Embedded Derivatives Definition: Atlanta Financial Guide

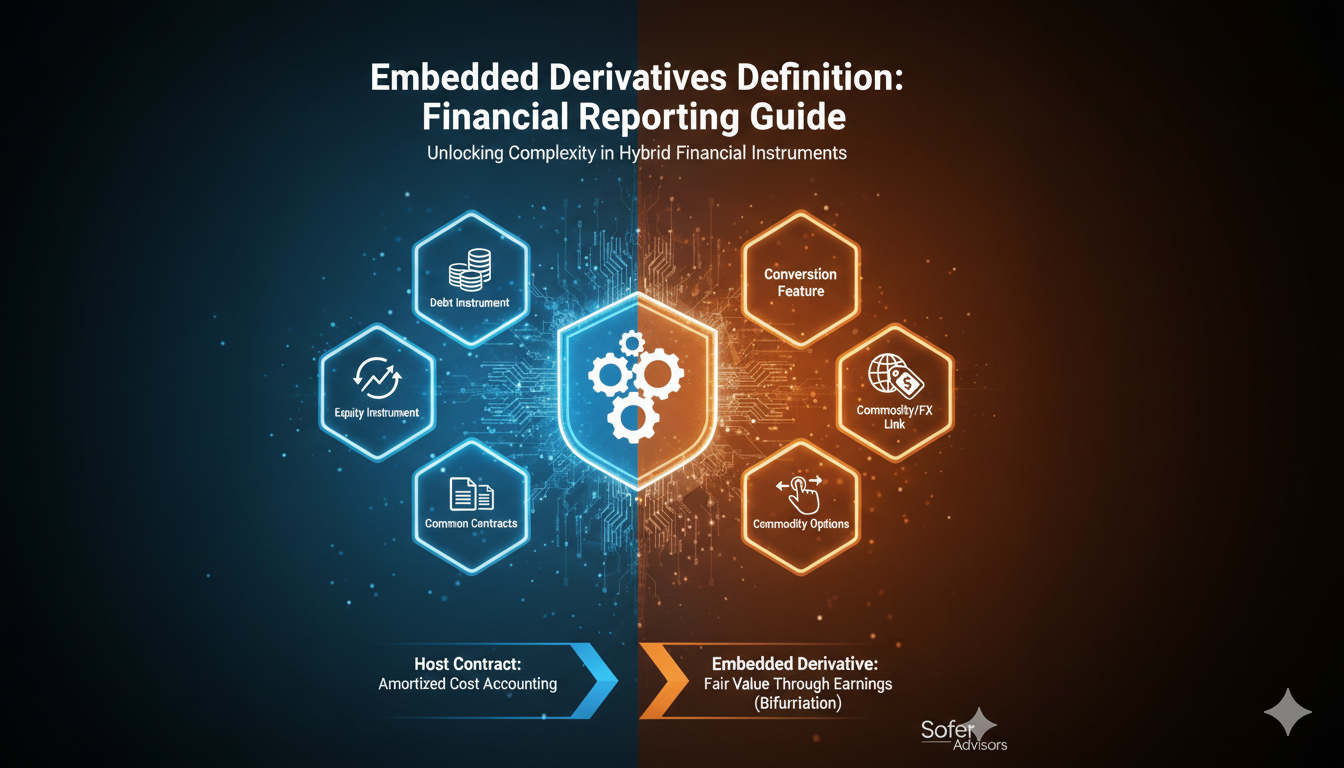

An embedded derivative is a component of a financial instrument that modifies the cash flows of the host contract based on changes in an underlying variable such as interest rates, commodity prices, or foreign exchange rates. These derivatives cannot be transferred separately from their host contract and require specialized accounting treatment under ASC 815. Understanding embedded derivatives becomes essential when Atlanta companies issue convertible bonds, structured notes, or other hybrid financial instruments.

For business owners and financial professionals in Atlanta’s growing finance and technology sectors, embedded derivatives represent a complex area where traditional accounting meets sophisticated financial engineering. Sofer Advisors provides specialized valuation services for embedded derivatives, helping Georgia companies navigate bifurcation requirements and fair value measurements that satisfy Big Four auditor scrutiny. The accounting treatment can significantly impact financial statements-often by millions of dollars for companies with substantial convertible debt-requiring careful analysis to determine whether bifurcation from the host contract is necessary. Atlanta-based public companies facing SEC filing deadlines must ensure compliant embedded derivative accounting to maintain stakeholder confidence.

What distinguishes embedded derivatives from standalone instruments?

Embedded derivatives differ fundamentally from standalone derivatives in their structure and transferability. Unlike freestanding derivatives that exist as separate contracts, embedded derivatives are integral components of hybrid financial instruments that cannot be transferred independently of their host contract.

For Atlanta companies in technology, healthcare, and real estate sectors issuing convertible securities, understanding this distinction proves critical. The conversion feature allows bondholders to exchange their bonds for equity shares under specified conditions, creating derivative characteristics embedded within traditional debt.

Key Differences Between Embedded and Standalone Derivatives:

– Transferability: Standalone derivatives trade independently; embedded derivatives cannot be separated from host contracts – Accounting treatment: Standalone derivatives receive direct fair value treatment; embedded derivatives require bifurcation analysis – Counterparty: Standalone derivatives may have different counterparties; embedded derivatives share the host contract’s counterparty – Legal structure: Standalone derivatives exist as separate contracts; embedded derivatives are contractual terms within larger instruments – Valuation complexity: Standalone derivatives often have observable market prices; embedded derivatives typically require model-based valuations – Documentation: Standalone derivatives have independent agreements; embedded derivatives exist within host contract documentation

Recognition of embedded derivatives requires evaluation under ASC 815. Atlanta companies working with external auditors from Deloitte, PwC, EY, or regional firms like Aprio must assess each hybrid instrument to determine if the embedded derivative significantly modifies the host contract’s risk characteristics.

How does ASC 815 define embedded derivative accounting requirements?

ASC 815 establishes comprehensive guidance for embedded derivative accounting, requiring companies to evaluate three critical criteria for bifurcation. First, the embedded derivative must not be clearly and closely related to the host contract’s economic characteristics. Second, the hybrid instrument must not be measured at fair value through earnings. Third, a separate instrument with the same terms as the embedded derivative would qualify as a derivative under ASC 815.

ASC 815 Bifurcation Criteria (All Three Must Be Met):

- Not clearly and closely related: The embedded derivative’s economic characteristics differ significantly from the host contract

- Not fair value measured: The hybrid instrument is not already measured at fair value with changes in earnings

- Derivative qualification: A hypothetical freestanding instrument with identical terms would meet the ASC 815 derivative definition

Bifurcation becomes necessary when these criteria are met, requiring companies to separate the embedded derivative from its host contract for accounting purposes. The embedded derivative receives fair value measurement with changes reported in earnings.

For Atlanta-based companies, professional embedded derivative valuations typically cost $5,000-$15,000 per instrument for straightforward features, with complex structured products ranging from $15,000-$50,000. Sofer Advisors, headquartered in Atlanta with certified valuation professionals holding CPA, ABV and ASA credentials, develops appropriate fair value measurements ensuring compliance with ASC 820 standards.

Documentation becomes crucial, as companies must demonstrate their analysis regarding bifurcation requirements. External auditors, including Atlanta offices of Big Four firms and regional CPA firms, scrutinize embedded derivative conclusions closely during financial statement audits.

What types of contracts commonly contain embedded derivatives?

Convertible bonds represent the most common example of embedded derivatives, where bondholders can convert their debt into equity shares at predetermined ratios. Atlanta technology companies and healthcare organizations often use convertible bonds to reduce borrowing costs-often by 2-4% compared to straight debt-while providing investors with potential equity appreciation.

Common Instruments Containing Embedded Derivatives:

– Convertible bonds: Debt with equity conversion features requiring bifurcation analysis – Callable bonds: Issuer redemption options that modify bondholder cash flows – Puttable bonds: Holder options to sell bonds back before maturity – Structured notes: Principal-protected instruments linked to indices or commodities – Convertible preferred stock: Preferred shares with common stock conversion rights – Warrant-attached debt: Bonds issued with detachable or non-detachable warrants – Foreign currency contracts: Debt denominated in non-functional currencies – Commodity-linked instruments: Financing tied to oil, gold, or other commodity prices

Structured notes combine traditional debt with derivative features linked to underlying assets, indices, or other variables. Banks and financial institutions-including Atlanta-based Truist, as well as major issuers like Goldman Sachs and Morgan Stanley-issue structured notes to provide customized investment exposure.

Georgia companies preparing for IPOs or capital raises frequently encounter equity-linked instruments, requiring professional business valuation services to ensure proper accounting treatment.

When does bifurcation become mandatory for embedded derivatives?

Bifurcation becomes mandatory when embedded derivatives fail the “clearly and closely related” test under ASC 815. This evaluation examines whether the embedded derivative’s economic characteristics and risks relate closely to those of the host contract. For example, an interest rate cap embedded in variable-rate debt would typically be considered clearly and closely related.

A practical example illustrates the bifurcation impact for Atlanta companies: Consider a $50 million convertible bond with a conversion feature valued at $8 million. Without proper bifurcation, the entire $50 million appears as debt. With correct accounting, the company records $42 million in debt liability and $8 million as an equity component-a significant balance sheet presentation difference affecting leverage ratios and debt covenant calculations.

Fair value election provides an alternative to bifurcation, allowing companies to measure entire hybrid instruments at fair value through earnings. Georgia companies must carefully consider the financial statement impact, often consulting with their Atlanta-based CPAs and external auditors before making this irrevocable election.

David Hern CPA ABV ASA, founder of Sofer Advisors, emphasizes that Atlanta companies should engage valuation specialists early when issuing hybrid instruments. Proactive engagement prevents year-end surprises and ensures audit-ready documentation.

How are embedded derivatives valued for financial reporting?

Valuation of embedded derivatives follows ASC 820 fair value measurement principles, requiring market-based inputs when available or model-based approaches for instruments lacking active markets. Option pricing models provide the foundation for most embedded derivative valuations, with binomial trees and Monte Carlo simulations commonly employed for complex features.

These models incorporate relevant inputs including underlying asset prices, volatility (typically ranging from 25-60% for equity-linked features), interest rates, credit spreads, and time to expiration. A 10% change in volatility assumptions can shift embedded derivative values by 15-25%.

Credit risk adjustments become essential, as the derivative’s value depends on the issuer’s ability to perform under the contract terms. Credit valuation adjustments (CVA) and debit valuation adjustments (DVA) modify fair value measurements, typically adding 2-8% to derivative values for investment-grade issuers and 10-25% for below-investment-grade companies.

For Atlanta companies, Sofer Advisors provides quarterly and annual revaluation services for embedded derivatives, ensuring accurate valuations that satisfy external auditor requirements and SEC reporting standards. Our Atlanta-based team coordinates with your finance department to align valuation timelines with reporting deadlines.

What challenges do companies face with embedded derivative compliance?

Identification challenges represent the initial hurdle, as companies must systematically review their financial instruments to identify potential embedded derivatives. Many Atlanta organizations lack internal expertise to properly evaluate sophisticated instruments, potentially missing embedded derivatives that require bifurcation-errors that can result in material misstatements.

Valuation complexity creates ongoing compliance challenges, particularly for instruments lacking observable market inputs. The technical nature of option pricing models often necessitates external valuation expertise, with annual embedded derivative valuation costs ranging from $10,000-$75,000 depending on portfolio complexity.

Timing pressures intensify for Atlanta companies during quarterly and year-end close periods. Public companies facing SEC filing deadlines of 60-75 days must complete embedded derivative valuations while managing regular financial reporting processes.

While larger firms like Kroll and Stout serve enterprise clients, Sofer Advisors specializes in middle-market Atlanta businesses requiring practical solutions that integrate with existing financial systems while satisfying Big Four and regional audit firm requirements.

Frequently Asked Questions

What are the 4 types of derivatives?

The four main types of derivatives include forwards, futures, options, and swaps, each serving different risk management purposes for Atlanta companies. Forwards and futures represent contracts to buy or sell assets at predetermined prices, with futures being standardized and exchange-traded while forwards are customized private agreements. Options provide holders the right to buy or sell underlying assets at specified prices, offering asymmetric risk profiles commonly used in convertible securities. Swaps involve exchanging cash flows between parties over specific periods for managing interest rate, currency, or commodity price exposures.

What is the difference between freestanding and embedded derivatives?

Freestanding derivatives exist as separate, transferable contracts that can be bought and sold independently in financial markets. Embedded derivatives are integral components of hybrid financial instruments that cannot be transferred separately from their host contracts, such as conversion features in convertible bonds commonly issued by Atlanta technology and healthcare companies. This distinction becomes crucial for accounting purposes, as embedded derivatives may require bifurcation and separate valuation under ASC 815, while freestanding derivatives receive direct fair value treatment.

Which is not an embedded derivative?

A derivative that can be contractually transferred independently of its host instrument, or has a different counterparty than the host contract, is not considered an embedded derivative under ASC 815. For example, a warrant issued alongside a bond but legally detachable and transferable constitutes a freestanding derivative rather than an embedded derivative. Atlanta companies issuing hybrid instruments should work with their auditors and valuation specialists to properly classify each derivative feature.

How do companies identify embedded derivatives in their contracts?

Companies identify embedded derivatives through systematic contract review processes that evaluate whether instruments contain features that modify cash flows based on underlying variables like interest rates, stock prices, or commodity prices. Finance teams typically develop checklists covering common embedded derivatives including conversion options, call provisions, and interest rate caps. Many Atlanta organizations engage external specialists like Sofer Advisors to review complex instruments and ensure comprehensive identification. Our Atlanta team works alongside your finance department to establish ongoing identification processes.

What documentation is required for embedded derivative accounting?

Embedded derivative documentation must include detailed analysis supporting bifurcation conclusions, including evaluation of the clearly and closely related criteria under ASC 815. Companies should document the economic characteristics of both the host contract and embedded derivative. Valuation documentation requires detailed support for fair value measurements, including model selection and input assumptions. Atlanta companies working with Big Four auditors or regional firms like Aprio typically require external valuation reports from credentialed specialists.

How often must embedded derivatives be revalued?

Embedded derivatives requiring bifurcation must be revalued at each reporting period, typically quarterly for public companies and annually for private companies following ASC 815 requirements. The revaluation process involves updating market inputs, reassessing credit risk factors, and recalculating fair value measurements. Changes in fair value flow directly through earnings, creating potential income statement volatility that Atlanta companies must carefully manage. Sofer Advisors provides quarterly revaluation services coordinated with your close calendar.

What happens if companies incorrectly account for embedded derivatives?

Incorrect embedded derivative accounting can result in material financial statement misstatements requiring restatement, potentially triggering SEC enforcement actions or audit deficiencies. Common errors include failing to identify embedded derivatives, incorrect bifurcation conclusions, or inappropriate valuation methods that violate ASC 815 requirements. These mistakes can affect debt classifications and balance sheet presentations, potentially impacting debt covenant compliance. Atlanta companies discovering embedded derivative accounting errors should immediately consult with their auditors and valuation advisors.

What is the fair value election for hybrid instruments?

The fair value election allows companies to measure entire hybrid instruments at fair value with changes recognized in earnings, eliminating the need for bifurcation analysis under ASC 815. This irrevocable election simplifies accounting but introduces earnings volatility from fair value fluctuations. Georgia companies typically consider this election when bifurcation would be complex. The election must be made at instrument inception and documented appropriately.

How do embedded derivatives affect debt covenant calculations?

Embedded derivatives can significantly impact debt covenant calculations by changing the classification and measurement of financial instruments on the balance sheet. Bifurcated embedded derivatives reduce reported debt when equity-classified, improving leverage ratios and debt-to-equity calculations. Conversely, derivative liabilities increase total liabilities and may trigger covenant violations if not properly anticipated. Atlanta companies should analyze their debt agreements to understand how embedded derivative accounting affects covenant metrics and discuss potential implications with lenders before issuing hybrid instruments containing derivative features.

What industries commonly issue instruments with embedded derivatives?

Financial services, technology, biotechnology, and real estate industries frequently issue instruments containing embedded derivatives due to their capital-intensive operations and investor preferences. Atlanta’s growing technology sector and established healthcare industry often use convertible debt to minimize current interest costs while providing investors with equity upside potential. Real estate companies in Georgia’s expanding commercial and residential markets use embedded derivatives in mortgage instruments and property-linked financing. Each industry’s specific characteristics influence the types of embedded derivatives encountered and the valuation approaches required for accurate financial reporting.

Conclusion

Embedded derivative accounting under ASC 815 represents one of the most technically challenging areas of financial reporting for Atlanta companies, requiring specialized expertise in both accounting standards and valuation methodologies. The bifurcation analysis, fair value measurements, and ongoing revaluation requirements create compliance complexity that most internal finance teams cannot address without external support.

The financial statement impact of embedded derivatives extends beyond accounting technicalities-affecting leverage ratios, debt covenant calculations, earnings volatility, and investor perceptions of financial health. A $100 million convertible bond issuance might include $15-25 million in embedded derivative value requiring separate recognition and quarterly revaluation. Getting this accounting wrong can trigger covenant violations, complicate refinancing discussions, and erode investor confidence.

Sofer Advisors, with 180+ five-star Google reviews and Inc. 5000 recognition, provides comprehensive embedded derivative services for Atlanta companies including identification support, bifurcation analysis, initial and ongoing fair value measurements, and documentation packages that satisfy Big Four auditor requirements. Our Atlanta-based team works alongside your CPAs, external auditors, and legal counsel to ensure coordinated compliance that meets SEC reporting standards and investor expectations.

SCHEDULE A CONSULTATION to discuss your embedded derivative valuation needs and discover how professional support ensures accurate financial reporting and audit-ready documentation for your Georgia business.

This article provides general information for educational purposes only and does not constitute legal, tax, financial, or professional advice-consult qualified professionals regarding your specific circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}