Personal Goodwill vs Enterprise Goodwill: Tax & Divorce Guide for Atlanta Business Owners

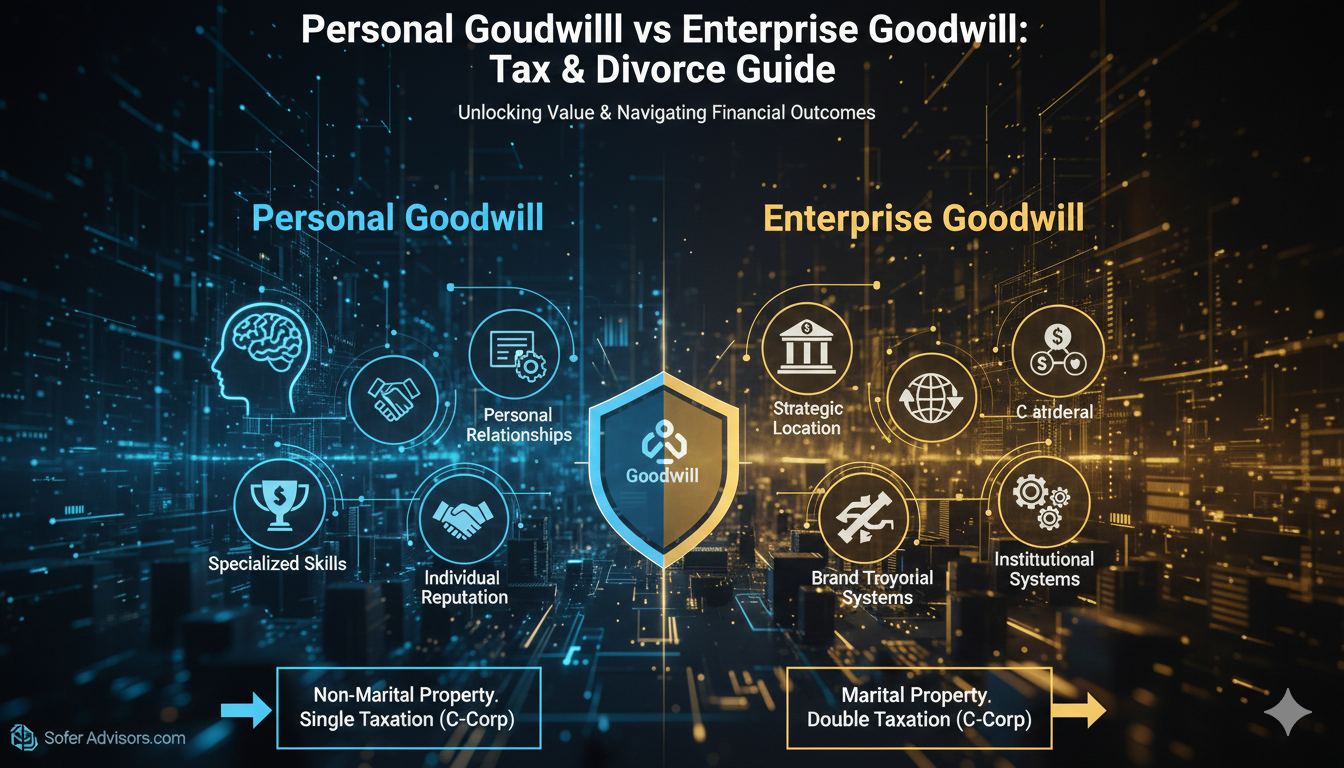

A personal goodwill vs enterprise goodwill distinction is the critical difference between intangible value tied to an individual’s reputation and skills versus intangible value inherent to the business entity itself under established valuation standards [AICPA Practice Aid: Assets Acquired in a Business Combination to Be Used in Research and Development Activities]. Personal goodwill includes an owner’s reputation, specialized expertise, and personal relationships with clients, while enterprise goodwill encompasses transferable assets like company name, location, customer base, and institutional systems. This distinction carries significant implications for tax planning during business sales under IRC Section 197 and Treasury Regulation §1.197-2, asset division in divorce proceedings under Georgia equitable distribution statutes [O.C.G.A. §19-5-13], and valuation accuracy in mergers and acquisitions requiring ASC 805 compliance.

This classification matters because personal goodwill in C Corporation sales receives single-level taxation treatment at capital gains rates under IRC Section 1(h), while enterprise goodwill faces double taxation at both corporate and individual levels under IRC Section 11 and Section 301. In divorce cases, Georgia courts following Mitcham v. Mitcham [263 Ga. 182 (1993)] and similar precedents treat personal goodwill as non-marital property exempt from equitable division, whereas enterprise goodwill constitutes divisible marital property. For Atlanta business owners-whether operating professional practices in Buckhead, manufacturing facilities along I-85, or service companies throughout metro Atlanta-understanding this distinction can mean differences of hundreds of thousands of dollars in tax liability or divorce settlements.

What is personal goodwill in business valuation?

Personal goodwill represents the intangible value attributable solely to an individual owner’s reputation, specialized skills, industry knowledge, and personal relationships with clients and suppliers under Revenue Ruling 59-60 fair market value standards. This type of goodwill is non-transferable and depends entirely on the specific person’s continued involvement in the business, distinguishing it from enterprise goodwill that transfers with ownership changes.

Components of personal goodwill include the owner’s professional reputation within their industry, specialized technical expertise that clients specifically seek out, and established personal relationships with key customers and suppliers per the factors established in Martin Ice Cream Co. v. Commissioner [110 T.C. 189 (1998)]. A classic example involves an Atlanta attorney whose clients specifically seek their counsel rather than just any lawyer at the firm, or a Buckhead plastic surgeon whose patients travel from across the Southeast specifically for their expertise.

The non-transferable nature of personal goodwill creates significant implications during business transitions analyzed under ASC 805 purchase price allocation requirements. When a business with substantial personal goodwill is sold, revenue often declines because customers follow the departing owner rather than continuing with the new ownership. This reality affects both sale valuations using the income approach and buyer willingness to pay premium prices for Georgia businesses.

Business appraisers certified through NACVA (National Association of Certified Valuators and Analysts) and the American Society of Appraisers examine five key characteristics when identifying personal goodwill: individual reputation reflecting professional standing and recognition within the industry that cannot transfer to new ownership, specialized skills encompassing technical expertise, certifications, or unique capabilities that clients specifically seek from the individual, personal relationships including direct connections with clients, suppliers, and industry contacts built over time through individual effort, non-contractual dependencies describing revenue streams that exist because of personal trust rather than formal business agreements, and celebrity value representing recognition or notoriety attached to the individual rather than the business entity.

Tax implications favor personal goodwill classification in C Corporation asset sales under the precedent established in Martin Ice Cream Co. v. Commissioner, where the Tax Court held that personal relationships of shareholder-employees are not corporate assets when no employment contract exists with the corporation. For Atlanta business owners selling C Corporations, this distinction can reduce effective tax rates from 35-50% on enterprise goodwill to 15-20% on personal goodwill-potentially saving $200,000 or more on a $1 million goodwill allocation.

What is enterprise goodwill?

Enterprise goodwill encompasses the intangible value inherent to the business entity itself, independent of any individual’s involvement and transferable upon ownership change under ASC 350 (Intangibles-Goodwill and Other) accounting standards. This category includes established business systems, brand recognition, strategic location advantages, and institutional customer relationships that continue regardless of ownership transitions and qualify as amortizable IRC Section 197 intangibles over 15 years.

Transferable enterprise assets include the company’s established name and brand recognition protectable under the Lanham Act, prime business location and associated foot traffic reflected in lease agreements, existing customer contracts and institutional relationships documented in accounts receivable aging, and established supplier networks with preferential terms. These elements retain value during ownership transitions because they attach to the business entity rather than specific individuals per ASC 805-20-25 recognition criteria.

For Atlanta businesses, enterprise goodwill often concentrates in location-dependent advantages. A restaurant in Virginia-Highland benefits from neighborhood foot traffic regardless of chef changes. A manufacturing company in Gwinnett County maintains supplier relationships and distribution networks that transfer with ownership. A professional services firm in Midtown Atlanta retains institutional client relationships documented through formal engagement agreements rather than personal connections.

Going-concern value represents a significant component of enterprise goodwill under Treasury Regulation §1.197-2(b)(1), reflecting the established income streams and normalized expected earnings that distinguish operating businesses from startups. This value stems from proven business processes, established market position in the Atlanta metropolitan area’s $400+ billion economy, and predictable revenue patterns that new owners can reasonably expect to continue based on historical financial performance.

Valuation professionals evaluate six core elements when assessing enterprise goodwill under AICPA Statement on Standards for Valuation Services VS Section 100: brand recognition including company name, trademark, and reputation that exists independently of current ownership, strategic location encompassing physical location advantages in metro Atlanta markets, lease agreements, and geographic market position, customer contracts representing formal agreements and institutional relationships that transfer with ownership, established systems including business processes, operational procedures, and institutional knowledge documented in operations manuals, workforce assets covering trained employees, organizational structure, and collective expertise under ASC 805-20-55-6 assembled workforce considerations, and market position reflecting competitive advantages, market share within Georgia markets, and established distribution channels.

Buyers typically prefer businesses with higher enterprise goodwill because these assets provide more predictable revenue streams and reduced integration risk per M&A due diligence standards. The transferable nature of enterprise goodwill supports higher valuations under the market approach and more confident acquisition decisions compared to businesses dependent on personal goodwill that may not survive ownership transition.

Why does the distinction matter for taxes?

The allocation between personal and enterprise goodwill creates substantial tax implications under IRC Sections 197, 1001, and 1060, particularly for C Corporation asset sales where different treatment can save hundreds of thousands of dollars for Atlanta business owners. Personal goodwill receives single-level taxation at capital gains rates under IRC Section 1(h), while enterprise goodwill faces double taxation at both corporate levels under IRC Section 11 (21% federal rate) and individual levels under IRC Sections 301 and 302.

For C Corporation sales structured as asset transactions under IRC Section 1060, enterprise goodwill allocated to the corporation triggers corporate-level taxation on the sale proceeds, followed by additional individual taxation when distributions occur as dividends or liquidating distributions. Personal goodwill, however, can be treated as a separate asset sale by the individual shareholder under the Martin Ice Cream precedent, avoiding corporate-level taxation entirely when properly documented with contemporaneous evidence.

The tax treatment comparison demonstrates the magnitude of potential savings for Georgia business owners:

Personal Goodwill Tax Treatment:

- No corporate-level tax applies

- Capital gains rate of 15-20% under IRC Section 1(h)

- Georgia state capital gains rate of 5.49% (2026)

- Effective combined rate: 20-26%

Enterprise Goodwill Tax Treatment:

- Corporate tax at 21% federal under IRC Section 11

- Georgia corporate tax at 5.75%

- Individual tax at 20-37% on distributions

- Georgia individual tax at 5.49%

- Effective combined rate: 40-55%

For an Atlanta business owner selling $1 million in goodwill, proper allocation to personal goodwill could save $150,000-$290,000 in taxes compared to enterprise goodwill treatment. These savings compound significantly for larger transactions common among successful metro Atlanta businesses.

Proper goodwill allocation requires documented support through professional valuation analysis meeting AICPA VS Section 100 standards. The IRS scrutinizes personal goodwill claims under audit procedures, requiring evidence that the value truly depends on the individual rather than transferable business assets per Treasury Regulation §1.197-2(b)(1). Factors supporting personal goodwill include lack of employment contracts per Martin Ice Cream, individual-dependent customer relationships documented through customer surveys, and specialized skills that cannot transfer demonstrated through licensing requirements or credentials.

The landmark Martin Ice Cream Co. v. Commissioner [110 T.C. 189 (1998)] established that personal relationships of shareholder-employees are not corporate assets when no employment contract exists with the corporation. The Eighth Circuit affirmed similar principles in Norwalk v. Commissioner [1998] and subsequent cases including Solomon v. Commissioner [T.C. Memo 2008-102]. These precedents support personal goodwill claims in similar circumstances but require proper documentation and analysis to apply successfully under current IRS examination standards applied by the Atlanta IRS district office.

How does goodwill classification affect divorce in Georgia?

Goodwill classification significantly impacts asset division during divorce proceedings because Georgia courts following equitable distribution principles under O.C.G.A. §19-5-13 treat personal goodwill as non-marital property while considering enterprise goodwill as divisible marital property. This distinction can substantially affect the financial outcomes for business-owning spouses in Fulton, DeKalb, Cobb, Gwinnett, and other metro Atlanta counties.

Personal goodwill typically qualifies as separate property in Georgia because it represents the individual’s personal reputation, skills, and relationships developed through their own efforts. Georgia courts following Mitcham v. Mitcham [263 Ga. 182 (1993)] and Thomas v. Thomas [259 Ga. 73 (1989)] recognize that these attributes cannot be divided or transferred to the other spouse, making them inappropriate for marital property classification under Georgia equitable distribution law.

Enterprise goodwill, however, represents value created during the marriage through joint marital efforts and resources subject to equitable division under O.C.G.A. §19-5-13. This category includes business assets that both spouses may have contributed to building, either directly through work or indirectly through supporting the business-owning spouse’s efforts per marital partnership theory recognized by Georgia Superior Courts.

Courts and forensic accountants examine five primary factors when classifying goodwill in Georgia divorce proceedings per the framework established in Dugan v. Dugan [New Jersey 1983] and adopted in Georgia practice: income generation source determining whether revenue depends on the individual’s presence or business systems, customer relationship structure distinguishing personal relationships from institutional business connections documented in CRM systems, marketing and branding focus revealing whether promotion centers on the individual professional or company identity, employment agreements indicating contracts that tie the individual to the business entity under Georgia enforceability standards, and competitive positioning showing whether the business depends on individual expertise or transferable institutional advantages.

Professional valuation becomes crucial in Georgia divorce cases to properly allocate goodwill between personal and enterprise categories under AICPA VS Section 100 and Georgia expert witness requirements. Expert witnesses testifying in Fulton County Superior Court or other metro Atlanta venues must provide detailed analysis supporting their allocation decisions using the Multi-Attribute Utility Method (MUM) or similar peer-reviewed frameworks, often requiring extensive documentation and testimony subject to Georgia evidence rules.

The financial stakes for Atlanta business owners in divorce are substantial. A professional practice worth $2 million with 70% personal goodwill allocation means only $600,000 of enterprise goodwill enters the marital estate for division-compared to the full $2 million if improperly classified entirely as enterprise goodwill. This $1.4 million difference demonstrates why proper goodwill analysis from qualified valuators is essential for Georgia divorce proceedings.

The stakes are particularly high in professional practices where personal goodwill often dominates per established case law. Medical practices in Atlanta’s healthcare corridor, legal firms in downtown Atlanta, and consulting businesses in Buckhead frequently involve substantial personal goodwill that affects divorce settlement negotiations and court decisions throughout the Atlanta judicial circuit.

What factors determine goodwill allocation?

Professional goodwill allocation relies on systematic analysis of seven key factors that business appraisers examine to distinguish between personal and enterprise components under the Multi-Attribute Utility Method (MUM) framework published in peer-reviewed valuation literature. This approach provides consistent and defensible allocation decisions meeting AICPA VS Section 100 and ASA Business Valuation Standards requirements across different valuation contexts including tax planning, divorce proceedings, and M&A transactions.

Income generation patterns provide the primary indicator of goodwill source under Revenue Ruling 59-60 factor analysis. Businesses where revenue depends heavily on the owner’s direct involvement suggest higher personal goodwill, while institutionalized revenue streams indicate enterprise goodwill dominance based on historical financial performance correlation. For Atlanta professional practices, this often means analyzing whether clients would follow the practitioner to a new Buckhead office or remain with the established firm location.

Customer relationship structure reveals whether clients connect primarily with the individual or the business entity per the factors established in Martin Ice Cream. Personal relationships that clients would follow to a new location suggest personal goodwill, while institutional relationships tied to the business location, contracts, or systems indicate enterprise goodwill. Customer surveys and retention studies following ownership transitions provide empirical evidence supporting allocation conclusions.

The seven-factor analysis framework that ASA-certified and NACVA-certified valuators apply includes:

- Income Generation Dependency – Measuring the extent to which revenue requires the owner’s direct involvement through correlation analysis of financial performance with owner presence per Revenue Ruling 59-60 standards

- Customer Relationship Structure – Determining whether clients connect with the individual or business entity through surveys, retention studies, and relationship documentation per Martin Ice Cream factors

- Marketing and Promotional Focus – Examining individual-centered versus company-centered branding through advertising materials, website content, social media presence, and promotional strategies

- Employment Agreement Terms – Analyzing contractual obligations tying key individuals to the business under Georgia enforceability standards for non-compete and non-solicitation provisions

- Repeat Customer Patterns – Identifying whether clients return for the individual or business services through transaction analysis and customer loyalty metrics

- Profit Allocation Methods – Reviewing how earnings distribute based on individual versus institutional contributions in partnership or S Corporation structures

- Competitive Market Position – Assessing whether advantages stem from individual expertise or transferable business assets through industry benchmarking within Atlanta and Georgia markets

Employment agreements and non-compete clauses affect goodwill classification by demonstrating whether individual contributions are contractually tied to the business per the Martin Ice Cream analysis. Strong employment terms with enforceable non-compete provisions under Georgia law [O.C.G.A. §13-8-53] support enterprise goodwill allocation, while absence of such agreements supports personal goodwill treatment.

Documentation requirements for goodwill allocation meeting IRS and Georgia court scrutiny include detailed interviews with ownership, customer surveys or statistical analysis of relationship patterns, competitive market research within metro Atlanta markets, and financial performance analysis correlating revenue with individual involvement. This evidence supports the valuator’s professional judgment and provides defensible conclusions for tax authorities under audit procedures, Georgia Superior Courts under evidence rules, or transaction parties in M&A negotiations.

When should Atlanta businesses seek goodwill analysis?

Atlanta businesses should obtain professional goodwill analysis before major transitions, tax planning initiatives, or legal proceedings where goodwill classification affects financial outcomes under applicable IRC provisions or Georgia property division statutes. Early analysis provides strategic advantages and ensures proper documentation for future IRS examination or court testimony needs in Fulton County and throughout Georgia.

Transaction planning represents the most common scenario requiring goodwill analysis under IRC Section 1060 allocation requirements. Atlanta business owners contemplating sales, mergers, or succession planning need to understand how goodwill allocation affects tax consequences at both corporate and individual levels. Early analysis allows time to implement strategies that optimize goodwill classification while maintaining substance-over-form compliance with IRS requirements.

Divorce proceedings require goodwill analysis when one spouse owns a business with significant intangible value subject to equitable distribution under O.C.G.A. §19-5-13. The analysis should occur early in the divorce process per Georgia Superior Court discovery rules to allow adequate time for expert testimony preparation under Georgia evidence standards and settlement negotiations based on accurate asset classification.

Purchase price allocation under ASC 805 requires goodwill analysis when Atlanta businesses complete acquisitions for GAAP financial reporting. Acquiring companies must properly allocate the purchase price across tangible assets, identifiable intangibles under ASC 805-20-25, and residual goodwill under ASC 805-30-30 for accurate financial statements filed with the SEC or provided to lenders financing Georgia business acquisitions.

Strategic timing for goodwill analysis follows established best practices across six primary scenarios:

- Pre-Transaction Planning – 6-12 months before anticipated sale or merger discussions to allow implementation time for goodwill optimization strategies

- Divorce Filing Analysis – Within 30-60 days of filing or receiving divorce papers per Georgia discovery deadlines to prepare expert testimony

- Tax Planning Annual Review – Year-end planning sessions with tax advisors particularly for C Corporations where Martin Ice Cream strategies apply

- Succession Planning Development – Aligned with creating or updating family business transition plans under IRC gift and estate provisions

- Partnership Disputes – Before shareholder conflicts escalate to legal proceedings or Georgia statutory dissent appraisal rights under O.C.G.A. §14-2-1301

- Estate Planning Updates – When updating wills, trusts, or gift tax strategies under IRC Sections 2031 and 2512

Tax planning scenarios benefit from annual goodwill assessment, particularly for C Corporations where allocation strategies under Martin Ice Cream principles can significantly impact future sale proceeds. Regular analysis helps identify opportunities to shift goodwill classification through business structure changes, employment agreement modifications, or operational process documentation meeting substance-over-form requirements enforced by the Atlanta IRS district.

How can Atlanta businesses optimize goodwill classification?

Atlanta businesses can implement strategic initiatives to shift goodwill allocation toward more favorable personal or enterprise classification depending on their tax or asset protection objectives under applicable IRC provisions and Georgia property laws. These strategies require advance planning and systematic implementation with proper documentation to achieve desired results while maintaining compliance with IRS substance-over-form doctrine.

Building enterprise goodwill involves creating transferable business assets that operate independently of individual ownership under ASC 805 identifiable intangible recognition criteria. This approach benefits Atlanta businesses seeking higher sale valuations under the market approach and more attractive buyer interest during exit planning for eventual sale to strategic acquirers or private equity firms active in the Georgia market.

Developing institutional systems replaces individual-dependent processes with transferable business operations documented in procedures manuals. Customer relationship management systems capturing institutional rather than personal relationships, standardized service delivery procedures reducing owner dependency, and documented operational processes enabling employee replication reduce dependence on specific individuals and support enterprise goodwill classification for Atlanta businesses.

Enterprise goodwill development focuses on six primary strategies that valuation experts recommend:

- Brand Building – Investing in company name recognition, trademark development under Lanham Act protection, and institutional marketing throughout metro Atlanta rather than individual promotion

- System Documentation – Creating written procedures, training materials, and operational manuals that enable employee replication and demonstrate transferability to potential acquirers

- Customer Contracts – Establishing formal service agreements with assignment provisions and institutional relationships rather than personal handshake deals common in relationship-driven Atlanta business culture

- Employee Development – Building capable teams that can deliver services without owner involvement per workforce-in-place intangible recognition under ASC 805

- Location Investment – Developing strategic location advantages in prime Atlanta submarkets, favorable lease agreements with assignment rights, and physical asset value

- Technology Integration – Implementing systems that create efficiency and competitive advantages independent of individual expertise

Personal goodwill enhancement strategies benefit tax planning scenarios where individual-level treatment under Martin Ice Cream principles provides advantages in C Corporation sales. These approaches require careful implementation to avoid compromising business operations while achieving legitimate tax objectives reviewed by Atlanta-area tax counsel.

Personal goodwill enhancement techniques include individual branding focusing marketing and promotion on the owner’s expertise rather than company identity through professional speaking at Atlanta business events, publications in Georgia industry journals, and personal networking through Atlanta business organizations, direct client relationships maintaining personal connections and avoiding institutional customer management systems that document enterprise relationships, specialized skill development pursuing unique certifications, advanced degrees, or expertise that clients specifically seek from the individual rather than the business, and limited employment contracts avoiding binding the individual’s expertise to the corporate entity through restrictive employment agreements or non-compete provisions that would convert personal goodwill to enterprise assets under Georgia enforceability standards.

Balancing these strategies requires professional guidance to optimize outcomes without creating unintended tax consequences or compromising business operations. The IRS scrutinizes aggressive personal goodwill claims under audit procedures applied by the Atlanta district, requiring genuine economic substance supporting allocation positions documented through contemporaneous evidence rather than post-transaction reconstruction.

Frequently Asked Questions

Can personal goodwill and enterprise goodwill exist in the same business?

Yes, most businesses contain both personal and enterprise goodwill components that professional appraisers must allocate between categories using the Multi-Attribute Utility Method or similar peer-reviewed frameworks under AICPA VS Section 100 standards. The allocation process determines what percentage of total goodwill stems from individual factors versus transferable business assets based on the seven-factor analysis. A successful Atlanta restaurant may have enterprise goodwill from its Virginia-Highland location and brand while also having personal goodwill from the chef-owner’s culinary reputation throughout the metro area.

How do Georgia courts verify personal versus enterprise goodwill claims in divorce cases?

Georgia Superior Courts rely on expert witness testimony from certified business appraisers (ABV, ASA, CVA credentials) who conduct detailed analysis using established valuation methodologies and seven-factor frameworks meeting Georgia evidence standards. The analysis includes customer surveys or statistical retention studies, financial performance correlation analysis, competitive market assessment within Atlanta markets, and documentation of business operations. Appraisers testifying in Fulton, DeKalb, Cobb, or Gwinnett counties must demonstrate that allocation decisions rest on factual evidence rather than speculation.

What happens if the IRS challenges personal goodwill allocation in a business sale?

IRS challenges under audit procedures require taxpayers to provide substantial documentation supporting personal goodwill claims through professional valuation reports meeting AICPA VS Section 100 standards, customer testimony or surveys, employment agreement analysis, and market evidence. The taxpayer bears the burden of proving that allocated value truly depends on individual characteristics per Treasury Regulation §1.197-2. The Martin Ice Cream precedent supports personal goodwill claims when properly documented, but inadequate support can result in reclassification, additional tax liability, accuracy penalties under IRC Section 6662, and interest.

Can non-compete agreements eliminate personal goodwill for tax purposes?

Non-compete agreements alone do not eliminate personal goodwill but can shift some value toward enterprise goodwill if they effectively restrict the individual’s ability to compete under Georgia enforceability standards per O.C.G.A. §13-8-53. Weak or unenforceable agreements under Georgia law provide minimal support for enterprise goodwill claims, while comprehensive agreements meeting reasonableness requirements for geographic scope and duration can demonstrate that expertise is contractually tied to the business entity. Personal goodwill may still exist if customer relationships depend primarily on reputation despite non-compete restrictions.

How often should Atlanta businesses update their goodwill allocation analysis?

Atlanta businesses should update goodwill analysis annually during tax planning or when significant operational changes occur that might affect allocation under the seven-factor framework. Changes in management structure, customer base composition through CRM data, service delivery methods, employment agreements, or competitive positioning within metro Atlanta markets can shift goodwill allocation over time. Businesses anticipating major transitions should conduct analysis 6-12 months before expected events to allow time for strategic planning, implementation, and documentation meeting IRS substance requirements.

What documentation supports personal goodwill claims during business valuations?

Personal goodwill documentation meeting IRS examination standards includes customer testimonials or survey data explaining their relationship with the individual owner, evidence of specialized credentials or professional licenses required in Georgia, marketing materials featuring the individual rather than company brand, and absence of formal employment contracts or enforceable non-compete agreements per Martin Ice Cream analysis. Financial analysis showing revenue correlation with owner involvement through statistical methods strengthens claims. Professional licensing requirements under Georgia law and industry recognition also support personal goodwill allocation.

How do different business structures affect goodwill classification?

Business structure significantly impacts goodwill treatment for tax purposes under IRC provisions, with C Corporations offering the most favorable personal goodwill opportunities per Martin Ice Cream. C Corporation shareholders can potentially sell personal goodwill separately from corporate assets under IRC Section 1001, achieving single-level capital gains taxation under IRC Section 1(h). S Corporation and partnership structures common among Atlanta professional practices may limit personal goodwill separation opportunities due to flow-through taxation characteristics under Subchapter S and Subchapter K, though some planning opportunities exist with proper structuring.

What role do customer contracts play in determining enterprise goodwill?

Customer contracts significantly support enterprise goodwill allocation by demonstrating that client relationships belong to the business entity under ASC 805-20-25 customer relationship intangible recognition criteria. Formal service agreements with assignment provisions, multi-year contracts, and institutional purchasing relationships indicate customers connect with the business rather than individuals. However, contracts alone do not guarantee enterprise classification if underlying services depend entirely on individual expertise that would not transfer with the contractual relationship-common in Atlanta professional services practices.

Can personal goodwill transfer to family members in succession planning?

Personal goodwill generally cannot transfer between individuals because it represents non-transferable characteristics like reputation, skills, and personal relationships under Revenue Ruling 59-60 fair market value principles. Family succession planning under IRC gift and estate provisions can develop enterprise goodwill components that transfer effectively through business entity ownership interests. Next-generation family members joining Atlanta family businesses must build their own personal goodwill through individual effort rather than inheriting it. Strategic planning helps optimize transitions for tax efficiency under IRC Sections 2031 and 2512.

What are common mistakes in goodwill allocation that reduce tax benefits?

Common mistakes include inadequate documentation supporting personal goodwill claims under IRS examination standards, failing to obtain professional valuation analysis meeting AICPA VS Section 100 requirements, and attempting excessive allocation without factual support inviting accuracy penalties under IRC Section 6662. Many Atlanta taxpayers underestimate IRS scrutiny and provide insufficient evidence of the seven factors supporting allocation. Poor timing creates problems when attempting goodwill planning after transaction terms are negotiated without substance-over-form support documented contemporaneously.

How do industry characteristics affect personal versus enterprise goodwill allocation?

Industry characteristics significantly influence goodwill allocation patterns under the Multi-Attribute Utility Method analysis. Professional services including Atlanta medical practices, Buckhead law firms, and Midtown consulting businesses typically show higher personal goodwill due to licensing requirements and individual expertise, while manufacturing companies along I-85 and retail businesses lean toward enterprise goodwill based on transferable systems and location advantages. Technology companies in Atlanta’s growing tech sector show mixed allocation depending on whether success stems from individual innovation or institutional intellectual property.

What happens to goodwill allocation when key employees leave the business?

Key employee departures can shift goodwill allocation by revealing which value components depended on specific individuals versus business systems, providing evidence for future valuation analysis. If revenue follows departing employees documented through customer retention studies, this demonstrates personal goodwill that may have been incorrectly classified as enterprise goodwill in prior valuations. Forward-thinking Atlanta businesses use retention strategies, employment agreements with enforceable non-compete provisions under Georgia law, and institutional relationship development to minimize personal goodwill concentration in key employees beyond the owner.

Conclusion

Understanding the distinction between personal goodwill and enterprise goodwill empowers Atlanta business owners to make strategic decisions that optimize tax outcomes under IRC provisions, protect assets in Georgia divorce proceedings under O.C.G.A. §19-5-13, and maximize business value during transactions requiring ASC 805 compliance. The allocation between these categories affects everything from daily operations to major life transitions including sales, succession planning, and marital dissolution-with potential financial impacts exceeding hundreds of thousands of dollars for successful Georgia businesses.

Successful goodwill management involves regular assessment using the Multi-Attribute Utility Method framework, strategic planning with proper documentation meeting IRS examination standards, and professional valuation analysis from credentialed experts (ABV, ASA, CVA) to support desired allocation outcomes. Whether building enterprise goodwill for an eventual sale to strategic buyers active in the Atlanta market, preserving personal goodwill for C Corporation tax optimization under Martin Ice Cream principles, or preparing for divorce proceedings in Fulton County Superior Court requiring expert testimony meeting Georgia evidence standards, early analysis provides the foundation for effective decision-making.

Professional valuators provide goodwill allocation analysis meeting AICPA VS Section 100 standards across multiple contexts including tax planning, divorce valuations under Georgia equitable distribution law, and M&A transaction advisory for businesses throughout metro Atlanta. Proper guidance ensures conclusions withstand IRS scrutiny from the Atlanta district office, Georgia Superior Court challenges under Daubert-equivalent standards, and buyer due diligence while achieving legitimate strategic objectives for Georgia business owners.

Additional Resources

Tax Code References:

- IRC Section 197 (Amortization of Goodwill and Intangibles)

- IRC Section 1060 (Allocation Rules for Asset Acquisitions)

- IRC Section 1(h) (Capital Gains Rates)

- IRC Section 11 (Corporate Tax Rates)

- Treasury Regulation §1.197-2 (Goodwill and Going Concern Value)

- Revenue Ruling 59-60 (Fair Market Value Standards)

Key Case Law:

- Martin Ice Cream Co. v. Commissioner [110 T.C. 189 (1998)]

- Norwalk v. Commissioner [8th Cir. 1998]

- Solomon v. Commissioner [T.C. Memo 2008-102]

- Mitcham v. Mitcham [263 Ga. 182 (1993)] (Georgia Divorce)

- Thomas v. Thomas [259 Ga. 73 (1989)] (Georgia Divorce)

Georgia Statutes:

- O.C.G.A. §19-5-13 (Equitable Division of Property)

- O.C.G.A. §13-8-53 (Non-Compete Enforceability)

- O.C.G.A. §14-2-1301 (Dissenters’ Rights)

Accounting Standards:

- ASC 805 (Business Combinations)

- ASC 350 (Intangibles-Goodwill and Other)

- AICPA Statement on Standards for Valuation Services VS Section 100

Professional Standards:

- ASA Business Valuation Standards

- NACVA Professional Standards

- Multi-Attribute Utility Method (MUM) Framework

Professional Valuation Services:

- Sofer Advisors – About Us

- Business Valuation Complete Guide

- Fair Market Value Calculation Guide

- Divorce Valuation Services

- Schedule Consultation

SCHEDULE A CONSULTATION to discuss your goodwill allocation needs with experienced valuation professionals serving Atlanta and Georgia business owners.

This article provides general information for educational purposes only and does not constitute legal, tax, financial, or professional advice-consult qualified tax advisors, Georgia family law attorneys, and valuation professionals regarding your specific circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}