How Long Does a Business Valuation Take? Complete Timeline Guide

Last Updated: Feb 2026

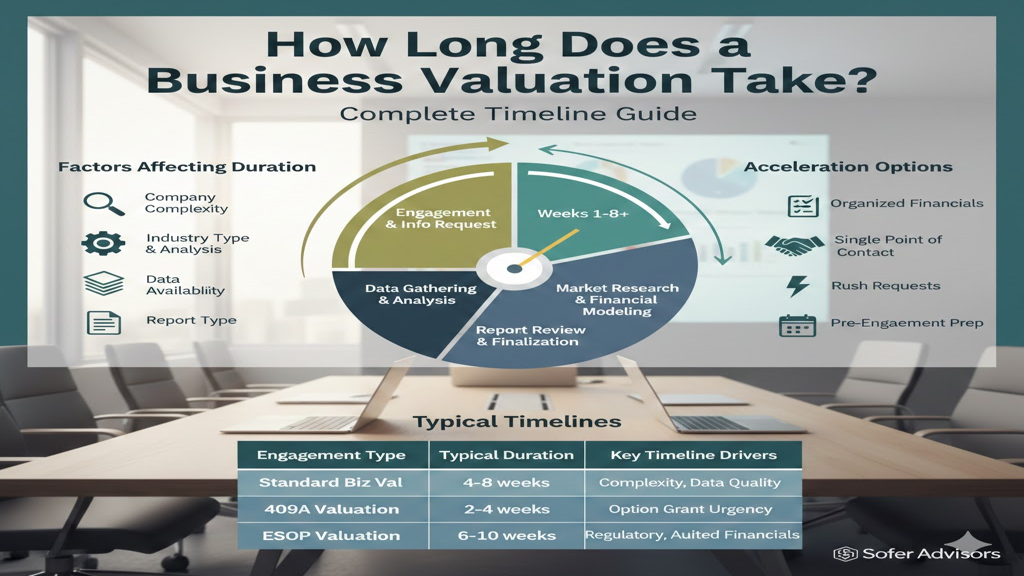

A business valuation takes four to eight weeks on average from engagement to final report delivery, though timelines vary based on company complexity, industry, data availability, and report type requirements. This duration encompasses information gathering, financial analysis, market research, report drafting, client review, and final revisions. Understanding typical timelines helps business owners coordinate valuations with transaction closings, tax deadlines, litigation schedules, and financial reporting obligations that depend on accurate valuation conclusions.

Timeline expectations matter because missed deadlines create serious consequences. Late ESOP valuations violate Department of Labor regulations. Delayed purchase price allocations under ASC 805 cause financial statement restatements. Gift tax valuations completed after December 31 cannot support current-year gifts. M&A transactions abort when valuation delays push closings past financing expiration dates. Litigation valuations submitted after court deadlines result in exclusion from evidence. Proper timeline planning ensures valuations serve their intended purposes without costly delays or compliance failures.

What factors determine business valuation duration?

Company size directly impacts the timeline. Single-location service businesses complete faster than multi-location manufacturers. Revenue matters-businesses under $10 million require less analysis than those exceeding $100 million. However, small companies with unusual characteristics may take longer than larger straightforward operations.

Industry complexity affects timelines significantly. Restaurant valuations complete quickly due to standardized metrics. Healthcare practice valuations require additional time for Stark Law compliance. Technology companies demand extended intellectual property and recurring revenue analysis.

Data availability dramatically influences speed. Companies with organized financial statements proceed faster. Businesses lacking formal accounting require extensive adjustments. Sofer Advisors provides detailed information request lists at engagement to help clients prepare efficiently.

Report type selection changes timelines substantially. Detailed reports require six to eight weeks. Summary reports complete in four to six weeks. Calculation reports finish in two to four weeks. IRS valuations require detailed reports while internal planning may accept summaries.

Valuation purpose introduces variations. Standard fair market value determinations follow predictable schedules. Financial reporting valuations require auditor coordination. Litigation valuations face discovery deadlines. ESOP annual valuations operate on fiscal year schedules with regulatory filing deadlines.

How does the valuation process unfold week by week?

Week one covers engagement. Consultations establish purpose and scope. Information request lists detail required documentation. Companies providing organized information immediately accelerate subsequent phases.

Weeks two and three involve information gathering. Valuators analyze financial statements, tax returns, and operational data. Responsive companies maintain momentum. Multiple follow-ups add weeks.

Weeks three and four focus on financial analysis. Valuators adjust financials for non-recurring items, owner compensation, and related party transactions. Complex structures extend this phase.

Weeks four and five cover market research. Valuators access GF Data, DealStats, and S&P Capital IQ for comparable transactions. Sofer Advisors maintains subscriptions to all major databases ensuring comprehensive access.

Weeks six and seven involve report drafting. Detailed reports include comprehensive documentation. All types require careful assumption documentation ensuring defensibility.

Weeks seven and eight allow client review. Drafts circulate for factual review. Sofer Advisors maintains next business day response policy ensuring revisions progress quickly.

The following table illustrates typical timelines:

| Engagement Type | Typical Duration | Key Timeline Drivers | Common Delays |

|---|---|---|---|

| Standard Business Valuation | 4-8 weeks | Company complexity, data quality | Missing financials, unclear ownership |

| 409A Valuation | 2-4 weeks | Option grant urgency | Pending funding rounds, incomplete cap tables |

| ESOP Annual Valuation | 6-10 weeks | Fiscal year-end coordination | Delayed audited financials |

| Purchase Price Allocation | 6-12 weeks | Asset complexity, auditor coordination | Customer contract terms |

| Litigation Support | Varies by court | Discovery deadlines | Opposing expert delays |

| Fairness Opinion | 4-8 weeks | Transaction timeline | Deal term changes |

| Update Valuation | 2-4 weeks | Changes since original | New debt structures |

What accelerates or delays valuation timelines?

Organized financial documentation accelerates timelines dramatically. Complete year-end statements, interim statements, tax returns, and detailed ledgers provided in week one eliminate common delays. Businesses requiring financials reconstructed from bank statements add weeks.

Management availability affects progress substantially. Responsive management answering questions within 24-48 hours maintains momentum. Companies where personnel take weeks responding experience delays. Designating a single point of contact prevents coordination delays.

Rush requests compress timelines to two to three weeks through dedicated resources. Sofer Advisors accommodates rush engagements when critical deadlines demand acceleration. However, rush timelines carry premium fees of 25-50% and require immediate complete information.

Scope changes mid-engagement extends timelines. Undisclosed subsidiaries, material related party transactions, or significant litigation change analytical requirements. Transparent disclosure prevents surprises.

These factors accelerate completion:

- Pre-Engagement Preparation: Gathering financial statements and documentation before engaging eliminates delays. Collect three to five years of financials, current interim statements, tax returns, and organizational documents proactively.

- Single Point of Contact: Designating one representative with information access prevents coordination delays. This person should have financial knowledge and operational understanding.

- Immediate Information Provision: Providing complete information within days maintains momentum. Partial provision requiring multiple follow-ups adds cumulative delays.

- Management Availability: Scheduling time for evaluator questions prevents waiting. Interviews require two to four hours total but scheduling delays extend timelines by weeks.

Rush premium fees of 25-50% compensate for priority scheduling. Standard $15,000 valuations become $18,750 to $22,500. However, poor planning creating artificial urgency wastes resources.

Analytical depth may decrease under extreme compression. Two-week timelines limit market research. When defensibility matters-gift tax, litigation, financial reporting-rushed timelines create risk.

When should I engage a valuator and how do types affect timing?

Transaction planning requires 90–120-day lead times before closings. Exit planning benefits from valuations 24-36 months before transitions identifying improvement opportunities.

Gift tax planning has strict year-end deadlines. December gifts require December-dated valuations. Valuation reports take four to eight weeks. Therefore, gift tax valuations should begin by late October or early November.

Buy-sell agreement implementation demands advance planning. Pre-event valuations prevent disputes. Annual updates maintain current references.

Financial reporting deadlines drive timing. Purchase price allocations under ASC 805 must complete within one year. Engaging within 30-60 days allows adequate time including auditor questions.

Litigation circumstances impose court schedules. Valuations should begin immediately after determining expert testimony necessity. Discovery producing relevant documents continues throughout litigation.

David Hern CPA ABV ASA, founder of Sofer Advisors, emphasizes proper timing transforms valuations from compliance into strategic tools. Early engagement allows scenario testing impossible under compressed deadlines.

Standard business valuations require four to eight weeks. These comprehensive engagements analyze financial performance and risk factors. 409A valuations complete in two to four weeks. ESOP valuations require six to ten weeks due to Department of Labor requirements. Purchase price allocations span six to twelve weeks based on complexity. Update valuations complete in two to four weeks, representing 50-70% of original timelines.

The following comparison shows timeline variations:

| Timeline Factor | Faster (4-5 weeks) | Standard (6-7 weeks) | Extended (8-12 weeks) |

|---|---|---|---|

| Company Size | Under $5M revenue | $5M – $50M revenue | Over $50M revenue |

| Locations | Single location | 2-3 locations | 4+ locations |

| Financial Quality | Audited statements, organized | Reviewed statements | Compiled statements, disorganized |

| Industry | Service businesses, retail | Manufacturing, distribution | Healthcare, technology |

| Report Type | Summary or calculation | Standard detailed | Financial reporting (ASC 805/350) |

| Data Availability | Immediate complete provision | 1-2 week gathering | 3+ weeks or incomplete |

| Management Response | Same or next day | 2–3-day response | Week+ response times |

What preparation minimizes timeline delays?

Financial statement organization provides the highest-impact preparation. Gather three to five years of year-end statements, current interim statements, and corresponding tax returns. Companies with only tax returns should consider having accountants prepare GAAP-basis statements.

Documentation compilation prevents delays. Collect articles of incorporation, bylaws, operating agreements, shareholder agreements, stock ledgers, and organizational charts. Sofer Advisors provides comprehensive information request lists, but proactive gathering accelerates timelines by weeks.

Management team coordination ensures response capacity. Identify who can answer financial questions, operational questions, and market questions. Block time for potential evaluator interviews. Designate a single coordination point preventing valuators from chasing multiple contacts.

Related party transaction documentation requires advance attention. Compile lists of related party entities and transaction types. Gather lease agreements with owner-occupied real estate, management fees, and interest on shareholder loans.

Industry-specific preparation varies by business type. Healthcare practices should gather payer contracts and physician employment agreements. Technology companies need customer contracts and intellectual property registrations. Manufacturers should compile equipment lists and capacity utilization data.

Frequently Asked Questions

What is the fastest possible turnaround for a business valuation?

The absolute fastest is two weeks for simple service businesses with organized financial information and management committed to same-day responses. Two-week timelines require rush fees of 25-50% and limit analytical depth. Most companies should plan four weeks minimum. Complex businesses, those lacking organized records, or situations requiring detailed reports need six to eight weeks regardless of urgency. When genuine emergencies exist, communicate with valuators immediately to explore feasibility rather than assuming compression is always possible.

Can I get a preliminary valuation estimate quickly?

Yes, preliminary estimates can often be provided within one to two weeks while formal reports proceed normally. These help with transaction negotiations or internal deliberations. However, preliminary estimates are not formal appraisal reports and cannot support IRS filings, financial reporting, or litigation. They typically cost 20-30% of full fees as separate engagements or may be credited toward full valuations. Preliminary work accelerates subsequent formal valuations since much analysis is complete.

How long does a valuation update take?

Update valuations require two to four weeks, representing 50-70% of original timelines and fees. Updates leverage prior analysis while incorporating current financial performance. Companies with minimal changes complete faster. Major acquisitions, operational restructuring, or new debt financing may require analysis approaching full valuations. Timing depends on how much has changed-discuss specific circumstances with your evaluator.

What causes the most common timeline delays?

Missing financial information causes 60-70% of delays. Companies lacking year-end statements, providing only tax returns, or missing interim financials create weeks of delay. Slow management responses add days or weeks cumulatively. Undisclosed related party transactions require additional investigation. Complex ownership structures need extra research. Scope changes when analysis reveals unexpected complexity and extended timelines. Companies can prevent most delays through proactive organization, immediate information provision, and transparent disclosure.

How do ESOP valuations differ in timeline?

ESOP valuations typically require six to ten weeks versus four to eight for standard valuations. Department of Labor regulations impose additional documentation and analysis requirements. Trustee coordination and review add time beyond standard client processes. Annual updates following established methodologies complete more efficiently. Companies with December year-ends should engage valuators by late January ensuring completion before Form 5500 deadlines. ESOP transactions involving leveraged structures require additional complexity analysis.

Can valuations be completed remotely?

Yes, most valuations complete entirely remotely through document sharing and video conferences. Site visits add minimal analytical value for service businesses or companies without significant physical assets. Manufacturing facilities or specialized equipment operations may benefit from physical inspection. However, even asset-intensive valuations increasingly use virtual walkthroughs. Remote engagements actually accelerate timelines by eliminating travel scheduling. Geography matters less than credential quality and experience.

How does multi-location operation affect timelines?

Multi-location operations extend timelines by requiring analysis of each significant location’s performance and characteristics. Two to three locations add minimal complexity. Five to ten locations require disaggregated analysis adding one to two weeks. Companies with dozens of locations need sampling methodologies. International operations introduce foreign exchange considerations and country risk analysis extending timelines by weeks. Companies should provide location-level financial statements and operational metrics proactively.

How do litigation deadlines affect valuations?

Litigation deadlines create hard timelines requiring careful coordination. Expert designation deadlines occur months before trial. Valuators need engagement soon after designation allowing adequate analysis time. Discovery continues throughout litigation producing relevant documents mid-analysis. Late production may necessitate supplemental reports. Deposition scheduling requires additional time beyond report completion. Companies should engage litigation valuators immediately after determining expert testimony necessity rather than waiting until deadlines approach.

Does report type affect timeline?

Yes, significantly. Detailed comprehensive reports require six to eight weeks. Summary reports streamlining content complete in four to six weeks. Calculation reports for limited purposes finish in two to four weeks. Report type should match valuation purpose-IRS and litigation typically require detailed reports; internal planning may accept summaries. Calculation reports may not be accepted for regulatory or legal purposes. Discuss report type requirements at engagement ensuring selected format meets your purpose.

Can providing more information upfront speed the process?

Absolutely-proactive complete information provision represents the single most effective acceleration method. Companies providing comprehensive financial packages, organizational documents, and operational data within days of engagement eliminate the primary delay source. Information arrival drives phase transitions-financial analysis cannot begin without financials regardless of valuator availability. Front-loading provision allows valuators to identify questions early. Partial information requiring multiple follow-ups adds cumulative delays. Create comprehensive packages before engaging rather than gathering documents reactively.

How much time between draft and final report?

Allocate one to two weeks between draft receipt and final report need. This allows management review, question formulation, and potential corrections. Companies requiring board presentations need additional time. Most valuators incorporate one revision round based on factual corrections within standard fees. Extensive revisions may require additional time and fees. Rush final turnarounds are possible within days when drafts contain minimal errors and clients respond immediately.

What delays can I expect with complex ownership?

Complex ownership structures extend timelines through multiple analysis requirements. Identifying beneficial owners, understanding voting and economic rights distributions, and analyzing shareholder agreements require additional time. Multiple classes of stock with different rights need separate analysis. S corporations with significant built-in gains require complex calculations. Partnerships with special allocations or waterfall distributions demand detailed modeling. Family limited partnerships with gifting history need extensive documentation review. Transparent ownership structure disclosure at engagement prevents mid-analysis surprises adding weeks.

Conclusion

Business valuation timelines average four to eight weeks but vary based on complexity, industry, data quality, and report requirements. Understanding timeline drivers allows companies to coordinate with transaction closings, tax deadlines, and regulatory schedules. Proactive information organization prevents common delays while management availability maintains momentum.

Sofer Advisors provides comprehensive business valuation services with transparent timeline commitments backed by 180+ five-star Google reviews and Inc. 5000 recognition. Our systematic approach ensures quality analysis while meeting critical deadlines through dedicated professional staff and next business day response policy.

Schedule a consultation to discuss your business valuation timeline needs and receive a detailed proposal outlining scope, deliverables, and completion schedule for your specific situation.

People Also Read

- How Do You Determine What a Business Is Worth? Complete Guide

- Business Exit Planning Strategies Guide for Owners in 2025

- ESOP Transaction Process Steps: Complete Guide for Business Owners

About the Author

This guide was prepared by David Hern CPA ABV ASA, founder of Sofer Advisors – a business valuation firm headquartered in Atlanta, GA serving clients across the United States. David holds dual accreditations as an Accredited Senior Appraiser (ASA) and is Accredited in Business Valuation (ABV), credentials recognized by the IRS, SEC, and FINRA. He also holds the Certified Exit Planning Advisor (CEPA) designation. With 15+ years of valuation experience, David has served as an expert witness in 11+ cases across multiple jurisdictions and built Sofer Advisors into an Inc. 5000-recognized firm with 180+ five-star Google reviews. The firm’s full W2 employee team maintains subscriptions to all major valuation databases and operates under a next business day response policy.

For professional business valuation services, visit soferadvisors.com or schedule a consultation.

This article provides general information for educational purposes only and does not constitute legal, tax, financial, or professional advice-consult qualified professionals regarding your specific circumstances.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}