – a C corp seller who transfers at least 30 percent of stock to an ESOP qualifies for capital gains deferral under IRC Section 1042 by reinvesting proceeds in qualified replacement property

- S Corporation Company Benefit – income attributable to ESOP-owned S corporation shares is exempt from federal income tax; a 100 percent ESOP-owned S corp pays no federal income tax on those earnings

- Employee Benefit – employees receive share allocations tax-deferred with no income tax owed until distribution and may roll proceeds into an IRA at retirement

- Employer Deduction – the company deducts ESOP contributions used to repay acquisition debt, converting loan repayments into deductible expense

- Valuation Requirement – every ESOP tax benefit depends on a qualified independent appraisal confirming the trustee paid no more than fair market value

Each benefit carries specific IRS and ERISA conditions that determine whether it applies and remains in force. The sections below examine how each works and where the limits are.

What Are ESOP Tax Benefits?

ESOP tax benefits are federally authorized incentives that reduce the income tax cost of selling a business to an employee ownership plan, operating the plan inside an S corporation, and accumulating retirement assets inside the ESOP trust. The benefits vary by corporate structure and by whether the beneficiary is the selling owner, the company, or the participating employee. No single benefit applies to all three parties simultaneously, which is why ESOP tax planning requires separate analysis at each level.

The three categories of ESOP tax benefit are:

- Owner-Level Benefits – the Section 1042 capital gains deferral for C corporation sellers who reinvest proceeds in qualified replacement property after selling at least 30 percent of stock to an ESOP

- Company-Level Benefits – the S corporation income tax exclusion on earnings attributable to ESOP-owned shares and the C corporation deduction on contributions used to service acquisition debt

- Employee-Level Benefits – tax-deferred accumulation of company shares inside the ESOP trust, no income tax on allocations until distribution, and IRA rollover rights at retirement

Which benefits apply to your business depends on corporate structure, the percentage of equity transferred, and how the transaction is funded. An S corporation owner who expects the Section 1042 rollover will be disappointed; that benefit is restricted to C corporation shareholders. An independent business valuation at the feasibility stage confirms not only the transaction price but also which tax benefit category is accessible based on the existing ownership and corporate structure.

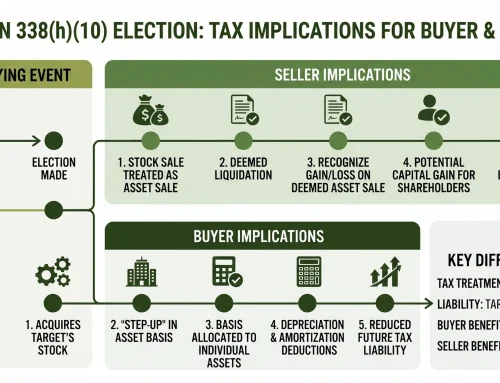

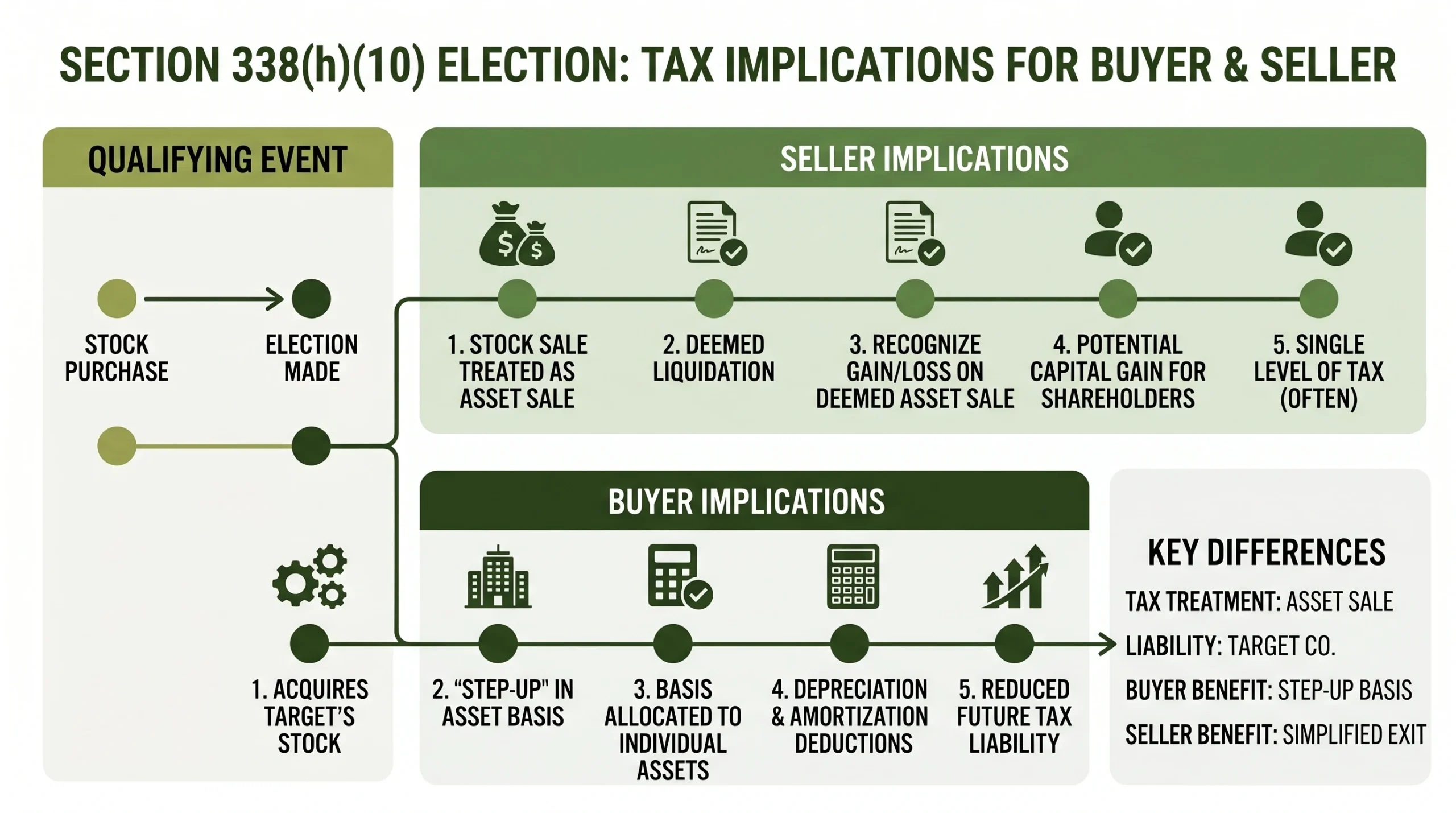

How Does the Section 1042 Rollover Work?

The Section 1042 rollover allows a C corporation shareholder to defer capital gains tax on the sale of stock to an ESOP by reinvesting the proceeds in qualified replacement property within a defined window. The deferral is permanent as long as the replacement property is held; the deferred capital gain becomes taxable only when the replacement securities are sold. If the seller holds the replacement property until death, the gain may be eliminated entirely through a stepped-up basis at death.

The four conditions required for a valid Section 1042 election are:

- C Corporation Requirement – only C corporation shareholders qualify; S corporation sellers, family members, and certain related parties are excluded from the election

- 30 Percent Threshold – the ESOP must own at least 30 percent of outstanding stock immediately after the sale for the election to be valid

- Qualified Replacement Property – proceeds must be reinvested in domestic operating corporation securities within 12 months before or after the sale date

- Election Timing – the seller must file the Section 1042 election with their federal tax return for the year of sale; no late elections are permitted

The Section 1042 rollover is the largest single tax benefit available to ESOP sellers and the primary reason C corporation owners evaluate an ESOP ahead of a third-party sale. A $5 million capital gain at the 23.8 percent combined federal rate represents over $1.19 million in deferred tax. According to the American Bar Association (2023), both the seller and the corporation must execute a consent agreement filed with the return; any procedural defect can invalidate the election entirely.

What Tax Benefits Do S Corp ESOPs Get?

S corporation ESOPs receive a different and, for many profitable companies, equally powerful set of tax advantages. Income attributable to the ESOP-owned percentage of an S corporation is exempt from federal income tax because the ESOP trust is a tax-exempt entity. A 100 percent ESOP-owned S corporation eliminates its entire federal income tax liability on operating earnings, generating cash to service acquisition debt, fund the repurchase obligation, or reinvest in operations.

Income allocable to ESOP-owned S corporation shares is excluded from federal income tax proportional to the ESOP ownership percentage. Most states conform to this exclusion, but several do not, and owners must confirm state-level treatment with tax counsel before projecting total savings. S corporation sellers cannot use the Section 1042 rollover; owners sometimes evaluate converting to C corporation status before the transaction to access the rollover.

National advisory firms such as Stout and Kroll perform ESOP trustee valuations for institutional S corporation transactions. Sofer Advisors delivers the same credentialed independent analysis for lower middle market S corporation ESOP candidates. The income tax exclusion can be material: a company with $2 million in annual taxable income that converts to 100 percent ESOP ownership eliminates that federal income tax liability entirely. The federal exclusion is the most consistent and quantifiable of the three ESOP benefit categories for profitable S corporations.

What Tax Benefits Do Employees Receive?

Employees in an ESOP accumulate company shares in their individual accounts on a tax-deferred basis, with no income tax owed on share allocations or account growth until they receive a distribution from the plan. The employing company, not the employee, funds the ESOP contributions, so employees build ownership without reducing take-home pay. This structure makes the ESOP a supplemental retirement benefit that operates alongside any 401(k) or pension the company maintains.

Shares allocated to employee accounts are excluded from gross income in the year allocated; income tax is deferred until the employee receives a distribution. The ESOP trust pays no income tax on share appreciation, compounding the full pretax value across the employee’s tenure. Employees who receive a distribution can roll proceeds into an IRA or qualified plan, deferring income tax until retirement withdrawals begin. The ESOP is entirely employer-funded, creating an ownership stake employees receive as a benefit of employment.

According to ERISA (2024), the ESOP trustee has a fiduciary duty to ensure employees receive shares valued at fair market value in each annual appraisal, protecting employee retirement benefits and shielding the trustee from personal liability. An employee who accumulates $200,000 in ESOP shares over a career owes no income tax on that value until distribution and can defer further by rolling into an IRA at retirement. The combination of employer-funded accumulation and tax-deferred growth makes the ESOP one of the most valuable retirement benefits available to non-executive employees.

What Are the Limits of ESOP Tax Benefits?

ESOP tax benefits do not apply automatically. The Section 1042 election requires a properly filed consent agreement; the S corporation income exclusion requires the ESOP to remain a qualified plan; and the employee tax deferral requires an annual independent appraisal confirming fair market value. Failure to satisfy any of these conditions triggers disqualification and retroactive tax liability with no corrective remedy available.

The four most significant limits on ESOP tax benefits are:

- Annual Valuation Requirement – the ESOP trustee must obtain a credentialed independent fair market value appraisal every year; failure disqualifies the plan and converts all deferred tax into immediate taxable liability

- Prohibited Transaction Rules – ERISA prohibits the ESOP from paying more than fair market value; a trustee who overpays faces personal liability and possible plan disqualification

- Repurchase Obligation – as employees retire and redeem vested shares, the company must fund repurchases from operating cash; a growing obligation can offset the annual income tax savings if not modeled before the transaction

- S Corporation Anti-Abuse Rules – IRC Section 409(p) prevents S corporation ESOPs from disproportionately benefiting highly compensated individuals; violations trigger an excise tax that eliminates the income exclusion

A Section 1042 election that fails due to a missed filing or a procedural defect in the consent agreement exposes the seller to the full capital gains liability they sought to defer. A plan that loses qualified status due to a deficient annual appraisal eliminates the income tax exclusion the company counted on to service its acquisition debt. Completing a credentialed feasibility study and formal valuation before the transaction closes is the most cost-effective way to protect access to each category of ESOP tax benefit.

Understanding the ESOP tax benefits at each level is the foundation for evaluating whether an employee ownership plan is the right exit vehicle. The valuation, debt capacity, and repurchase obligation must be modeled alongside the tax benefits to confirm the full picture.

Frequently Asked Questions

What is the tax benefit of an ESOP for the owner?

The primary benefit for a selling C corporation owner is the Section 1042 capital gains deferral. Selling at least 30 percent of company stock to an ESOP and reinvesting proceeds in qualified replacement property within 12 months defers the capital gains tax indefinitely. If the replacement property is held until death, the gain may be eliminated through a stepped-up basis. S corporation sellers do not qualify.

What is the ESOP 30% rule?

The ESOP 30 percent rule is the minimum ownership threshold for a C corporation seller to elect the Section 1042 capital gains rollover. After the sale, the ESOP must own at least 30 percent of outstanding stock for the election to be valid, measured immediately after close. The rule applies only to C corporation sellers; S corporation sellers are excluded regardless of ownership percentage transferred.

How do I avoid tax on an ESOP sale?

A C corporation seller who qualifies for Section 1042 avoids capital gains tax by reinvesting proceeds in domestic operating corporation securities within the 12-month window. The deferral is permanent while the replacement property is held. Sellers who hold until death may eliminate the deferred gain entirely through a stepped-up basis. S corporation sellers do not have access to this mechanism.

What is the downside to an ESOP?

The primary downside is the debt the company takes on to fund the ownership transfer, typically consuming 30 to 40 percent of annual pre-tax earnings during repayment. The repurchase obligation grows as employees retire and redeem shares, creating a second long-term liability. The ESOP tax benefits reduce income tax expense but do not eliminate the debt service and repurchase costs funded from operating earnings.

Can an S corp owner use Section 1042?

No. The Section 1042 rollover is available only to C corporation shareholders; S corporation shareholders are explicitly excluded. Owners who want access to Section 1042 sometimes evaluate converting to C corporation status before the ESOP transaction. A conversion triggers additional tax analysis, including potential built-in gains tax on pre-conversion appreciation, that must be weighed before any structural changes are made.

Are ESOP distributions taxable to employees?

Yes. ESOP distributions are taxable as ordinary income unless rolled into an IRA or qualified plan within 60 days. The deferral applies during accumulation inside the trust; distribution is the triggering income tax event. Employees who roll to an IRA continue deferring until retirement withdrawals begin. A direct cash distribution also incurs a 10 percent early withdrawal penalty for employees under age 59 and a half.

How does an ESOP reduce company taxes?

An S corporation ESOP excludes income attributable to ESOP-owned shares from federal income tax, scaling proportionally with the ownership percentage. A C corporation ESOP allows the company to deduct contributions used to repay the acquisition loan, converting debt repayments into deductible expense. Both reduce taxable income but operate under different IRC provisions and apply to different corporate structures.

How much does an ESOP valuation cost from Sofer Advisors?

An independent ESOP valuation from Sofer Advisors typically costs $15,000 to $35,000 depending on company size, the complexity of the capital structure, and whether the engagement includes a repurchase obligation study alongside the formal share valuation. A feasibility-level engagement costs $7,500 to $25,000 and is typically completed four to eight weeks from receipt of financial materials. Contact Sofer Advisors to scope the right engagement for your transaction stage.

Related Case Studies

- Deferred Compensation Dispute: Precise Valuation Changed the Outcome

- Divorce Business Valuation: Resolving Conflict Through Expert Analysis

- Valuation Timing: Why the Right Date Changes Everything

Executive Summary

ESOP tax benefits operate at three levels: C corp sellers defer capital gains under Section 1042; S corps exclude ESOP-attributable income from federal income tax; and employees accumulate shares tax-deferred with IRA rollover rights at distribution. Each benefit carries qualifying conditions under the Internal Revenue Code and ERISA. A credentialed independent appraisal is required annually to maintain plan qualification and protect access to all three tax advantages.

What Should You Do Next?

Commission an independent valuation before structuring the ESOP transaction. A credentialed fair market value appraisal is a legal prerequisite for every ESOP tax benefit and protects the trustee, the seller, and the employees from disqualification risk.

David Hern CPA ABV ASA, founder of Sofer Advisors, provides independent ESOP valuations and feasibility studies for business owners evaluating employee ownership as an exit strategy. Schedule a consultation to discuss the right approach for your transaction.

People Also Read

- ESOP Transaction Process: A Complete Guide for Business Owners

- Business Succession Planning Tips for Smooth Ownership Transfers

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors, a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This content is for informational purposes only and does not constitute professional valuation advice. Business valuation conclusions depend on specific facts and circumstances. Contact Sofer Advisors for guidance regarding your specific situation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}